Chemours Q1CY23 Concall Snippets

On TSS (Refrigerants) business which consist of HFC and HFO

You kind of mentioned in passing that you kind of expected some really strong demand in the second half of the year going into that 2024 step-down in HFCs. Your volumes are pretty darn strong actually in the first quarter. I guess, are you seeing any – or earlier pull than expected for Opteon in some of your HFOs ahead of that step down? Or is this something else?

I think what’s driving volume – what’s helping to drive volume in Q1 was the strong automotive SAAR that we saw. Auto volumes were strong in both Europe and the U.S. And so I think as we think of the full year, one question for us would be where do auto volumes go? Clearly, the automotive companies are building cars with the supply chain more normalized. The question is with higher interest rates, does that continue throughout the year?

So I’d say our record Q1 performance in TSS is in part driven by strong auto, but it’s also being driven by continued adoption of Opteon in the stationary side. And then as we said earlier, strong HFCs based on an effective AIM and F-gas framework working as well.

So listen, TSS is really, out of the starting block, very strong. And we expect TSS to have a great yearYou mentioned the potential pull forward in refrigerants ahead of the step down. How much of an impact do you think that would have on your volumes after the regulation change?

So we’ll have to wait and see, to see what kind of summer we have? I think – my sense is, and we’ve indicated this on prior calls, is that the step down is likely to generate some level of buying activity as people sort of look, how much of my quota have I used up in the year, again based on how much demand there is this summer, how much do I have remaining and using that up towards the end of the year.

Clearly, in a market that’s restricted on volume based on a quota, that could drive more robust price in the second half. It may also have some impact on seasonal demand patterns throughout the year in terms of HFC demand as people look at their use of quota versus actual demand in the marketplace. So we’ll have to wait and see. But obviously, net-net, it’s a favorable impact on the business ahead of the step down next year.

On Advance Material Fluoropolymer business

Yes. APM is kind of a mix – well, APM has two distinct portfolios. Performance Solutions and Advanced Materials. And Advanced Materials tends to be “more economically sensitive.” These are broad industrial applications, where we saw some volume fade. There are also markets, candidly, we are deemphasizing as we free up inputs to drive the growth on Performance Solutions.

In terms of areas of strength, our Teflon PFA is integral to any new semicon fab. So while there’s some softness in electronics broadly speaking, there’s still a lot of focus on building new fabs for higher quality, lower node size chips, where our high-purity PFA is key.

And actually, the limiting factor for us on both things like PFA and Nafion membranes for hydrogen where again, we’re sold out is how quickly we can relieve capacity and, in some cases, get permits to expand capacity at some of our plants.

So there’s kind of a push and a pull within the APM segment this year where the advanced materials is more subject to sort of global macro, which you saw in our results in Q1. And Performance Solutions is really tied mainly to our ability to unlock capacity, which the team is really focused on.

as we said at the beginning of the year, for APM, this is a year of transition, right? You saw that in Performance Solutions is up 20%. Advanced Materials down 8%. And Advanced Materials are more economically sensitive business. So that’s kind of reflected as you’re going to think about overall seasonality into the year, have that overlay of the APM transition as well as you kind of think about overall guide for the full year.

Okay. Great. And then just lastly, there’s a large chunk of fluoropolymer and related chemistries market share available after 2025. Can you give a sense of how much of that Chemours should be able to pick up? And do you need to do any investments in 2024 on either in terms of new formulations, qualifications, customer service cost or CapEx to pick up that share?

We obviously believe that fluoropolymers are essential for modern living, but they are also key to renew economy whether we’re talking about high-speed data, AI, electric vehicles, hydrogen. And our big investments in APM today are focused on hydrogen, where we are wanting to do a significant expansion of our Nafion membrane capacity and capabilities.

We’re also expanding our Teflon PFA line in our Washington Works plant in West Virginia, which, by the way, we’re the only PFA supplier in the U.S. So if there’s a U.S. onshoring of chips, we’re key to that whole activity.

So the investments that we’ve announced today are both in Teflon PFA as well as the hydrogen facility, which we would like to cite in Villers-Saint-Paul in France, and we continue to be focused on those near-term opportunities. But the team is also very focused on debottlenecking a number of our plants.

Again, whether it’s demand for materials on the EV side, we’re really focused on the growth in our Performance Solutions business, which as you saw in the quarter, was up 20% and really is subject to more of our ability to bring capacity online more quickly.

Interestingly, Performance Solutions was 31% of the portfolio last year. In this recent quarter, it’s 39%. So that higher CAGR is making the APM segment a lot more specialized as we move forward in time. And candidly, when I look at our TSS and APM business, I really would agree with the sentiment that our multiple doesn’t reflect the power of the earnings of those businesses over time. So we’re very excited about where we go from here, and the team is very focused on delivering.

Solvay Q1CY23 Concall Snippets

Specialty Polymer (Fluoropolymer) Business

Sales in Specialty Polymers improved 15% driven by higher prices as customers continue to value what we bring are lightweighting solutions because these are mission-critical and they also have to reduce CO2 emissions. Volumes were slightly down mainly because of reduced demand in EV batteries as customers continue to reduce their high inventory levels. And that impacted the demand for our PVDF, but it’s important to note that our PVDF suspension technology offered a differentiated value proposition, specifically for the high-end battery applications like NMC. And this supports margins even in the current inflationary environment. Elsewhere, sales grew most notably in the electronics market, where our polymers are used in semiconductors and also grew in our Life Solutions sector where our polymers are used in pharmaceutical packaging and hemodialysis.

On the PVDF market dynamics. Can you maybe indicate how far the destocking has gone at the customer level? And also what’s that destocking trend has maybe caused to pricing dynamics in the market? I know you have different technology in the mainstream and you’re in the high rents, but can you maybe also elaborate on the pricing dynamics for your products and the market overall in PVDF?

we told you that there has been a destocking which will continue probably to quarter 2 as well in general, in batteries in automotive. But as you’ve seen, frankly, and I will come back to batteries, our business is not only PVDF battery, right? I mean you’ve seen Specialty Polymer really doing well, including in other applications in auto under the hood, right? So we’re in business of lightweighting, electrification, but please do not forget lightweighting.

On PVDF, Wim, yes, there has been a destocking on EV batteries and you’ve seen it in many other publications. We expect it again to continue in over quarter 2 this year. On the differences, and I think we’ve tried to do some education on emissions versus suspension, Karim alluded to that again. There are 2 types of PVDF technologies for EV battery suspension emission. No one material is inherently better or worse than the other, but we produce both. But the reality is that suspension-grade PVDF in which Solvay is the world leader, has a set of properties that make it better suited for nickel-rich high-energy density cathode like in lithium-ion batteries and specifically with NMC, which is the high-end batteries in the market, right?

So the suspension is the reference binder material in the production of those NMC material. There is basically no immersion PVDF used in NMC today. I know people are still trying to get there, but this is mainly suspension. And the emersion PVDF, it’s commercial products available worldwide with Chinese competition. We expect that to be more commoditized in the midterm and with very little again and no significant penetration in the high end in NMC.

So what has happened, I think, for us, obviously, there is a raw material cost decrease. For us, we just kept our margin constant and even as compared to the end of last year. So without giving you that much number and sensitive competitive information, our Q1 PVDF battery margins have been stable compared to the end of last year.

So I think that’s the message that’s how we ask our team to fight for value pricing on PVDF. So we are more resilient than the other technologies. And definitely, we like our – the investments we are doing in Europe and in the U.S. in the suspension because the barrier to entry for imports, for example, from China, like in the United States of America are pretty higher. The tariffs are high, more than 30%. So all of this makes our strategy very sound for future growth CapEx.

I think the volumes, and I talked about the destocking right on the PVDF side. And we are more resilient than others because, again, our Specialty Polymer portfolio generally is not only automotive, by the way – is only one sector that in automotive, is not only batteries. So I think the diversification which investors do like in the Specialty Polymers is really a good thing. We had many markets with Materials delivering volume growth with only batteries down. So in Specialty Polymers, we have a new fab equipment supported growth for our polymers using electronics. We also delivered volume growth, for example, in health care applications, such as pharma packaging.

Something important to note is while polymer demand for EV batteries was low due to destocking. Again, the polymers auto and non batteries grew in the quarter under-the-hood application. .

So the pricing level versus last year, the business has demonstrated its ability to maintain higher pricing which was the main driver of the growth. So that’s value pricing. I’m not going to repeat my favorite case and story of replaced metal under-the-hood.

Customers, they come to us when they have many ends, like they need chemical resistance, bridging resistance, et cetera. So as many ends needed they come to us. So that makes us very differentiated. And even, by the way, when you look at our batteries products, right. In the destocking, we kept the margins, right. The percentage sales – the EBITDA margins for those products or gross margins for those products became stable.

So over time, we will continue value pricing our solution. While in some applications, we will get back pricing when raw materials are favorable, right? By the way, we did it somewhat in batteries because 142B, for example, as the raw material prices for those who are – they know the Level 2 or 3 of the formula of batteries and PVDF we gave away, but we protected our margins, right? We sustained margins when – even when the batteries volume and destocking is happening.

And longer term, we have Speciality margins here. That’s what we are talking about. And we will look for more profitable volumes because given lightweight and electrification, we will continue penetrating with those technologies, like in composite, whatever the market that. So it’s value pricing, right, not value based on cost plus, right, or cost plus? And I think that’s what you can expect from us in the specialties and in Specialty polymers, specifically.

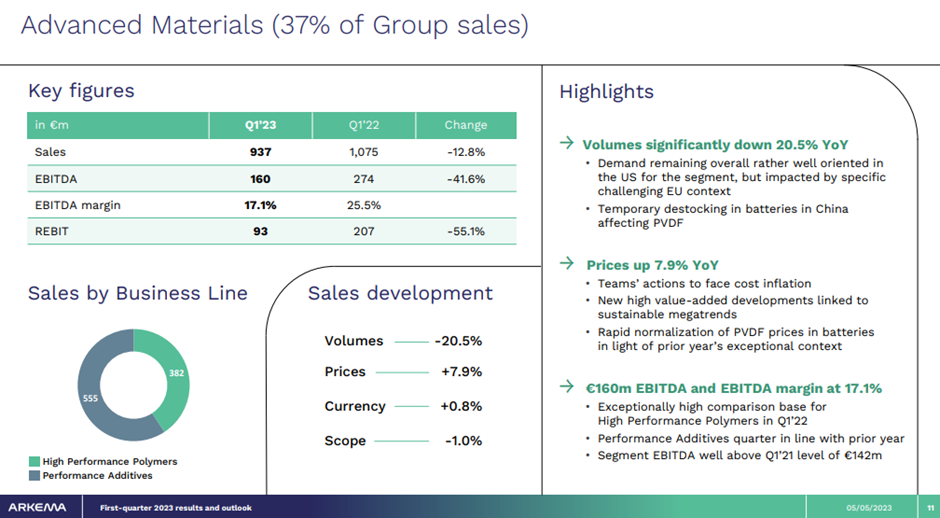

Arkema Q1CY23 Concall Snippets

Advance Materials (Fluoropolymer) Business

Our volumes were lower year-on-year due to poor demand in Europe, slowdown in construction in the U.S. and significant destocking in batteries chain, temporary but significant in China, which impacted PVDF.

Excluding PVDF volume in China are pretty much in line with last year level for our Specialty Market’s Materials against a rather low comparison base.

The 20% volume decline in materials looks like something you perhaps would have seen at the depths of the financial crisis. I appreciate you’ve got a diverse portfolio going into lots of applications and markets, but can you just elaborate a little bit on why the volumes are so bad? And I think in your introductory comments, you did mention some impact of strikes in France. Is it possible to isolate perhaps what the impact of that was within the volumes?

On the first front, I would say strikes is incremental, but we would say in this kind of environment, even incremental could cost EBITDA. So this is why we mentioned it, but we did not mention it as a broad topic, but I think in our transparency, it was important to mention it. But I would say it’s quite an incremental number inside the 20%. So I would not make it a big topic at your level. No, the 20% is mostly coming from destocking. This means that it’s not reflecting the true GDP.

It’s clear that it takes time and I agree that the numbers are big, not only for us, but for other peers, which are positioned in the same end market. And – which my interpretation beyond the macro that you know – as we know, is that after the COVID, after the tension on the raw material side, which happened in the first half last year and in the end of ’21 and also on the transportation limitation, a lot of stock has been built along certain value chain. We still need to be digested. This is my explanation. As you have a long history in this industry, that you have so long destocking. So you have to put that in the context of the post-COVID and also this element, which creates a suppletion disruption last year and the year before the last. And we are still to a certain extent being impacted with that on top of the macro, so we have the double paying.

Now, as you know, we have seen different situation in the past. We are – we work on our self-help. We are patient. At the end, it will change. I think the good news is that if you look at the kind of EBITDA, we have been able to deliver with this low volume as the end is solid, but I agree with you. There is some frustration there because normally, you don’t get hit by so little volume for such a long period. Now it will come back and maybe there will be in the second half, restocking that will also support delivering the result on the full year. So you know me, we work on – we don’t compliant. We work and we believe that it will come back. We have just to be patient.

We are not losing market share, it was also one of your questions. So it’s really the end market. Maybe they have been helping us well in the past 2 years. So we have some counter back, but no specific answer beyond stopping and also macro, which is not overall supportive currently. But – so this is why we really work very strongly on the short term, mitigating the impact, but we continue to invest in the long run, which is part of your second question because we believe that at the end, it will come back and sustainability, at least for the one we are well positioned and Arkema is one of them will be really a key driver of growth for the coming years.

And the second question is really on PVDF. Apologies for asking this, but could you just tell us like fundamentally, if you have the technology to make suspension-grade PVDF. And if so, you could actually compete at the highest end, if possible? Or is it that you guys have a genuine technological gap with one of your listed peers?

With regard – I don’t want to enter too much in the detail of the PVDF, but I will make a couple of comments. First of all, PVDF, you have different technologies. Some are better for certain applications and some are better for other applications. So I don’t think that there is only one by far. And even in batteries, for certain applications, suspension is better, for other emissions better.

With regard to Arkema, as everybody know now because it was communicated by one of our competitors, we are a company, which is – which has been focused on the emission. And I think we are glad about it. We are very strong in that. Can we make suspension not now because of tools, we’ll be able to make suspension in the midterm. The answer is yes. Do we have beyond what we are making today, evolution of our products, including emission, which will address the market in batteries for different applications, new generation, et cetera? The answer is yes. Is PVDF sufficient to address the battery market? The answer is no. You need to have other technologies and other technologies? The answer is also yes. So I think we have plenty of cards to play. You have not one a company, which is positioned like the other was. This is the beauty of this incredible – incredibly growing market. I think we have a position with some very strong strengths and some weaknesses the sale for our competitors, but we have really enough to be the fantastic story. So don’t worry about that.

| Subscribe To Our Free Newsletter |