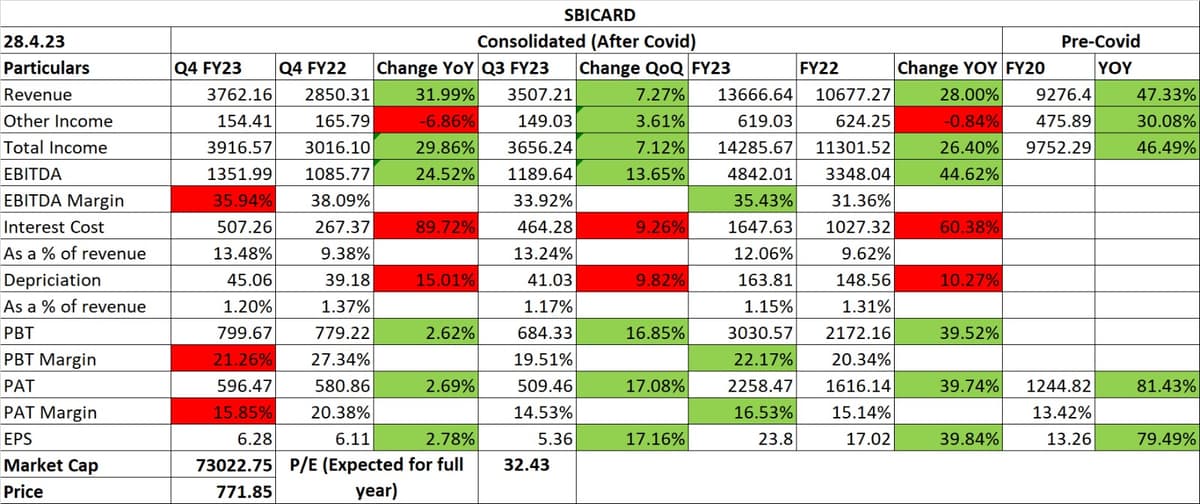

SBI CARD Q4 FY23 Result Update:

- Guidance: Cost of funds is expected to increase by 10-15 bps in H1 FY24. These are expected to reduce in H2 FY24. Margins will start getting better in H2 FY24. Credit costs will moderate gradually in the coming quarters.

- Spends conversion to EMI has been higher v/s the Pre-Covid levels that is driving the higher mix of EMI book. Revolver book is expected to witness a gradual recovery.

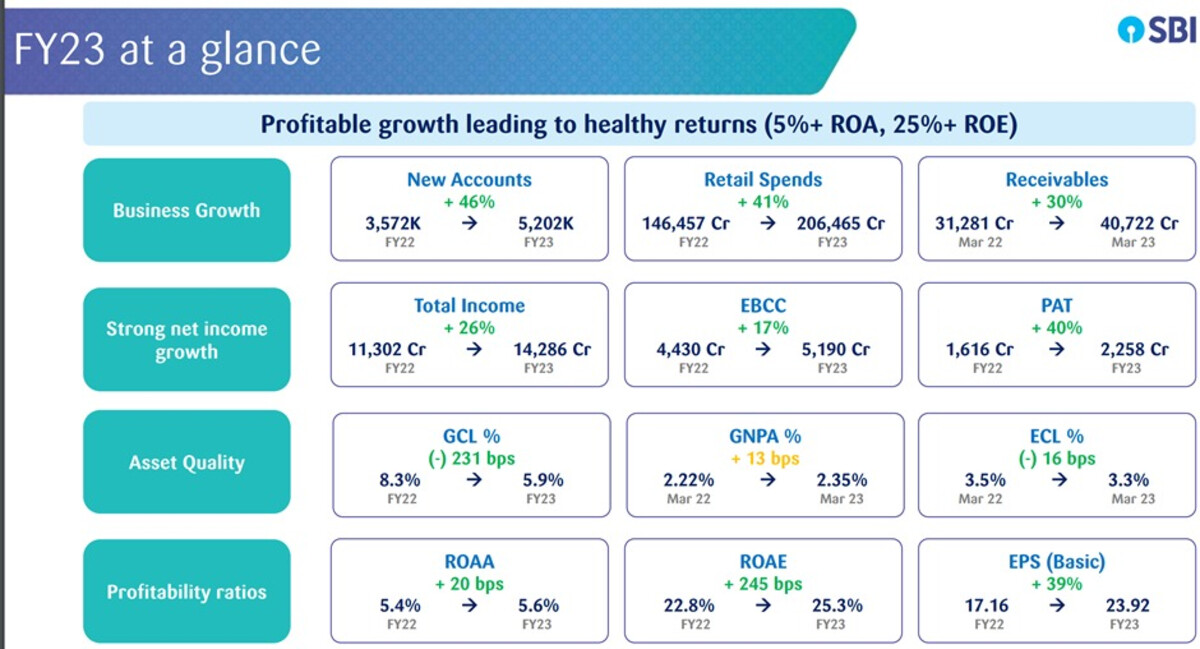

- Overall spends grew 32% YoY/4% QoQ, with retail/corporate spends rising 33%/32% YoY. The share of online retail spends stood at 57% in FY23. Spends in the industry is likely to grow at ~22-25% and SBICARD would try to grow higher than the industry growth rate.

- Brokerages have guided PAT for 23-24 to between 2800 cr to 2850 cr.

| Subscribe To Our Free Newsletter |