Not sure if the CA in your name refers to chartered accountant or something else, but correct me if I’m wrong, there seems to be a fundamental misunderstanding of the Cash flow statements for a lending company.

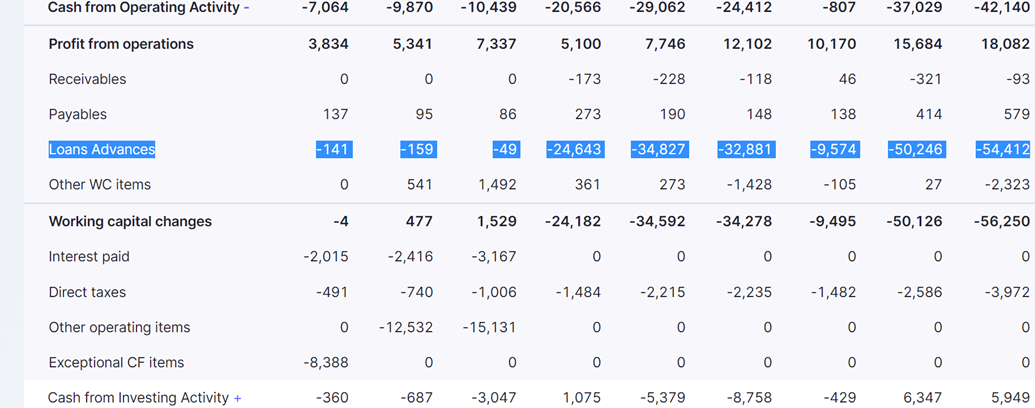

- In financial (lending) companies its not the CFO (positive or negative) that reflects the strength of the business unlike in manufacturing firms etc. Lending being the primary operating activity it is expected that growing NBFC’s will lend out money (that will reflect as a negative cash item “loan advances”) below the “cash flow from operations” sub heading (Pic below). What is important, is to ensure that this negative CFO is matched by the CFF and CFI line items, otherwise the firm will burn through the cash on the B/S. If you look at a Bajaj Finance or take your pick of any lending NBFC, they all have negative CFO’s. And this is by design, it is not a flaw. That’s how GAAP/IFRS accounting works. If they have a positive CFO that should be a reason for alarm in my view

and not a negative against the company. Bajaj Finance’s CFO below.

and not a negative against the company. Bajaj Finance’s CFO below.

- As for the promoter holding being low – Again, this is because of the nature of a lending business. In order to fund growth and maintain Tier 1 capital above the regulatory requirements, almost all lending companies have to dilute stakes periodically. And this dilution overtime results in a smaller promoter holding. Bajaj finance seems to be an exception here with a holding greater than 50% but if you look at all the other peers, a Shriram finance or an Aavas etc. It is difficult to grow the book stupendously without diluting. If they try to do this they will be severely over leveraged (8-10x book value). I think over leveraged financial companies are a bigger risk than an “optically” low promoter holding of 35%.

Anyways, I don’t think its of any benefit to anyone if this page becomes a crash course in accounting ![]() .

.

Lets try and dig deeper in to their business to poke holes at the operating model of Five Star, to identify risks and operating challenges of lending sub prime in India. Things I am still struggling with include

a. How good is the collateral & how liquid is it? Are homes ranging from 4-10 lakhs in tier 6 cities good collateral ? Or is the low LTV an optical illusion. Are these homes liquid? I am trying to find data points regarding the same.

b. As an add on to the previous point, what is the state of land records in Tier 3- Tier 6 cities in India? If these are still antiquated and not digitized could this potentially be a ceiling to future growth? Land records being a state subject in the constitution, is that why Five star has mainly focused on the southern states so far, which have digitized/ considered to have less ambiguous land records?

c. Their lending model being labor intensive because of the customer profile and the amount of manual on ground checks that are required prior to lending, how scalable is Five Star’s business? They have demonstrated incredible growth (growing 50x) in the past 7 years, but what would it take (in terms of employee head count & back end technology stack) to add 300k-400k new customers annually without compromising on asset quality?

d. Why is a Five Star or an Aptus etc. averse to leveraging more than 3-4x of book? It’s definitely not because of CRAR requirements. What do they know that we don’t? Are they concerned that if they leverage beyond that, a negative shock could wipe out book value? If so, is that a sign of fragility? Shouldn’t their collateral & low LTV help in recovery even if they do leverage beyond a 3-4x?

| Subscribe To Our Free Newsletter |