Background:

- 160+ years old Engineering conglomerate.

- Transforming from traditional (stagnant growth) engines and auxiliary power systems business to fuel agnostic powertrain, electric vehicles (2W, 3W), aftermarket spares & retail solutions.

- Business owns 6 manufacturing locations and is supported by auto aftermarket network with 8000+ retail outlets, 20000+ mechanics and 350+ dealer touch points.

Key products/services:

- Automotive Engines: Diesel & CNG engines for 3W and small 4W.

- Non-Automotive: Farm Equipment (Portable Engines, Portable Pump sets, Power Tiller, Reaper, Rotavator), Portable Gensets 5 to 7.5 KVA and Industrial Gensets 10 KVA to 1250 KVA, and Industrial Engines.

- Retail outlets: One stop shop for Sales, Service & Spares (3S). Consists of AutoEVMART, Greaves * Care and Greaves retail.

- AutoEVMART: National multi-brand EV retail. 150 Stores.

- Greaves Care: Multi-Brand service. Service and Spares of the major brand for 3W, commercial and passenger vehicles. 170 Stores.

- Greaves Retail: Spares Sellers. 8000+ stores.

- Greaves Electric Mobility (GEM): Manufacturing and Selling of Electric 2W & 3W. Ampere (E-scooters), ELE (E-Rickshaw), & Teja (E-Auto). EV manufacturing facility and an Experience Centre at Ranipet, TN. Acquired Ampere brand in FY20. Ampere ranked amongst India’s top three electric vehicle manufacturers in FY23.

- Greaves Finance: Finance options to electric vehicle buyers.

What’s Interesting?

- In 2017, business-initiated steps to establish itself as a leading fuel agnostic powertrain solutions & services company, recognizing electric vehicles as an upcoming large opportunity.

- Past revenue used to be 100% B2B. However, 66% revenue of Q4FY23 66% came from B2C. This shall lead to overall margin expansion once GEM division attains scale.

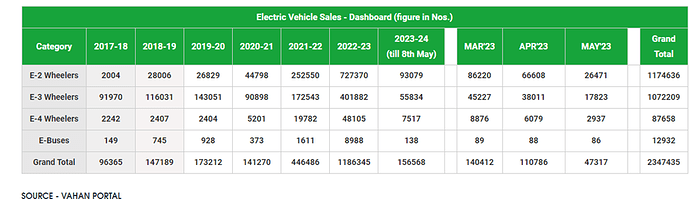

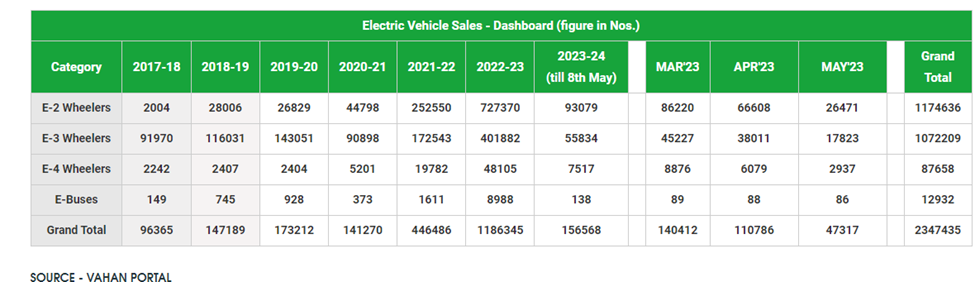

- The significant growth opportunities for E-Mobility businesses considering governments push for EV adoption. Below snapshot shows the trend of the last few years:

Source: SMEV EV Industry

How I expect numbers to trend?

As a base case, I expect that consolidated margins would double from current 5% and Sales, EBITDA & PAT would grow at CAGR of 13%, 29% and 28% respectively for the next 5 years as the business would earn most of the revenue from B2C channels, which will scale up with time due to huge opportunity and sectoral tailwinds. It will be great to hear counter views from far reaching minds on this aspect.

(Details are shown below).

| Revenue | FY23 | FY24(E) | FY25(E) | FY26(E) | FY27(E) | FY28(E) | Exp. CAGR |

|---|---|---|---|---|---|---|---|

| Engines | 1015 | 1015 | 1015 | 1015 | 1015 | 1015 | 0% |

| Retail Spares+Care+Evmart | 535 | 589 | 647 | 712 | 783 | 862 | 10% |

| Excel Controlinkage | – | 200 | 220 | 242 | 266 | 293 | 10% |

| Electric Mobility | 1124 | 1349 | 1619 | 1942 | 2331 | 2797 | 20% |

| Consolidated | 2674 | 3152 | 3501 | 3911 | 4395 | 4966 | 13% |

If ‘Electric Mobility’ assumed CAGR of 20% materializes, business would sell 2.5 Lacs vehicles from their current production capacity of 5 lacs. As a base case, I assume that ‘Electric Mobility’ penetration would grow at the rate of 20% and Greave/Ampere would at least defend its current mkt share (~12%) over the next 5 years.

| OPM | FY23 | FY24(E) | FY25(E) | FY26(E) | FY27(E) | FY28(E) | |

|---|---|---|---|---|---|---|---|

| Engines | 8% | 8% | 8% | 8% | 8% | 8% | |

| Retail Spares+Care+Evmart | 20% | 20% | 20% | 20% | 20% | 20% | |

| Excel Controlinkage | – | 25% | 25% | 25% | 25% | 25% | |

| Electric Mobility | -5% | -2% | 0% | 3% | 4% | 5% | |

| Consolidated | 5% | 7% | 8% | 9% | 9% | 9% | |

| EBITDA | 132 | 222 | 266 | 342 | 398 | 467 | 29% |

| Other Income + | 55 | 55 | 55 | 55 | 55 | 55 | |

| Interest | 12 | 13 | 15 | 16 | 18 | 19 | 10% |

| Depreciation | 57 | 63 | 69 | 76 | 83 | 92 | 10% |

| Tax % | 25% | 25% | 25% | 25% | 25% | 25% | |

| PAT | 118 | 201 | 237 | 306 | 352 | 410 | 28% |

Risk & Concerns:

- Diesel parts business may remain stagnant or decline.

- New entrant in 2W and 3W industry as an OEM.

- Recurrent Executive Directors and CFO churn.

- EV manufacturers are yet to breakeven at operating level. To maintain level playing field with the competition, margins of the GEM division would remain under pressure in the near term.

Disc: Not Invested Yet.

| Subscribe To Our Free Newsletter |