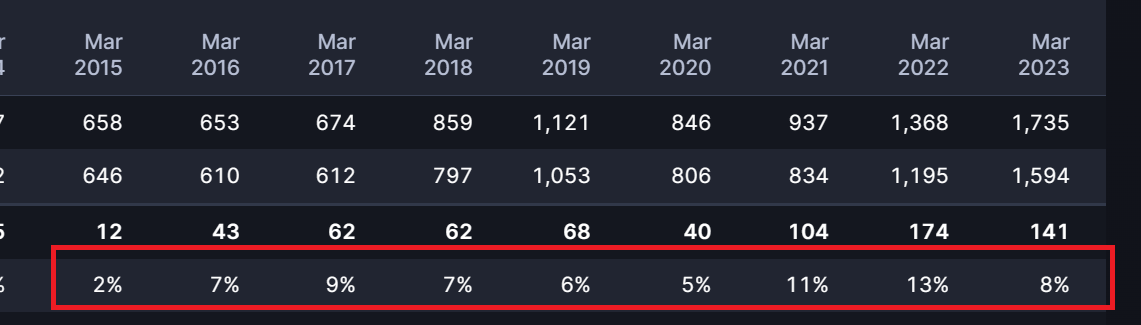

The company did 2 lakh tonnes of sales in FY23 and do not have the capacity to be able to do more than 2.3 lakhs in the next 3 years, nor do they seem to have any capex plans to increase capacity.

Therefore from a topline perspective, we are looking at a maximum upside of 30% in the next 3 years. So any meaningful upside over and above this can come from increasing realizations / margin expansion. With regards to margin expansion, I have my doubts as the commodity upcycle is now ebbing and commodity players are bracing for a period of normalized margins. If you look at Vardhman’s historical margins, they have been in the range of 6-7% barring the commodity upcycle seen in FY21 & FY22 where the company witnessed margins of 11% and 13%.

| Subscribe To Our Free Newsletter |