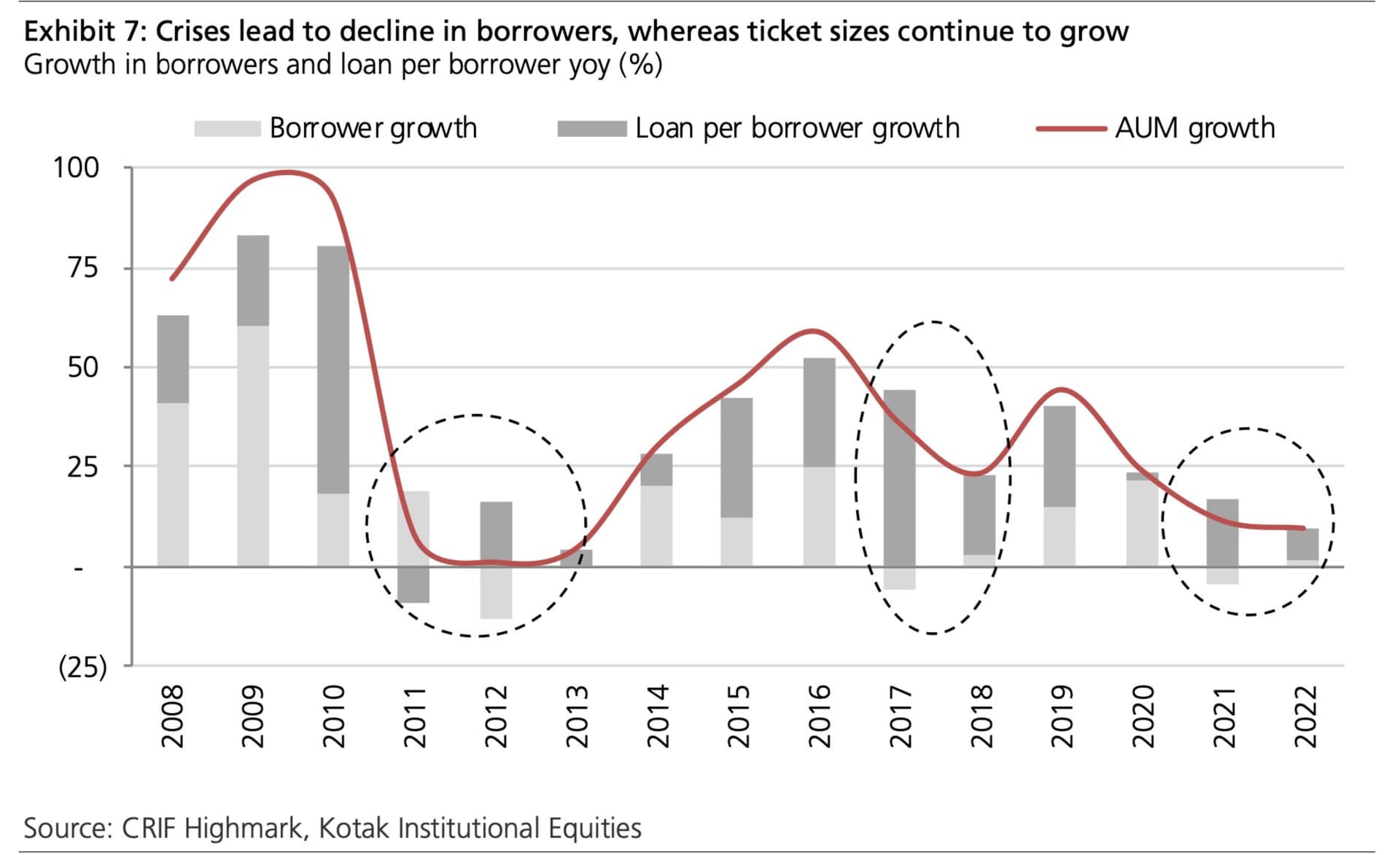

Positive Microfinance Cycle which might be accelearating

In last 13 years, we have seen 3 Negative cycles of Micro-finance and 3 positive ones.

Purpose of the post is to see where do we stand in the current cycle?

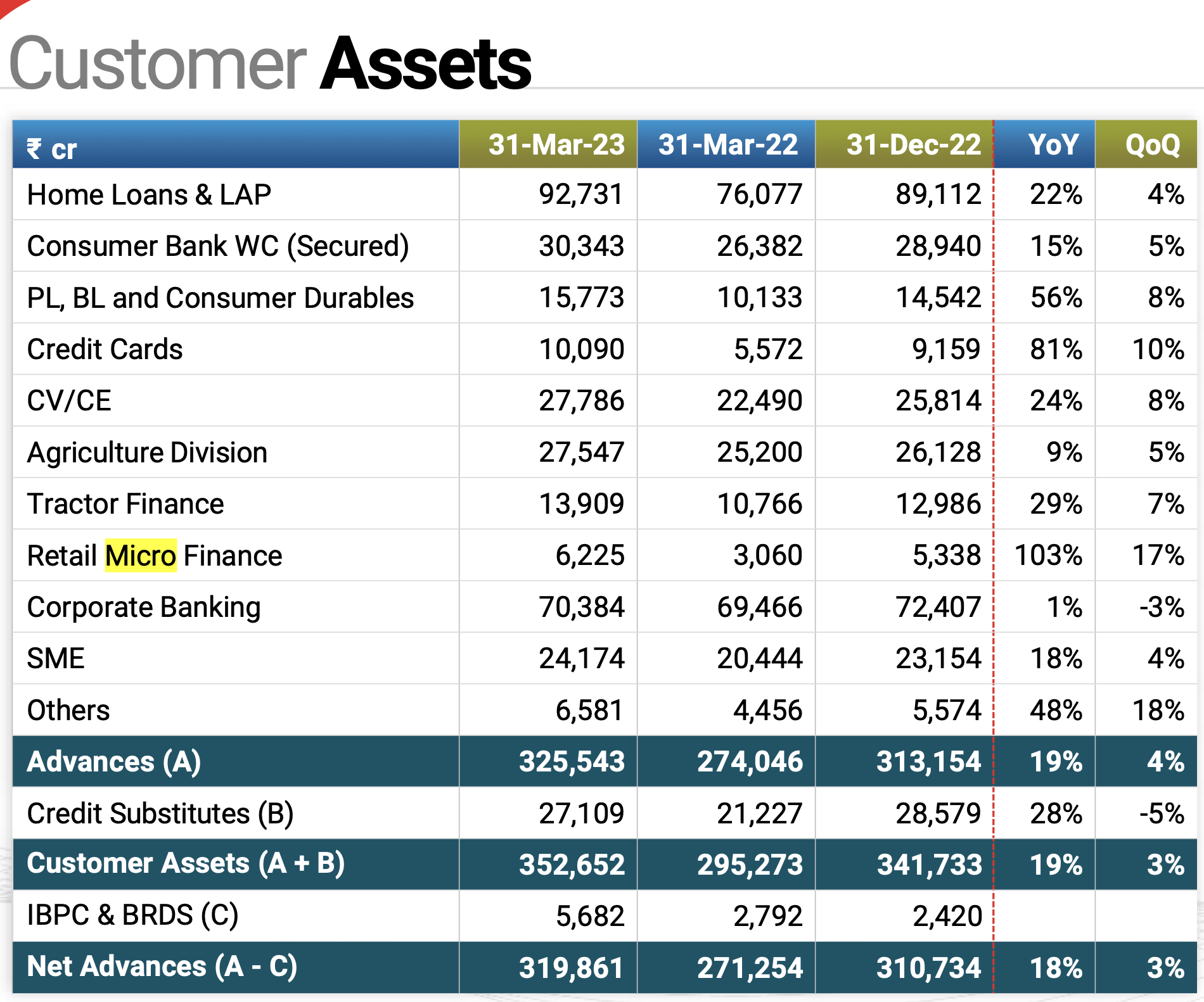

- Starting with the numbers of one of the most conservative lenders that is in the listed space:- Kotak Mahindra Bank

Kotak acquired BSS in 2017.

This year Kotak has grown advances by 103% YOY in Mirco-finance.

UDAY KOTAK IN Q3 CONCALL

We are happy to announce that our retail microfinance business crossed the 1 million customer mark during this quarter. Collection efficiencies in this segment are holding up very well, and which shows the ability of the customers to honor their repayments. We see good credit demand in the rural economy, and our MFI business is well poised to leverage this for the coming quarter. We have expanded our presence into 3 new states, Gujarat, Rajasthan, and UP apart from where we are, which is Karnataka, Bihar, TN, MP and Maharashtra. There is a large unserved market that requires access to formal credit, and we will focus to continue our growth with the same risk-adjusted returns that we see.

Pat of BSS has gone from 83 crores to 293 crores. Asset quality has been pristine.

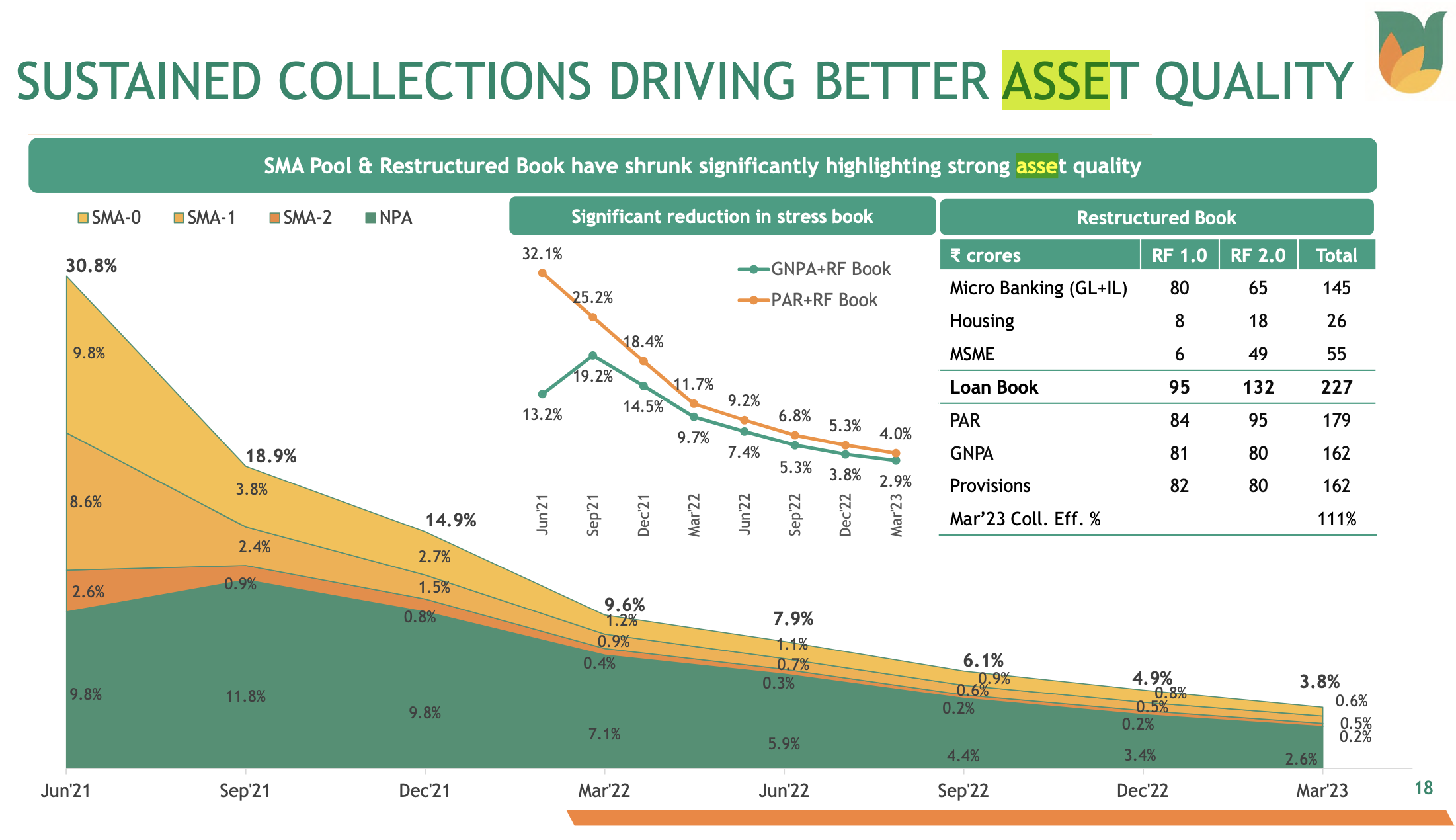

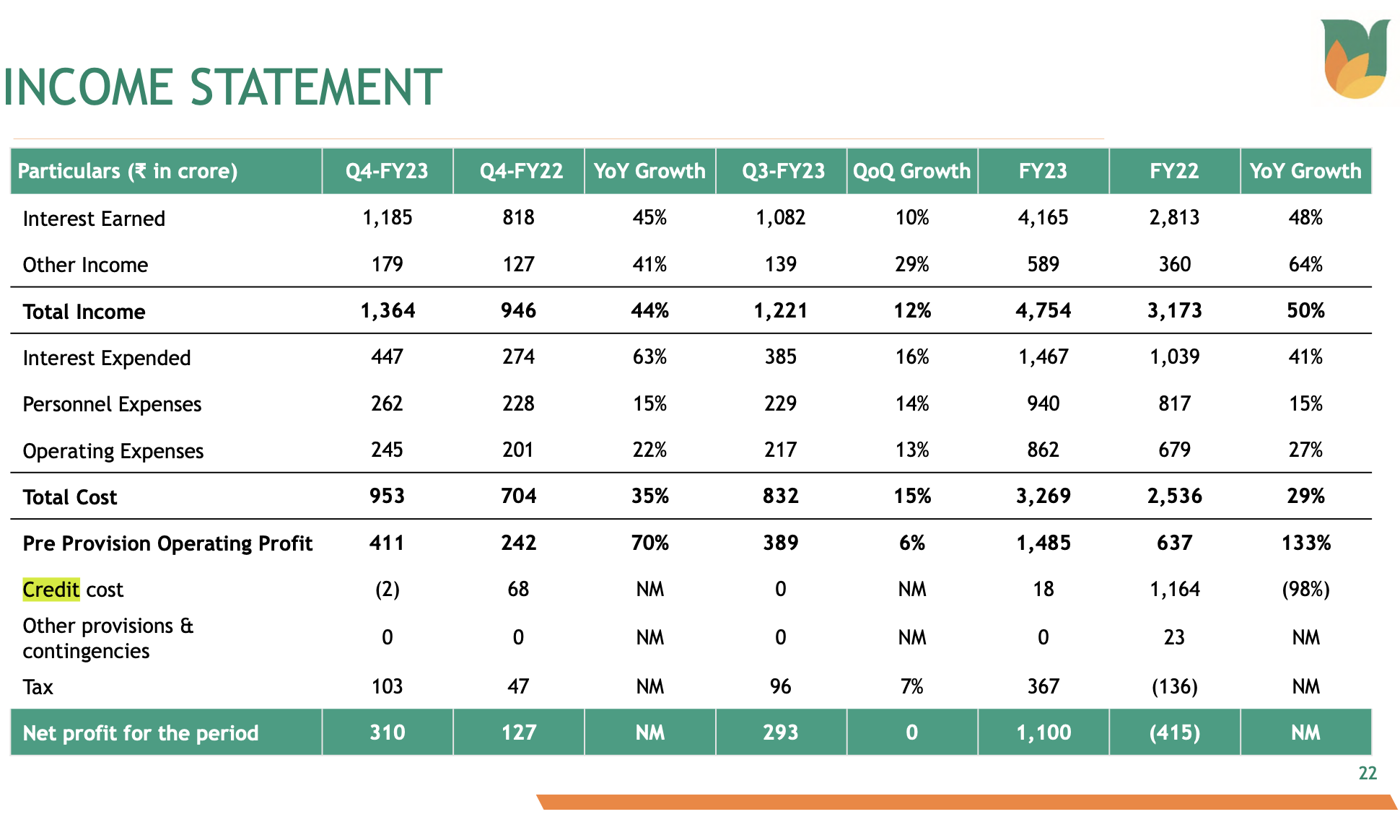

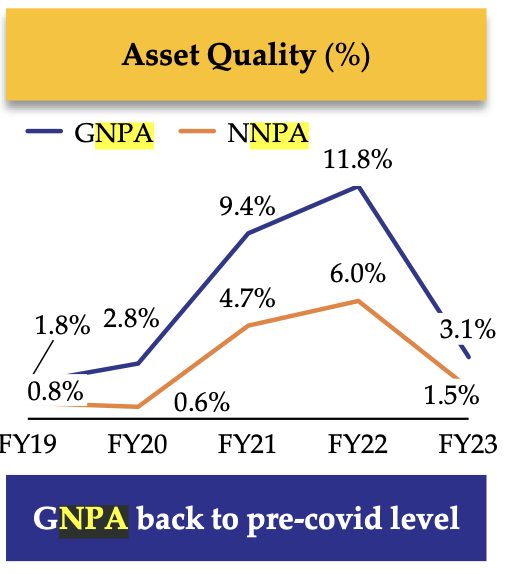

- Coming to one of the lenders which reported losses during covid time and is now reporting negative credit cost with improving asset quality and trajectory:- Ujjivan Small Finance Bank

SMA BUCKET 0,1 & 2 Have normalised and fallen below pre covid levels.

Lets look at the NPA’s:-

NNPA is barely at 0.04%.

The ultimate hallmark of pristine asset quality for the time being can be seen in the credit costs Ujjivan has been reporting (Possibly due to write backs)

- Survodaya which has reported high GNPA’s in the past has also started seeing both GNPA’s and NNPA’s fall.

At the same time gross advances have grown at 20%+ YOY.

- Lenders with past governance issues like Spandhana Spoorty have also started reporting reduction in NPA’s.

Moreover they have started growing their AUM aggressively.

- Finally, the removal of Yield caps on Microfinance NBFC’s will help them to price the risk better and open up a vast majority of the sector which was untouchable. This is one of the reasons why Micro NBFC’s sound very confident of maintaining their NIM’s in FY24. Eg;- Nirmal Jain in IIFL’s concall pointing to increase in PF yield for Mfin loans.

Disc: Playing the cycle, and invested in Ujjivan Fin at 250, Arman at 800s. No reco to buy or sell.

| Subscribe To Our Free Newsletter |