Results are out!

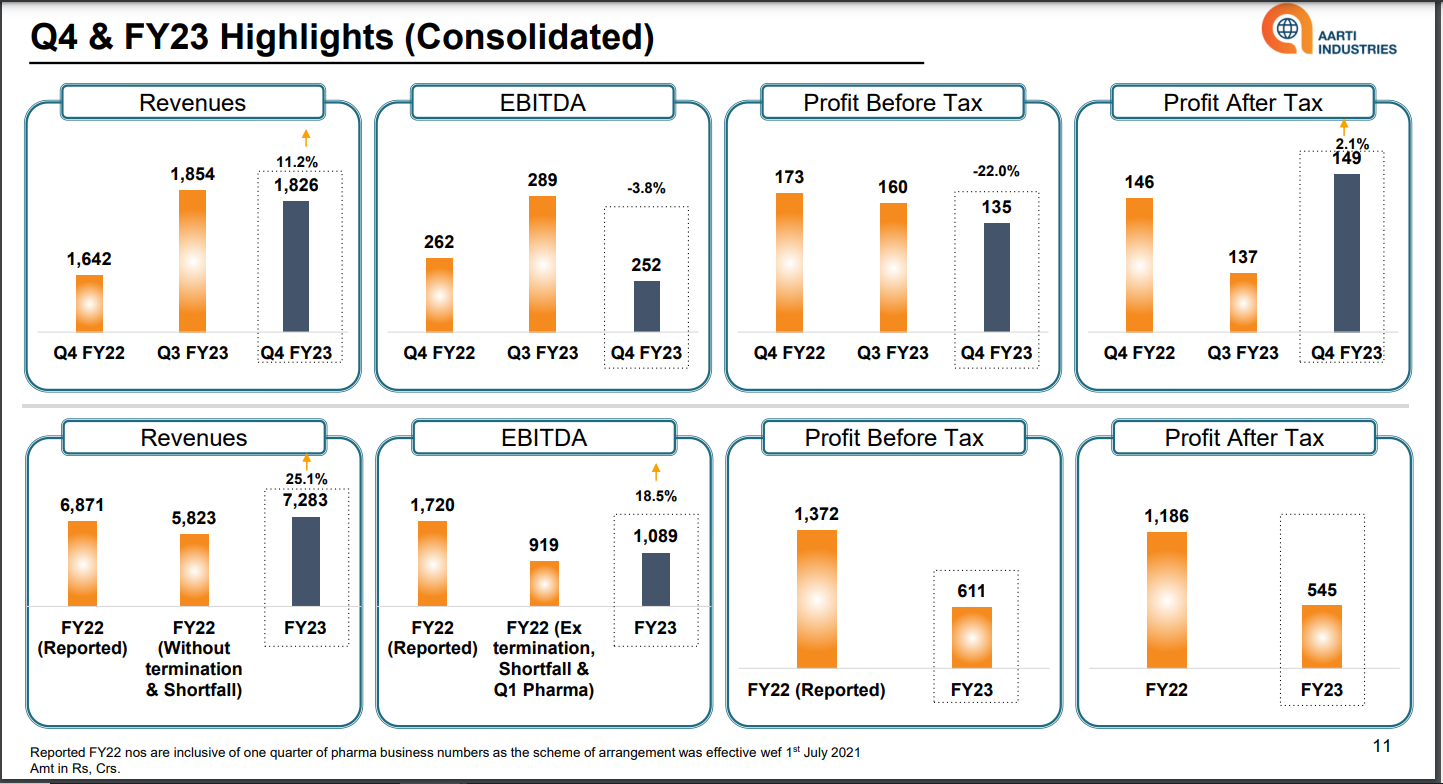

Again they are conveniently taking the lower numbers i.e. without termination and shortfall (for YoY Revenue and EBIDTA) to show better growth compared to FY22 ! Request someone who has been following this closely to comment on the results.

Highlights from MD V Gogri’s commentary:

Positives:

- For the current fiscal 2023-24, the firm is looking at volume growth of around 25 percent. Part of that volume will come from our non-regular market because regular market demand is under pressure.

- Discretionary side demand seems to be recovering from at least the first quarter of FY24.

Negatives

- EBITDA growth will be lower (than revenue rate), we will be targeting around 20 percent growth in EBITDA for FY24

- Some global demand is still under pressure on the discretionary side because of higher interest rate.

General commentary:

- Company is targeting revenue growth of about 30 to 45 percent over two years (at constant raw material cost).

- Some inventory correction is also taking place. So the feedback we are getting is that quarter-on-quarter, demand should increase on the discretionary side in FY24

- Exports will be continuing – around 50 percent of the sales will come from export

| Subscribe To Our Free Newsletter |