I would start by saying that this was 6-7% of my initial capital allocation, but the sheer size of return in the last two years made it this significant in my portfolio today. I’m tempted to trim down, but I want to see how it performs in the next two quarters. You know, we give ourselves some leeway when we know that we have a sufficient margin of safety. And you start understanding compounding a bit when a stock gets this big, but yes, I still see the potential ahead.

In the second half of 2020, this counter started appearing simultaneously in my Results Blockbuster screen (Funda) + All that is Hot (Price-action) screen. I like growing, high ROCE companies with limited share, supply, and, of course, cheap valuations are the cherry on the cake. The only caveat I encountered were issues with Cash Generations and high TR in the B/S. I visited this thread and came across some audit-related concerns. But all in all, I ended up taking a small position due to some things that stood out for me across the pessimism, and I kept building my position in the next six months. One big thing which intrigued me was the claim of being the 2nd biggest company in white glue adhesive. What you are comparing now is 300Cr. MC micro-cap to the 1,20,000+ Cr. Mark Cap Pidilite, and I understand Pidilite is not just adhesive now, but still, that sheer comparison took me off guard. So I did some searching, which I highlighted in my Dec 2022 post. Here are a few other things that I find interesting:

- Ferocious buying from the promoter group across the shareholding history.

- It started with very cheap valuations and significantly fewer no. of shares O/S (40Lac – Pre Split: This is a turbo engine when everything is going hunky-dory).

- The language in the filings and disclosures started mentioning ‘Cash Generations Focus’ and ‘Brand Visibility,’ and they started delivering on that front.

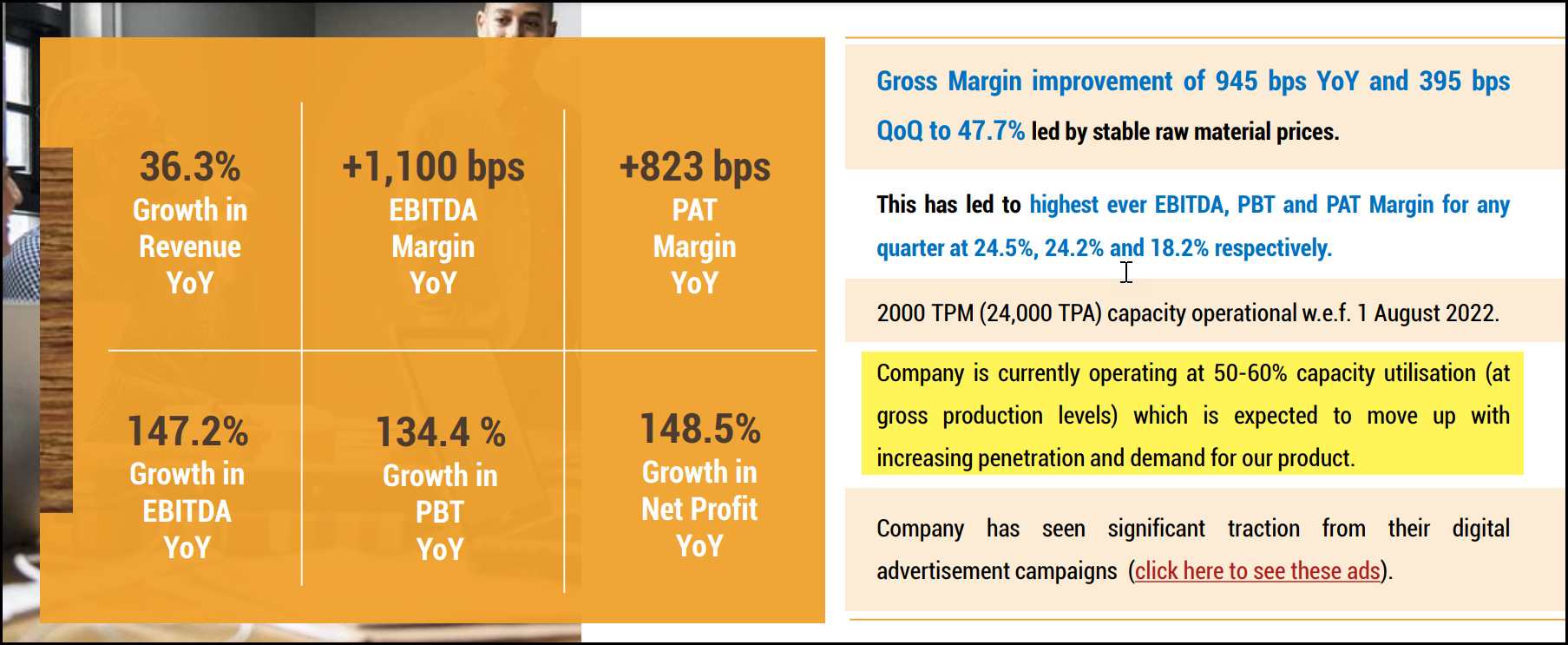

- Demand:- The company declared a 500MTM expansion from 1000 to 1500 MTM and, within 6-8 months, increased it to a further 2000MTM.

- Interestingly, their Product (Euro 7000) does have a degree of brand identification, and I would say it is pretty successful in tier 2-3 cities.

- Relatively small base and consumption-related nature of business. My portfolio in that period lacked such a consumption-related counter. Specifically, what I like about this theme is that if you prove the fundamentals of the business are strong, you can command a much higher price premium than any other kind of business.

Next, the results keep getting better and better, so I am still holding it now. But I would say I’m pretty anxious about what this company has to offer currently and if I should trim the size of it. One exciting thing I noticed in the latest EP is that the capacity utilization was still 50-60%, which I thought would be upwards of 70-80%.

Disc: Invested

| Subscribe To Our Free Newsletter |