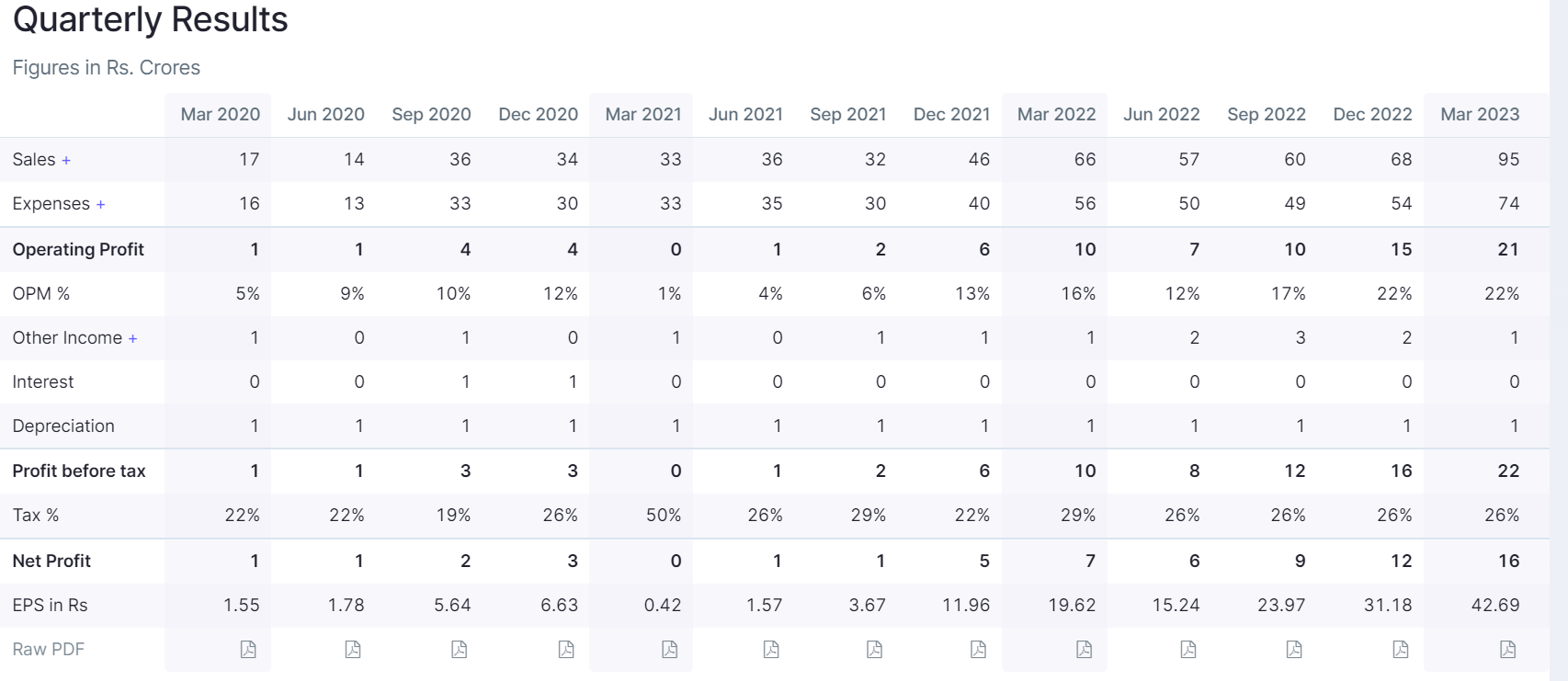

Thanks @sharemarketgen_ for regular insights on Shilchar performance

Shilchar has been delivering consistent growth with margin improvements over last many qtrs

Here is a quick peak in possible drivers behind this performance and more importantly how long can this demand tailwind last going ahead

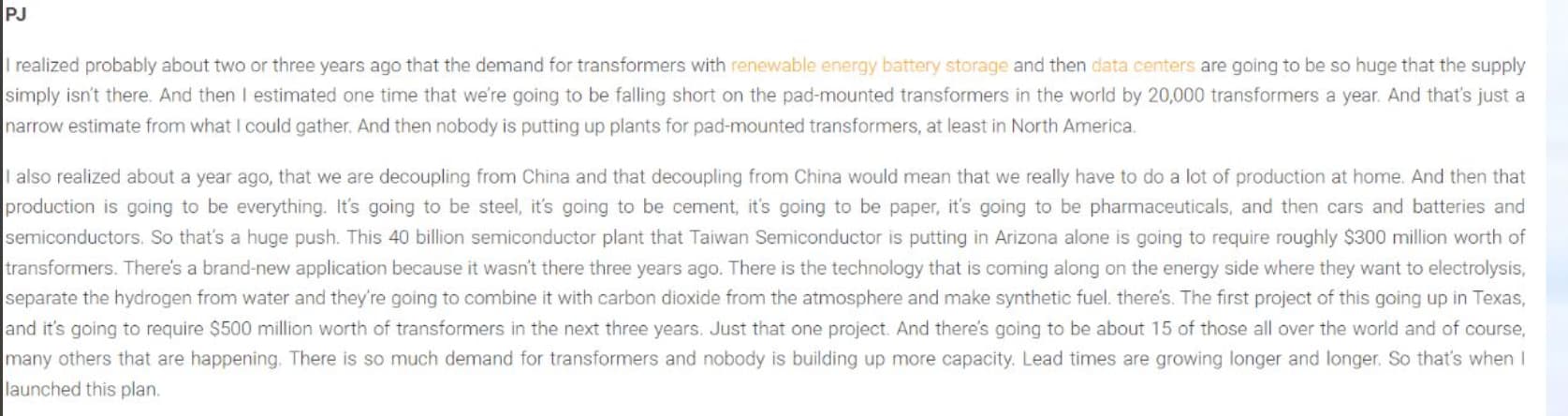

- Transformer Demand-supply scenario in US indicates supply shortages, structural pattern given a new transformer plant takes 1.5 to 2 yrs to commission – interview of largest transformer maker in USA

- US power infra needs massive upgrade (partly being 35-40 yrs old and beyond age limit) – per Utilities companies Transformers are critical to make it happen and are in shortages

- Transformer shortages are causing delays in home deliveries

Power transformer shortage causes delays in building new homes

Above are not comprehensive but just to get a feel of factors affecting demand – supply

In general Transformer players are upbeat, more so those in exports of electrical infra(shilchar doesn’t do concall but one can get good idea from concall of Apar industries, CG power etc on global electrical infra scenario), as captured in thread @rupeshtatiya notes + exports tracking – Shilchar is lot export focused and this reflects in performance (including cashflows), one can also see export trends of transformers from india

To watch for/better understand in next AGM

- India positioning in global transformer supply chain (China is biggest supplier globally but may not be into customization etc and high on labor costs, as well as in general China+1 theme playing out as described in Virginia transformer mgmt interview above)

- Shilchar technology differentiations and demand visibility

- Capex plan given demand visibility is indeed long term, minor uptick in FA per this qtr bal sheet visible as well of near 4 cr – quantum unclear

- High time required to commission a new plant – 1.5 to 2 yrs

D : Invested

| Subscribe To Our Free Newsletter |