Salzer, Monthly – Made an ATH today. The previous peak was 332 made in July ’15 (not in chart). Has had a bit of congestion around 300 levels last few months and it has been resistance since start of the year but looks like we might be getting a move on

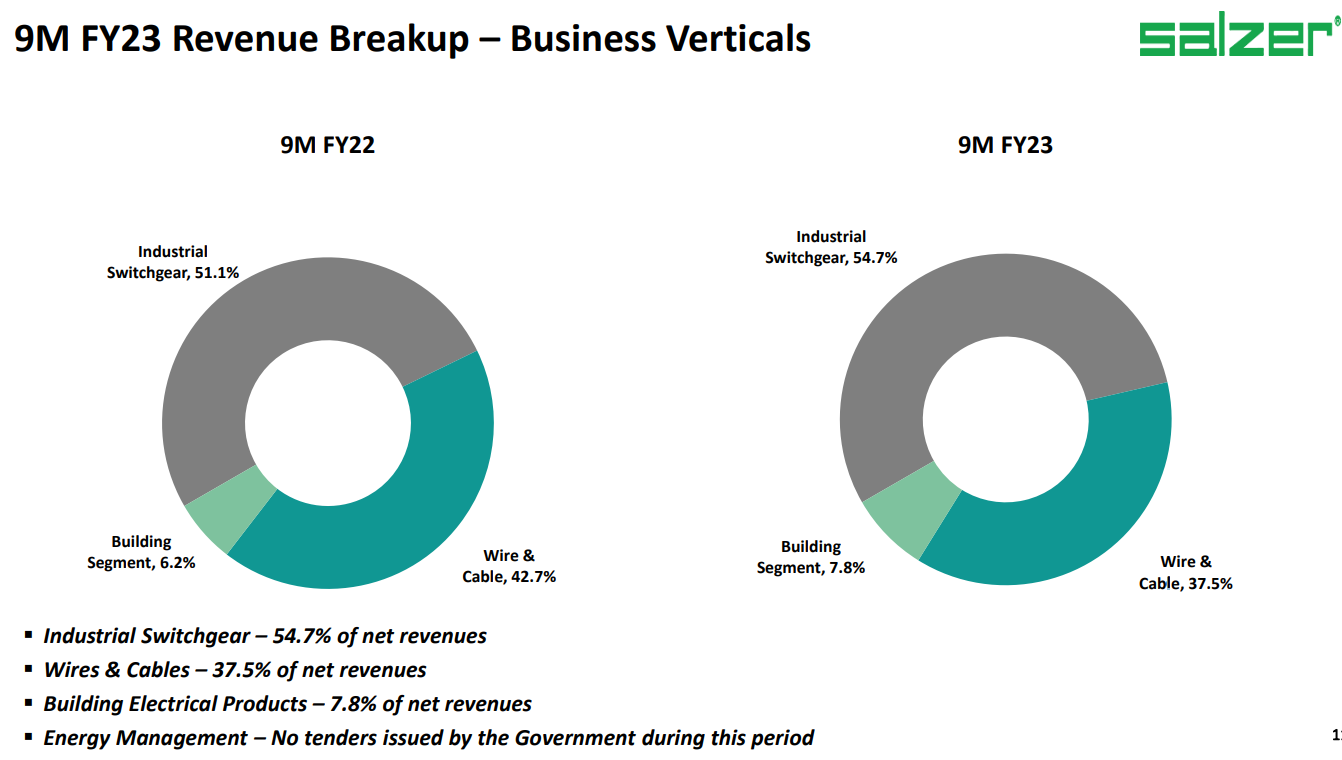

The company makes switchgears (rotary switches, wire harness, toroidal transformers, mpcbs etc), building electrical products (MCBs, modular switches) and also copper products (wires and cables).

The switchgears and building segments is doing well while the wires and cables are being a drag (10% decline YoY)

The wires and cables are also being a drag on the margins of the company as this is a commodity business and it has caused the margins to dip quite a bit of late.

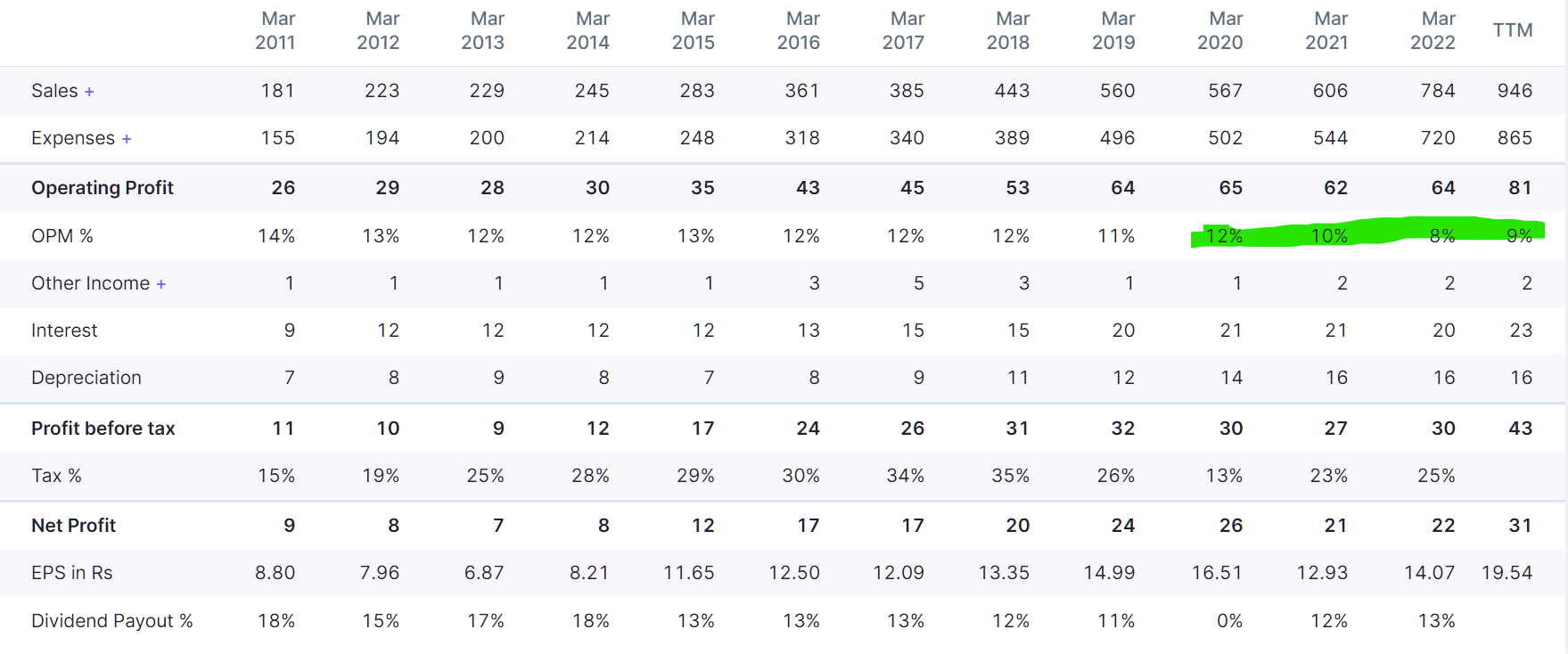

This is however changing and margins as guided by the management should be back to 11% level in a quarter or two at most. Good part is exports are increasing in contribution from 22% to 28% levels YoY for last quarter. Most of the good performance is masked by the drag caused by the wires and cables business which is marred by high inflation and suppressed agri demand and also copper price fluctuations.

So that takes care of the base business performance.

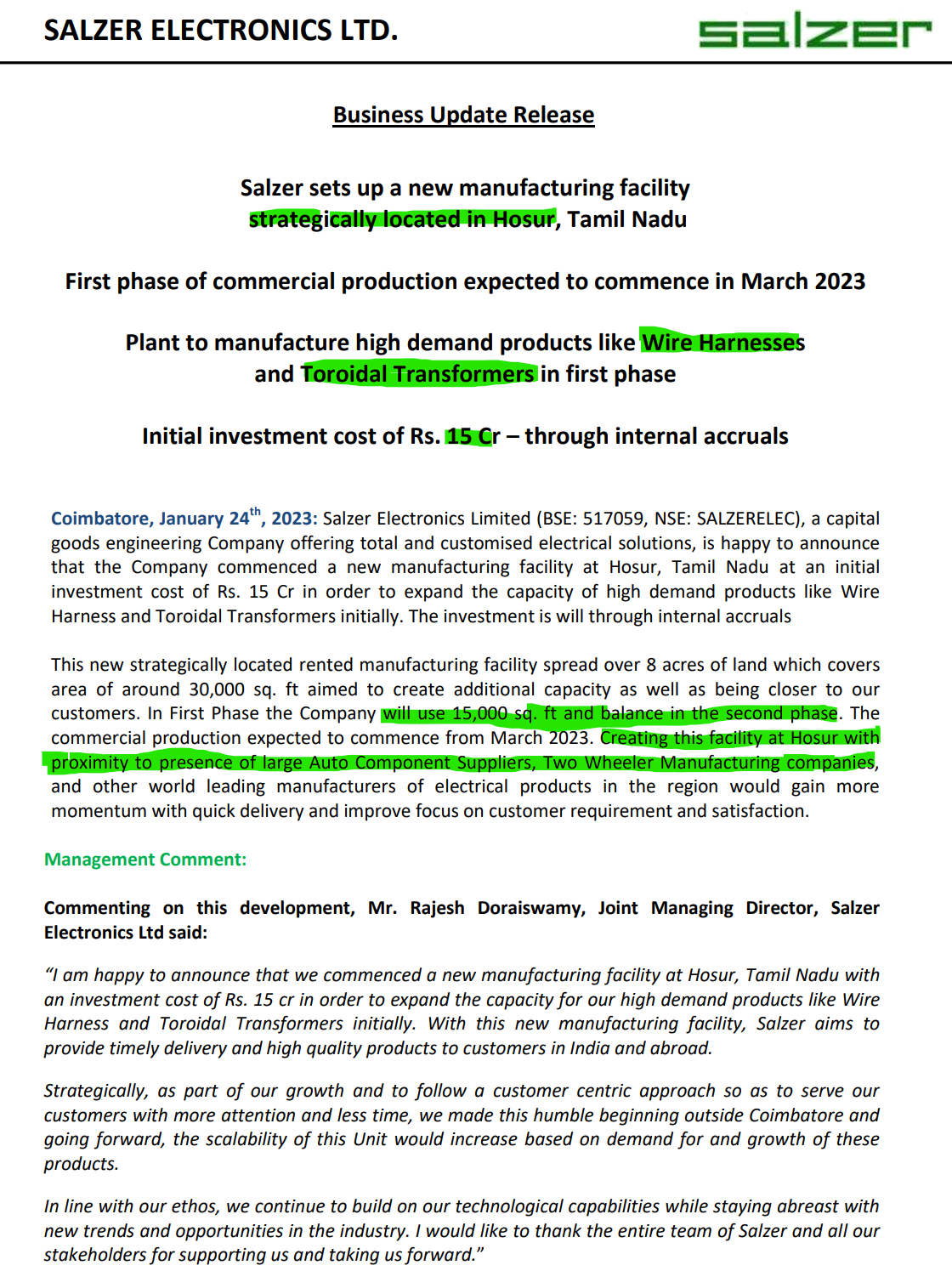

The company is also expanding its wire harnesses and toroidal transformers used in 2W EVs. The proximity to two-wheeler companies here could mean that they are setting this up to supply to Ola and Ather (management hasn’t confirmed though in the call so it is solely my assumption)

This should be the growth kicker from Q1 FY24 (current quarter if it has commenced production as planned). It is also interesting that this company with 5 manufacturing facilities in Coimbatore is for the first time getting out of its comfort zone into another town, signaling its ambitions.

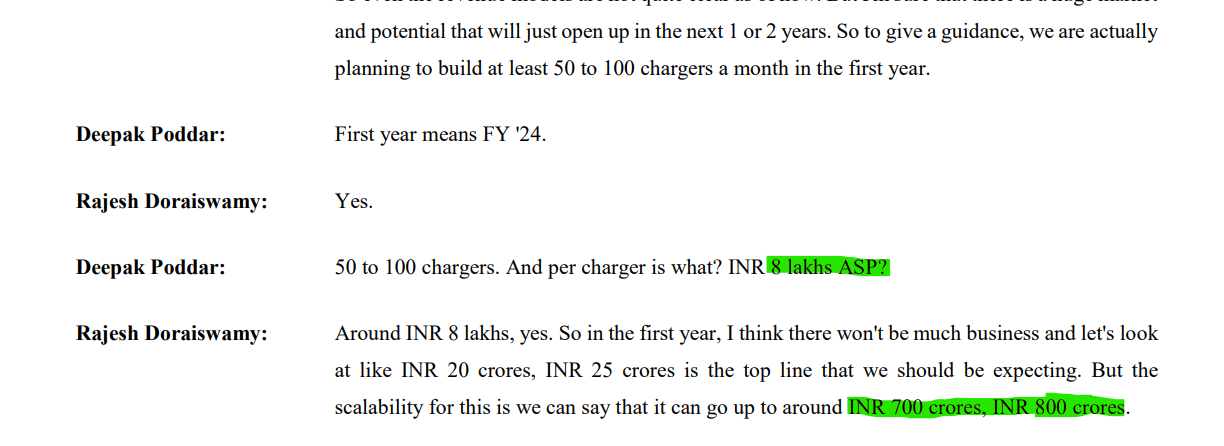

The ambitions are also visible in its JV with Kostad GmbH (26% interest with option to inc it to 50%)

The product is in prototype stage and they are looking to localize as much as possible. But the risk here is that there’s no clear model on how EV fast charging networks are going to be setup here. So I see this more as an optionality while the base business growth and recovery in margins, along with the under-valuation supports the price in the near term.

Unfortunately I was researching the idea when P/E was 13 but actually bought when P/E was 15 and today it already at 17. Re-rating was part of the thesis but it has hit a ATH today so its already underway. I feel Q4 and Q1 numbers should give a direction on the recovery in margins and incremental growth. Commercialisation and clear direction on the fast chargers could be the optionality

Disc: Have positions between 300-310. I am not a registed RIA and just a novice sharing what I find interesting. Please do your own research

| Subscribe To Our Free Newsletter |