| – | The Return on Equity for FY23 was 15.7%. ROCE is at 12%. |

|---|---|

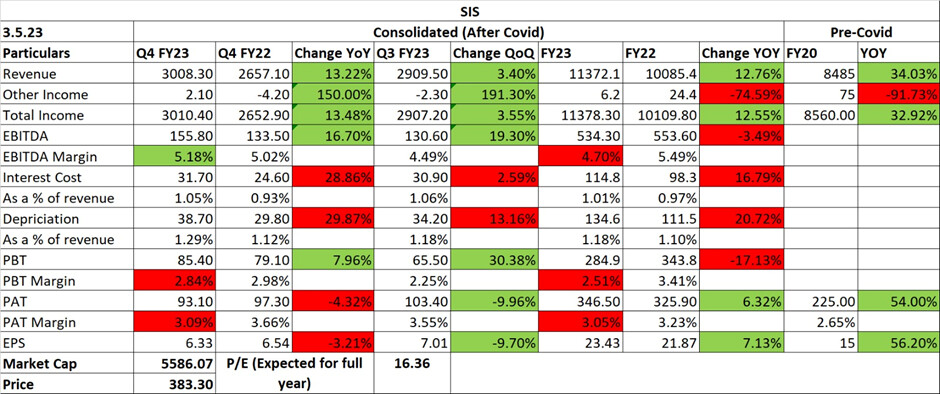

| – | Security Solutions India posted a revenue growth of 19.9% over FY22. Our technology based security solutions businesses continue to grow, with 1,088 new installations during the quarter in VProtect , our Alarm monitoring and response business, which now services more than 14,000 customer connections. Additionally, the VProtect business has a strong pipeline with confirmed orders of almost 5,000 sites of to implement in the coming quarters. |

| – | Facility Management Solutions posted a revenue growth of 36.2% over FY22. This growth was primarily driven by new wins of around INR 11 cr. of monthly revenue in Healthcare, Manufacturing, IT and Transportation segments. The role of technology in service delivery is increasing with increasing interest from customers for more mechanized and advanced facility management solutions. DSO days remained stable at 85 days during Q4 FY23. |

| – | Security Solutions International posted a revenue growth of 0.7% over FY22 (0.5% on constant currency basis); the growth was achieved despite the one time COVID related contracts falling off this year. Labour shortages in international geographies continued to affect costs. |

| – | Cash Logistics also continued its strong revenue growth with a 38.3% growth over FY22. |

| – | Margins have shown improvement due to robust management of operations. |

| – | Due to, hardening interest rates and the strong cash flow generation in FY23, post Q4 FY23, we have paid down A$15 mn . (INR 82.6 cr.) to the debt syndicate led by National Australia Bank (NAB) in Australia and reduced the outstanding amount to A$88.5 mn (INR 487.1 cr). |

| – | Net Debt/ EBITDA was 1.75 as of end of Q4 FY23, which was lower than 2.06 as of end of Q3 FY23. The decrease in Net Debt / EBITDA was driven by better working capital management during the quarter. |

| – | OCF/EBITDA on a consolidated basis was 144.2% for the quarter which is a result of the strong working capital management. DSO for the quarter reduced by 2 days. |

| – | Client concentration is very low. |

| – | Guidance: Confident of gaining medium term momentum on the backdrop of deals won. Expects improvement in margin front. Expects pickup in facility management & security business. For Facility management, the growth trend will continue but more focus on EBITDA margin rather than top line. Want to keep the D/E ratio at 1.5-2 range. The ideal ratio would be to keep a little below 1.5. Reach pre-covid level margins in India business which is 5.5-6%. Traction in FY24 is such that margins will be achieved. |

| Subscribe To Our Free Newsletter |