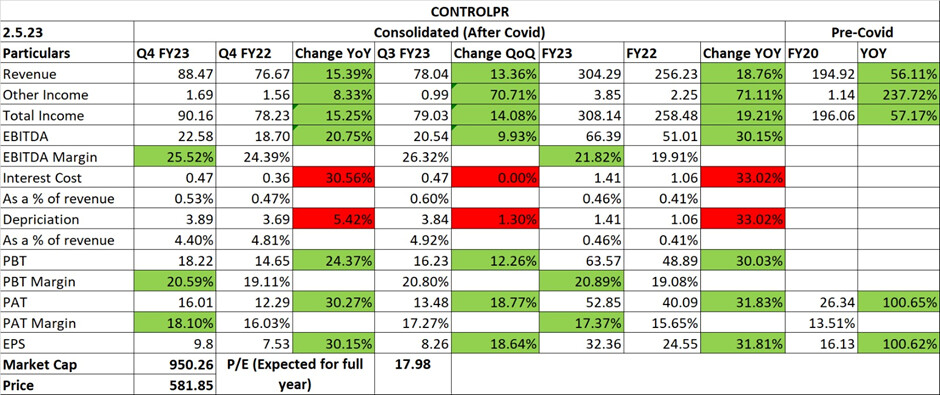

| – | Quarterly threshold of Rs. 800+ mn revenue crossed during the fourth quarter. |

|---|---|

| – | Consumables sales continued to be steady leading to overall EBITDA margins above 23.7% during the quarter and 25.5% for the year. |

| – | Building Material sectors has continued to see growing traction as infrastructure is promoted very highly. |

| – | Gross margins maintained above 60%. |

| – | Increase in share of revenue from consumables and focus on capturing larger market share with increasing installed set of printers. |

| – | New launches and demand from the replacement market would also be key growth drivers in the coming period. |

| – | The installed base of printers is currently at 17000+ against 16000+ as of December 2022. The company sold 950+ printers during Q4FY23 against 800+ printers in Q3FY23 and 675+ printers in Q2FY23. |

| – | Consumables segment contributes 55-60% of sales while the printers segment contributes 15-20% of sales and the balance is contributed by the services & spares segment. |

| – | Capacity utilization has been more than 60% for consumables segment. |

| – | 10% growth for consumables is easily achievable. |

| – | New products are being introduced for industrial and non-industrial verticals. These are specialized printing products, e.g. customized products with the plywood sector to give better branding (track & trace for other sectors). Currently at nascent stage |

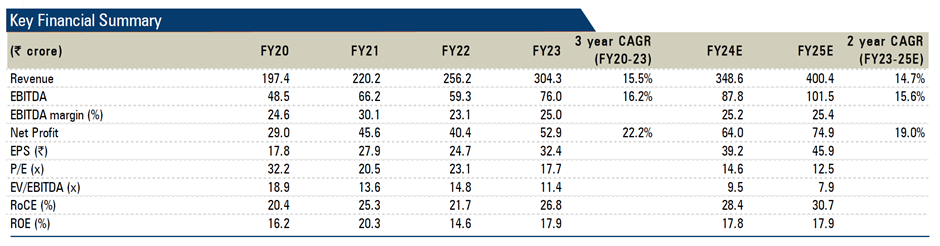

| – | ICICI Direct suggests a BUY with TP of Rs. 690. FY24 EPS is suggested at 39.2 and revenue at 348 cr. |

| Subscribe To Our Free Newsletter |