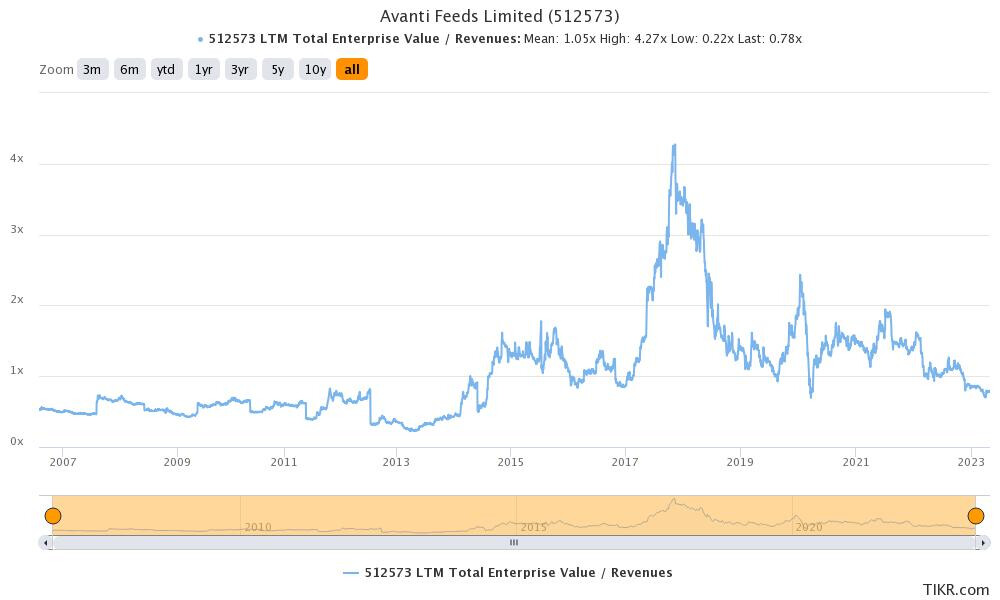

Its largely a reversion to mean story for me, its interesting to note that when I had first initiated a position in March 2020, my underwriting logic was the same as today.

Over time, as Avanti kept on gaining market share in shrimp processing business using cashflows from shrimp feed division, it became clearer to me that they are the absolute leaders in this industry.

Despite this, there has been no returns for a very long time as industry was first hit with raw material inflation resulting in contraction in profitability, which has now worsened as Indian shrimp cos are facing competition from Ecuador amidst slowdown in end markets.

All this has resulted in valuations of Avanti going back to pre-2014 levels. My observation has been that once stocks go through this kind of derating, one needs very few positive surprises to make money. That’s why I continue to hold (and also add to my existing position).

No.

| Subscribe To Our Free Newsletter |