Information dump that might useful for people trying to understand the business

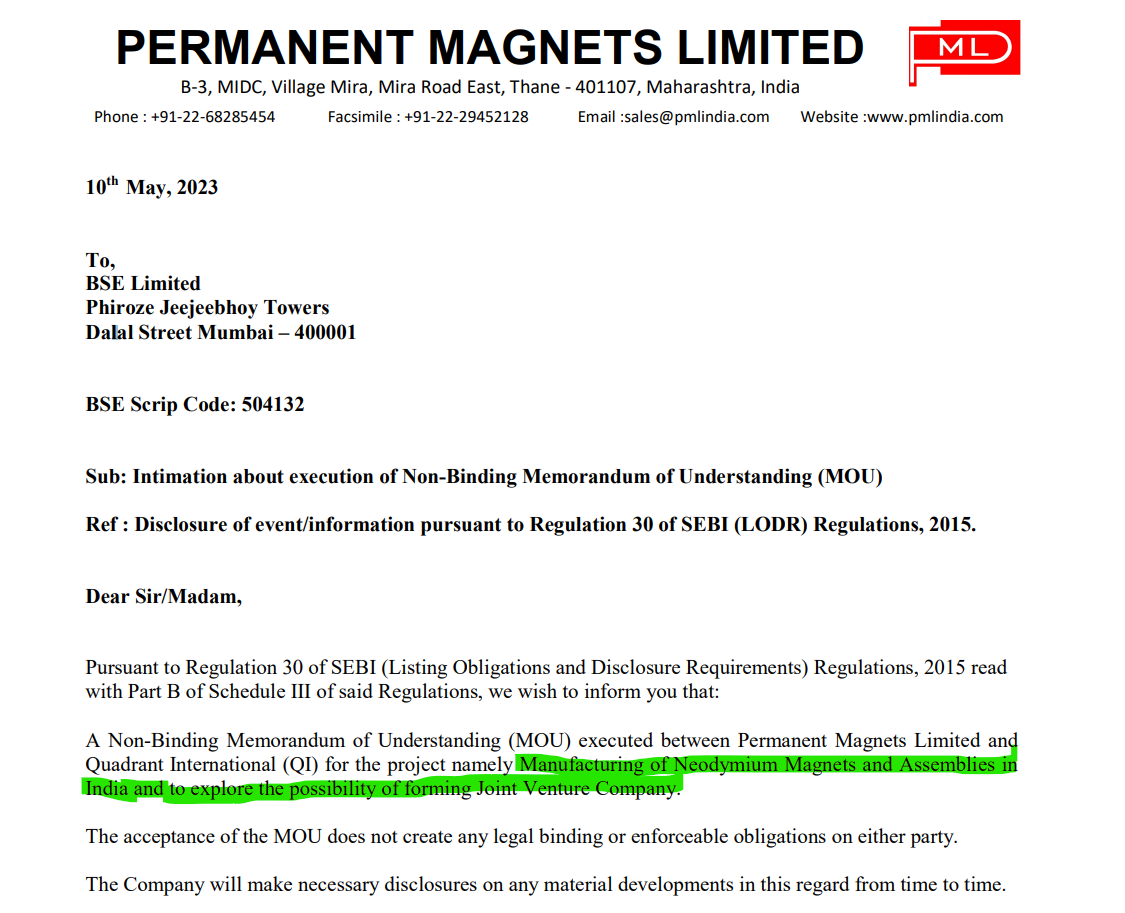

- Taken from today’s notification. This can be an interesting JV if it goes through.

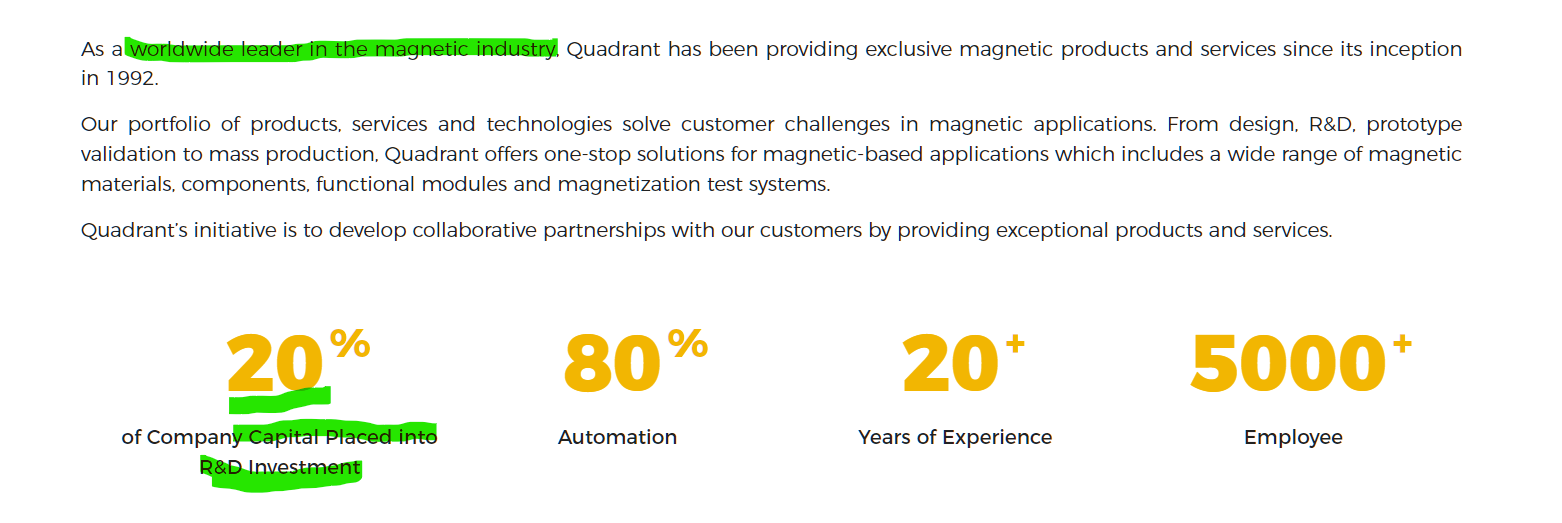

Quadrant seems to be a world leader in magnetics

Even if a fraction of that manufacturing is moved to India, it could be a huge opportunity for PML. PML current imports NdFeB rare earth magnets for its lifters and other appliances it manufactures if am not mistaken. So it could be a good backward integration of a valuable component.

Quadrant seems to be a very good fit for PML in forward components and modules integration as well with its automotive applications. It can all add up so well if this thing works out. I would give the odds for it working out at 5% even if am optimistic.

- Recently came across the last 3 AGM transcripts. I think this helps understand management vision better than even the informative AR. @ankitgupta @ayushmit @desaidhwanil @rohitbalakrish_ have been following this for awhile as can be seen in the transcripts

Incidentally it was @ankitgupta and @rohitbalakrish_ that helped me understand the business late last year after I got excited looking at the AR

-

The land issue queried somewhere in this thread is addressed in multiple AGMs. The land is not developed and the land area is 1,25,000 sqft and PML has a 15% share in it and its value could be 25-30 Cr (I assume this is PML’s interest)

-

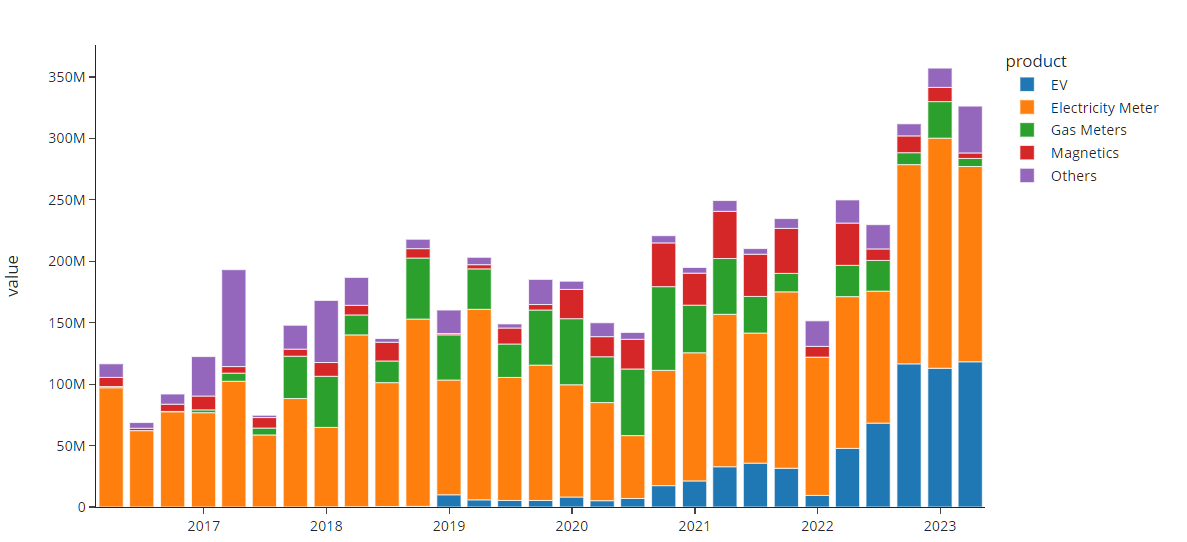

This is based on analysis I did on exports data. It is thus not indicative of complete company profile but what the management has been saying in IR/AR adds up in terms of EV contribution (at least in exports)

The split-up has some assumptions built in from my side and could be slightly inaccurate

What is even more interesting is that unlike the electricity meters business which is lumpy from a few large customers, the EV business is very fragmented and the company has at least 45 unique customers it appears to be dealing with.

(Thanks to @Sanjay_Kumar_E for helping out with data and interpretations)

This part of the business should be fairly robust, unlike the gas meter / electricity meter business IMO.

However, this business has several risks if you go through the AGM transcripts. The feel I get is this like a CRO/CDMO business that works based on projects in the pipeline and some of these could turn out to be big opportunities but there’s no way of saying when current products could go obsolete. When some project becomes big, PML becomes the suppliers until the lifetime of the product. But most of these should be micro/small contributions to the topline like in a CRO/CDMO business. The quarter on quarter numbers also could fluctuate just like one! I see so many parallels but please excuse if this is a stretch

The robustness of this business can only be measured by its “pipeline” and which projects are commercialised and how long their contribution will last, just as in a CDMO (I wish management gave us visibility on the pipeline like how a Neuland labs provides visibility on its pipeline and what stages the projects are at). Otherwise, this is a bet on the management to know what they are doing. So far they are doing really well if you go by @GourabPaul ‘s post above and go through the new website which lists all their products in much great detail. Also, to be able to sit at the table with a giant like Quadrant Magnetics itself is perhaps an achievement

Disc: Invested from 550 levels. No recent transactions. I feel the stock is very expensive at current levels and would think ~700 to be fair value

| Subscribe To Our Free Newsletter |