Logically one would think it would be the latter. One cant pay tax on a legacy loan repayment amount

(For Capital gains calculation one would consider only the distribution received as loan repaid. For distribution tax calculation one needs to take historical aggregated value). Please suggest if this is the wrong interpretation

Below article gives an example

So the benefit of loan repayment exemption gets neutralized at the time of sale of units thru a higher capital gains tax amount (as the purchase value comes down)?

Quoting from the article

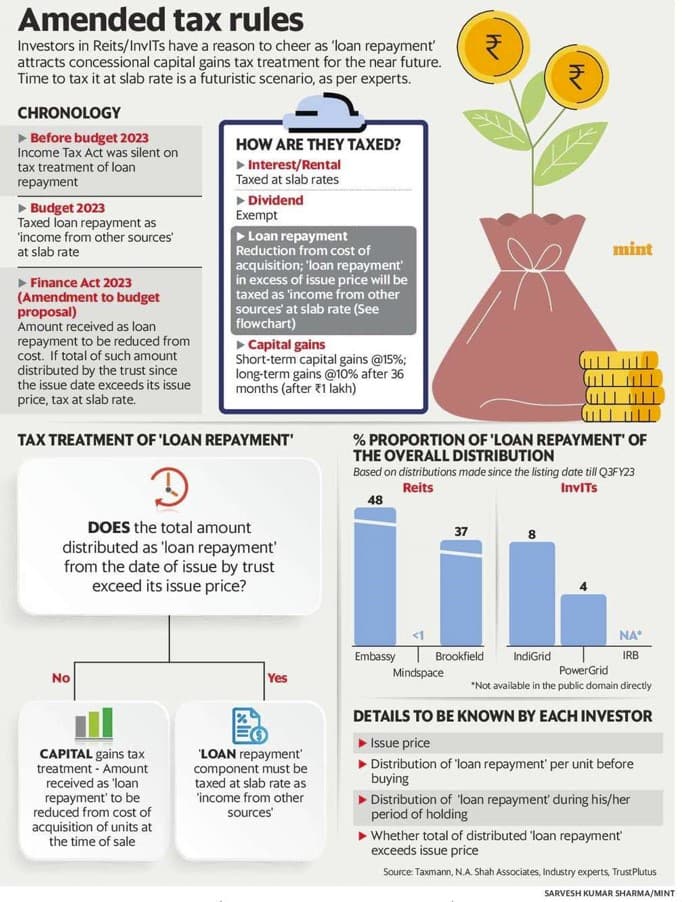

“The amended tax rules indicate that the amount received as ‘loan repayment’ must be reduced from the cost of acquisition at the time of sale of unit by the investor.

For example, you bought a unit of a reit at ₹400 and sold it after 3 years at ₹500 in the secondary market. During the period of your holding, say, the reit distributed ₹50 as ‘loan repayment’.

To calculate capital gains at the time of sale, you need to reduce ₹50 from your cost of acquisition of ₹400, which would come to ₹350 per unit. Thus, your capital gains will be ₹150 per unit ( ₹500 – ₹350) and not ₹100 ( ₹500 – ₹400).

Effectively, the loan repayment component will be taxed as capital gains at the time of sale of units.

But that’s not all. Just like with every tax rule, this provision is not without ifs and buts.

The capital gains tax treatment for ‘loan repayment’ component is not forever. It is only until the total of such amount distributed by a reit/invit doesn’t exceed its issue price.

For instance, the issue price of a reit/invit unit is ₹300 per unit. Say, you bought a unit of a trust when the total of ‘loan repayment’ component distributed by that reit/invit (from the issue date, not from the day you bought) just exceeded ₹300.

Any distribution that you will receive in the form of ‘loan repayment’, irrespective of your holding period, will be considered as income from other sources, which attracts tax at the slab rate in the year of receipt of such income.

But your predecessor, who held the unit before the sum of ‘loan repayment’ by the trust exceeded ₹300 (issue price), would be eligible to adjust such income from the cost of acquisition and treat it as capital gain at the time of sale of unit.

Now, a doubt might arise to you on how you as an investor would know whether the reit/invit distributed ‘loan repayment’ in excess of its issue price or not. That’s where the disclosures from companies come into picture. The industry players are still unsure of how, what and when such details must be disclosed by trusts and awaiting a clarity from the government.

Having said that, industry experts believe that investors need not worry about it much. This is because they opine that it would take minimum of 15-20 years for the existing trusts before the total amount paid as loan repayment exceeds its issue price.”

| Subscribe To Our Free Newsletter |