BSIL – INFRASTRUCTURE (CORPORATE)

Bajaj steel – a lot seems to be changing, from a majority one product / one industry/ india focused to more of a engg solutions provider/ multiple industry /multiple country player. Corporate video above gives a good idea.

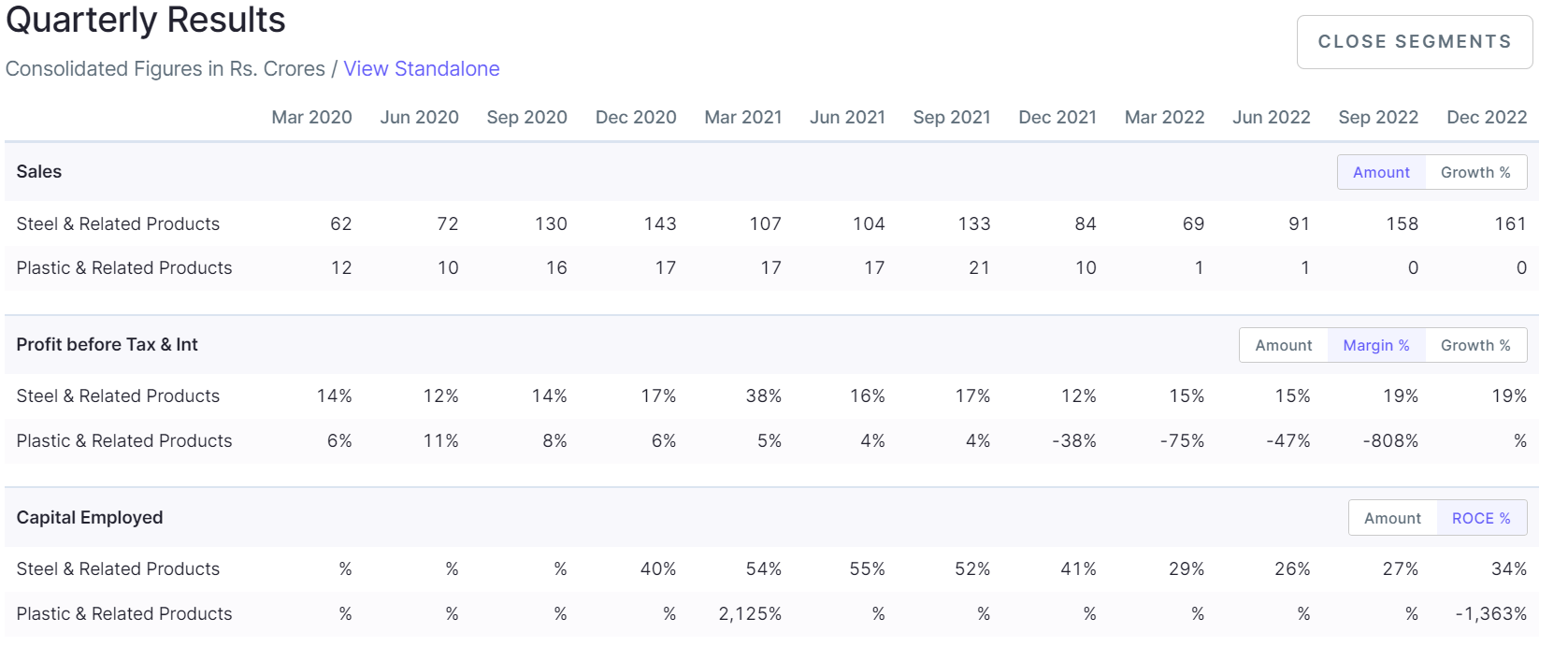

quick glimpse on numbers

recent developments

- Hived off loss making business

- Exiting of a set of promoter (took plastic biz) – clean run for current set of mgmt

- per recent credit report – sizable order book from PEB(pre engineering bldg – infra play – has done 1000+ projects per website) and many new customer + new geo for core biz

- Stable margins across last few qtrs (wd be better once hived off plastic biz no hit goes away)

- Focus on consumables + exports helping remove cyclicality for ginning machine consumables – AR and credit reports give good insights

- Strong export trajectory to US (via Baja coneagle – local setup in US)

- Good price action with good delivery based accumulation

- textile revival should augur well for ginning mills (a sizable end customer biz), as well as RM cool off to help

- Since they are one of majority player in ginning machinery exports – one can track same to get idea of trend – though that is not the only thing they do

Valuations – TTM basis 11PE is not demanding for a ginning leadership co and leadership position in ginning machinery and upcoming PEB verticals to expand opportunity size, clean bal sheet. Promoter holds substantial stake (incldg grp co under pulic holdg) and have increase recently.

Risk – Still ginning(cotton processing) heavy, Q2 and Q3 traditionally has been stronger though trend is smoothening, upcoming Q4 numbers need to confirm same. Not much communication from mgmt. to market besides YT channel. Success of other verticals stay a key watch out.

Conducive price action with good delivery % indicates accumulation. closer to ATH

D – Invested

| Subscribe To Our Free Newsletter |