Quality Growth

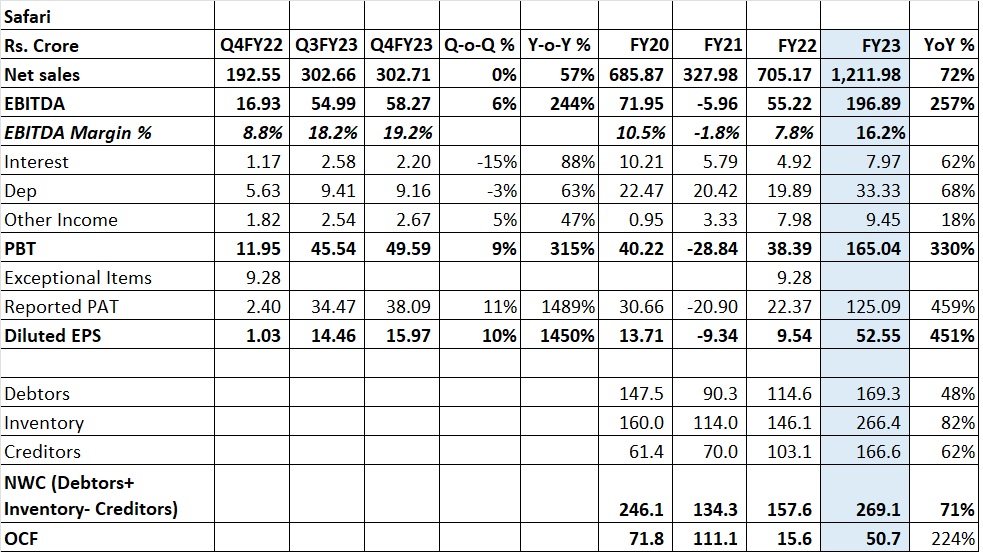

Quantitative growth has been a consistent track record of Safari (except for covid period). However, growth quality in terms of industry leading margins and positive OCF come as positive surprise. I think benefits of capacity expansion and operating leverage are yet to playout as margin expansion seems to be more due to change in sales mix and decline in input costs. This could provide buffer for continuation of aggressive sales strategy in future. OCF/EBITDA for FY23 optically looks low; this is still good considering 72% revenue growth during the year and cumulative OCF of Rs.249 crore for FY20 to FY23, which is 78% of cumulative EBITDA. I believe both Industry leading margins resulting in earnings multiplying and positive OCF during last 4 years despite high growth trajectory are beyond anyone’s expectations (including mine).

Between FY19 to FY23, VIP’s revenue has grown just 1.17x times and Safari has grown 2.1x. Safari has proven itself on all the counts and market has rewarded Safari for the outperformance. While believers of VIP still have faith due to its leadership position, market has differentiated due to muted revenue growth and loss of market share.

What Next?

- Further capacity expansion, built up of large inventory base (Rs.266 cr as on March 31,2023) and industry tailwinds indicate possibility of continuation of growth trajectory

- Possibility of superior OCF growth on low base

- Operating leverage from increased share of inhouse manufacturing and overall size

- Stated intent to enter into premium category opens up new growth avenue

Key Risks

- Increase in input prices in future

- Any moderation in industry growth

Disc: Invested. I am not SEBI registered Advisor/Analyst. The information provided above is for education purpose only.

| Subscribe To Our Free Newsletter |