My 2 cents on Gravita:

Opportunity and Supply Chain Dynamics

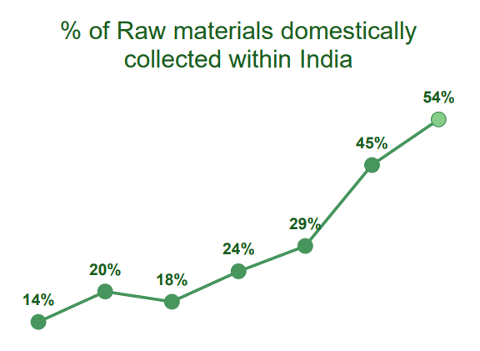

The Extended Producer Responsibility and Battery Management Rules 2021 impose strict regulations on OEMs and recyclers to get more raw material and supply better output. For instance, automotive and industrial manufacturers are expected to reuse 35-40% of lead used in batteries. (source – CPCB)

These rules were there since 2001, but apparently very poorly implemented. This has directly resulted in Gravita getting more raw material (batteries) from India:

This has triggered Gravita to increase their capacity from currently 200,000 MTPA to almost 400,000 MTPA by 2026. This will correspond to ~25% volume growth for the next 3 years.

Demand Trends

This is where things arent really blooming for them. The primary use (~80%) of Lead is in Lead Acid Batteries (LAB) which is a sunset industry. With Li-ion batteries getting affordable and much more sustainable, the shift could be imminent.

For now, the commentary of battery manufacturers and recyclers suggest that LAB are here for another decade with industrial growth (28% as per Amara Raja), use of LABs in Solar and Wind energy and small % of LABs still being used in EVs. But this evolution could be really quick.

Competition

In India where LABs are still relevant and showing some minor growth YoY, there are mainly just 2 competitors – Nile and Pondy. Though management has talked about a private Pilot industries as third major competitor. I also saw POCL (which somehow feels like a spinoff from Pondy itself), but it’s too small and in many other metal recycling solutions

One edge Gravita has over its domestic competitors is its raw material sourcing. Gravita collects almost 48% of batteries from Africa where the raw material prices are far less. For instance they have a 26% GM from their Ghana plant (there are other benefits as well like no import duty into Europe and tax benefits).

Although Pondy is a much smaller company with the same market opportunity, I feel they are at a higher risk due to being concentrated in Andhra and not able to import from Africa (shows in margins too).

Management

The management is as enigmatic as I have seen. They have made some sound capital allocation decisions to reach this spot. They have invested smartly by establishing plants in locations that help the business. Africa, Sri Lanka, and Mundra plants have relatively higher gross margins and some enjor special tax benefits (like Kathua and Ghana).

But on the other hand, management keeps looking for many other avenues. For instance, they have in the last 10 years:

-

Started a power company and closed it in a year

-

Started an IT company that has suffered a loss in every year since its inception

-

Invested in Real Estate business in a London associate of a family member

Although these things could be regular for companies of it’s size and there aren’t any glaring red flags as such!

One thing I loved about Gravita and its management is its employee friendliness. The increase in headcount and ESOP strategy is very transparent and fair.

Risks

No analysis is complete without this section. These are some risks I think the business faces:

-

Although their entire Lead inventory is hedged, the fall in Lead prices causes a corresponding loss in revenues. I consider this as deeply cyclical

-

Somewhat unpredictable future of LABs. Although the company has already grown to be a generic recycler than a Lead recycler (almunium and plastic). And more recycling products are coming up

-

Competition from unorganized sector and OEMs setting up their own recycling plants in future

-

Low capacity utilization – historically the Lead recyclers operate at ~50% capacity utilization. And since Gravita is doing a 500cr capex in setting up recycling plants, if the raw material supply isnt strong, they will operate at much less utilization level

Valuation

Although the valuations arent steep now, the stock had a strong run in the last 2 years. And with cyclicality coming in, it could make sense to wait for a down cycle.

Disc – tracking but don’t own. Investing learner, don’t take anything as gospel. Do your own research ![]()

| Subscribe To Our Free Newsletter |