Punjab Chemicals & Crop Protection Ltd

I have tried to see the 3 big fall in Punjab chemical and found few things in common.

-

All the three fall are between 60% to 70% with an average of 65%.

-

During the coivd fall it took support near the all time high of 2015 and the current share price is close to the all time high of 2019.

-

The current P/B is now below the all time low during covid. It is also below the 10yrs median of 6.3 and 5yrs of 7.8. Current P/B is 3.5

-

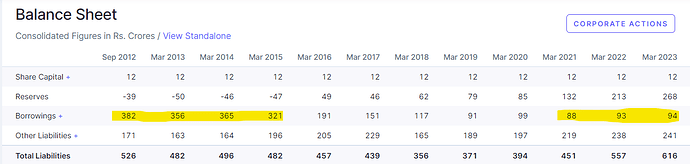

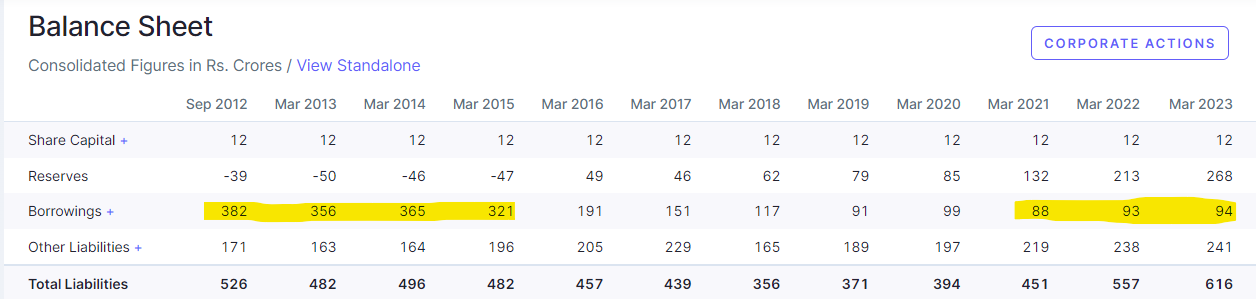

Over the years debt has been reduced substantially

-

The company is planning to do sales of 1500cr by FY25 with margins of 14% to 15%. The current sales is 1000cr and margins are 12%.

-

This company generally has an Asset turnover ratio of 4 to 5times and they are doing a capex of 150cr . So this is where they are planning to get the incremental sales.

This company has been covered very deeply by harsh Sir. There are good 1hrs videos on youtube in VP EUROPE channel which covers this company

Overall looks like the downside is less and the entire agrochemical space is going through the downcycle. Things are expected to pick up form Q1,Q2 FY24

Invested at around 780 levels

| Subscribe To Our Free Newsletter |