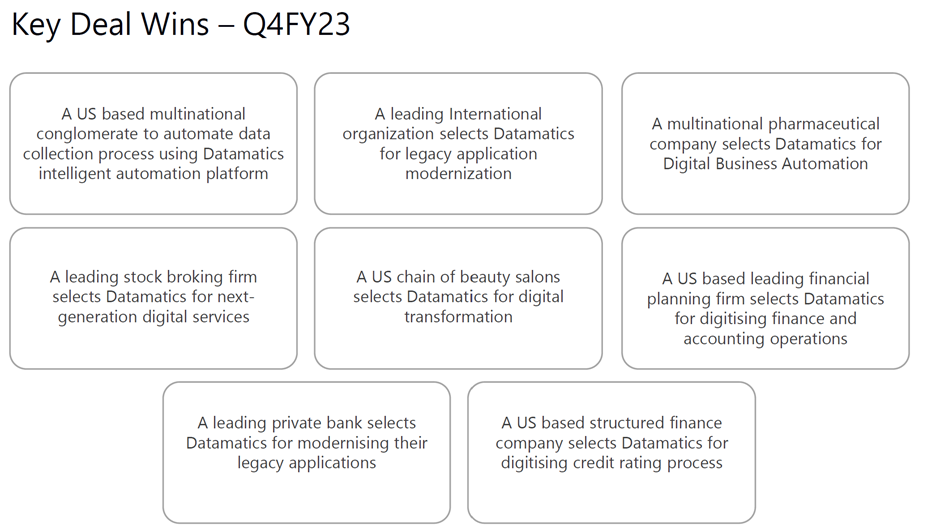

| – | 300+ clients worldwide, added 21 clients in Q4FY23. Signed total contracts of 20 million in the Q4 FY23. |

|---|---|

| – | Attrition rate at 24.8%. |

| – | Digital Operations: 45% of total revenue from 41% in last quarter. EBIT Margin of 23%. Industry-vertical-oriented operations and enterprise back-office operations segments are expected to witness the highest volume of new work in next 5 years. Finance & Accounting Operations are expected to grow at 9-10% CAGR over the next couple of years. |

| – | Digital Experiences: 14% of total revenue. EBIT Margin of 28.2%. |

| – | Digital Technologies: 41% of total revenue from 43% in last quarter. EBIT Margin of 9.1%. Turned profit making in Q3 FY23. Growing traction from more IT spending & Intelligent Process Automation. Shift to growth of cloud over on premises. |

| – | Change in revenue mix led to better margin overall. The expansion of margins can be attributed to strong revenue growth, cost optimizations, reduced attrition and revenue conversions at higher price. |

| – | ROE/ROCE at 21.4%/20%. |

| – | D/E at 0. |

| – | Total Cash and Investment (Net of Debt) increased from 428 in FY22 to 498 cr in FY23. |

| – | Guidance: Full scale impact of price hike can be expected in FY24 which will help to maintain a stable and healthy margin profile. Price hikes of 5-30% have been taken. Supply side challenges are seen easing which help in maintaining margins same as this year. They have a healthy pipeline and will grow on the base of new customer acquisition. Headwinds seen in demand from US and Europe. Revenue growth in FY24 expected to be 14-15%. Same kind of deal wins expected in FY24. |

| – | Targeted Acquisitions: Have initiated dialogues with several customers or prospects target companies. Looking to make acquisitions worth 20-50 million in FY24. |

| – | Brokerage Choice is giving a revenue target of 1750 cr for FY24 and EPS of 37.2 for Target price of 447 (already achieved). |

| Subscribe To Our Free Newsletter |