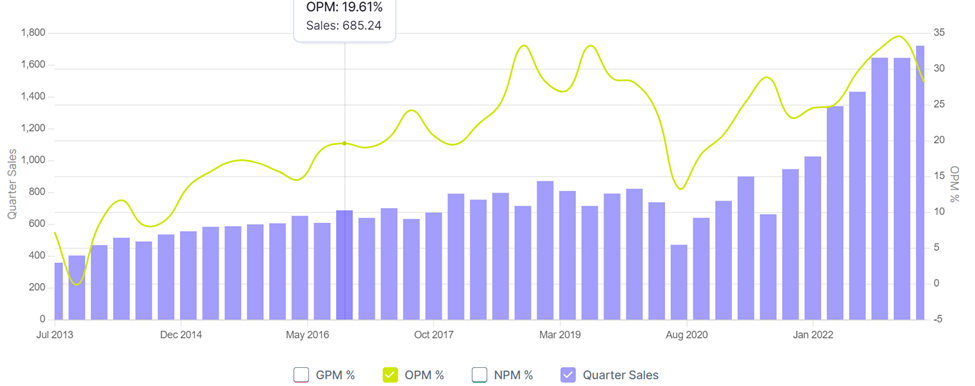

OPM margins were down to 28 % from 34 % on a QoQ basis. Share prices have dropped from a peak of Rs .447/- on August 22 to 366 as of yesterday ie, 17.05.23. So far it is perfectly following the usual cyclical understanding that price peaks before the peak margins and signaling the end of a cycle.

The landed cost of imported paper is usually the largest dampener to the paper industry in India. As discussed, there are two things that affect the cost of imported paper. 1) Pulp price. 2) Cost of transport or shipping costs 3) Import duty.

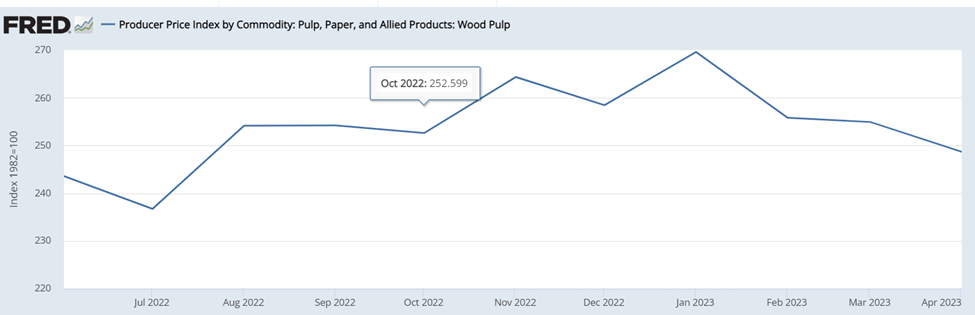

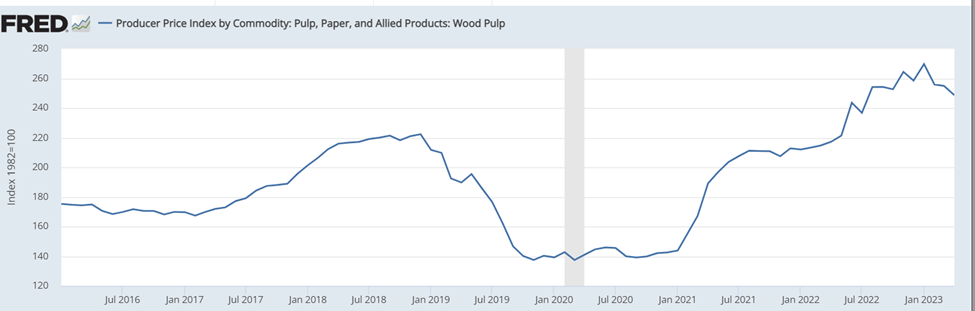

Pulp price is indicated by pulp price index

The pulp price index has come down to 248 as of April 23 from a peak of 269 on January’23. So, considering the pulp price index alone margins may come down further in the Q124.

However, it’s still far better than the peak we saw in 2018.

The company in its earnings release indicated that the selling price of some products has reduced in Q423. It also mentioned some other costs are reduced (No idea what it is)

Shipping costs

Shipping costs have fallen drastically over the past 1 year which makes import more competent. However, it may aid the company with more export opportunities. As per India Ratings, JKPL increased its export volumes 7% yoy in FY22 (constituting 12% of sale volumes), with increased opportunities in overseas markets amid global supply disruptions and rising pulp/wastepaper prices.

New Capex and acquisition of corrugated box manufacturers

JKPL acquired two corrugated boxes manufacturing companies Horizon Packs Private Limited (HPPL) and Securipax Packaging Private Limited (SPPL) in December 2022 that are leading players across seven locations in North, West and South India. Also, it has started trial-runs at its greenfield corrugated boxes plant in Ludhiana (in subsidiary JKPL Packaging Products Ltd) which is likely to be commercialised in March 2023. JKPL’s overall volume are likely to witness strong growth in FY24 as well, as additional volumes come from the entry into corrugated boxes along with higher packaging volumes.

JKPL acquired HPPL and SPPL in December 2022 for a consideration of INR5.8 billion, funded by internal accruals. Apart from this, the company is setting up a corrugated boxes capacity in Ludhiana, Punjab, for which it has already incurred about INR1.4 billion and could incur another INR0.3 billion in FY23. Other than this, no major expansionary capex is planned as per the management.

Source: India ratings Jan’23.

As per the earnings release, the company mentioned only that the operation of corrugated box manufacturing is satisfactory. No mention of any capacity utilization.

Increasing FII shareholding.

Source: Screener

It is interesting to note that FIIs have been continuously increasing their shareholding for the past 3 quarters.

Debt Repayment

The consolidated debt came down from 3079 crores to 2803 crores. Interest on a QoQ basis has come down to 63 crores from 94 crores. Adding depreciation to net profit = 365 crores. The company does have the cash flow to reduce the debt significantly. The company hinted at accelerated debt repayment in August’ 22 con call. But went on to acquire 2 corrugated box manufacturers for 586 crores. With this acquisition, the company is however able to further diversify its products.

The company’s OPM margins since 2016 haven’t fallen below 19 % even at the bottom of the cycle except for 2020.

Margins may further dip in the next quarter, but I expect the company to have good cash flows to pay down the debt. FIIs increasing the stake in the company is interesting.

Discl: Not invested. Just trying to learn about the company.

| Subscribe To Our Free Newsletter |