Hi guys this is my first chemical company analysis so please pardon me incase my understanding of few concept is wrong. So let’s begin

CAPEX

A. Problems During large capex

-

There can be a delay in capex and the cost estimates can be wrong. So in Deepaks case this has already happened so in my view it is already priced in. One of the major reason for this was they bought land close to the main road which was expensive than the land 1 to 2km away for main road and the conversion of land to industrial land. So expensive land and delayed conversion.

-

If you are doing backward integration for RM how competitively can you make the RM, how critical it is for your business, do you have any experience. So in short above in the thread we have seen how critical the RM is ( it is close to 80% of their entire RM used across different vertical) they already have experience of making ammonia.

How competitively?

So ammonia is made from natural gas and Deepak will buy NG internationally in the form of LNG(Liquefied Natural Gas) and domestically. So a company who has a factory in Middle east has access to cheaper NG and hence they can make it more competitively. But as per management the economics are in their favor such that it is as good as buying NG at middle east rates.

So as per management the ammonia capex cost is 20% to 30% lower than somebody who would have done In middle east and the economics are in their favor such they are buying NG at middle east rate. (will explain later in detail)

- Who is using the RM. In deepaks case 100% is being used for internal use. (Big advantage)

- DEBT- So in their case they take long term debt of more than 10years in this kind of setup the burden to pay principle is very low so their basic cash flow generating ability should be able to handle this. Their next three year obligation is very low as per management.

- Commissioning, scaling and stabilizing. In deepaks case the plant will start commercial production from Q2 and in this FY it will run for 9 months at 75% to 80% utilization. DFPCL Ammonia Project Update (April 2023) – YouTube ( Status of plant as on april)

The engineering of this plant has been done by TOYO a 80year old Japanese company and here are few of it past projects.

They are pretty experienced and the contract with Deepak fertilizer is a performance guarantee contract where TOYO will have to prove the capacity, purity, efficiency. I am pretty confident that the project will be running by Q2 FY24 commercially. I my view there will be now commissioning issue.

These are majorly all the problems a chemical company can face when doing large capex .

B. Ammonia economic and GAS

Economics per TON

- They are going to save anywhere between 80$ to 90$ on logistics.

- They are going to get 9% of SGST refund of the transfer pricing from ammonia plant to the consumption plant. So basically 9% of ammonia price per TON. So if ammonia is 500$ then they will get 45$

- Since this is an exothermic activity the ammonia plant will release a lot of energy which will be used in their TAN plant which is close to 10$ to 15$ of savings per TON

- The difference between the GAS price and ammonia price

- This entire projects adds 200cr of interest cost and close to 110cr of depreciation ( as per Q4 concall)

- They have 25$ to 30$ of other expense which is basically to run the plant.

So if you take ammonia price of 450$ then all the additional benefit will be close to 140$ so when you convert this 140$ in LNG terms it comes out to be 3.5$ to 4$ and on an average gas prices have been 8$ to 8.5$ hence it is as good as buying gas at 4$ to 4.5$

GAS

First let us understand the relation between ammonia and gas. With my limited understanding ammonia demand is most of the time going to be there and will grow at a certain % the supply side disruption is the major reason for price fluctuation.

During Russia war gas prices went up pretty fast this lead to most of the ammonia factory shutting down in Europe GAS is RM hence ammonia shortage prices went up. Now GAS prices came down factory opening, ammonia oversupply hence ammonia price down. Now there has to be a certain margin in producing ammonia. Like if gas is 100$ ammonia has to be 110$ whenever there is disruption in this margin the supply side adjust. GAS is more volatile and ammonia price take time to adjust hence we see these cycles. Like in the above example now ammonia price are so low that the margins are again being affected.

China also plays a role here being a large supplier. So there has to always be a spread between

ammonia and gas other we would keep seeing the cycles.

I don’t know how relevant the above table is it came from chat GPT

They have tied up close to 68% of GAS requirement and they will do it for balance as well before commissioning

As per management for 10$ of LNG landed cost on per TON basis is 330$ (conversion and freight included)

So current Gas price is 11$ to 11.5$ landed which is close to 360$ to 375$ on per ton basis and the current ammonia price FOB Middle East is 280$. If I include all the benefits as on date the ammonia realization will be 410$ and their operational cost is 25$ to 30$ so they are at break even.

So as per above logic this should be the case with other global manufacturer as well so now either gas has to fall or ammonia rise but definitely they are in a down cycle

THIS IS ONE OF THE BIGGEST RISK FOR ANY CHEMICAL COMPANY DOING CAPEX BECAUSE THEY ARE AT BREAK EVEN BUT THEY HAVE INCREMENTAL DEPRECIATION AND INTEREST OF 310CR. DESTRUCTION OF P&L

Currently in domestic market ammonia is selling at 50% to 60% premium.

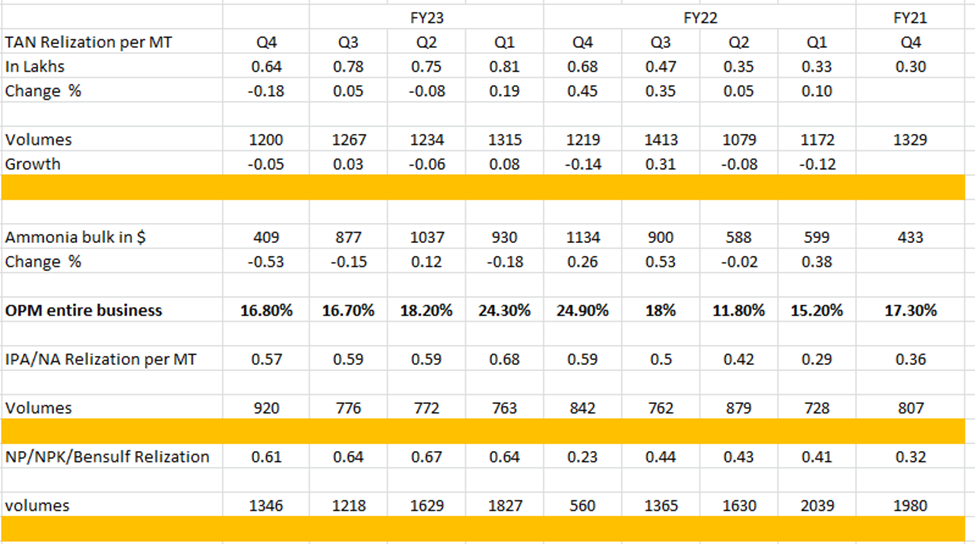

Q4 ANALYSIS AND ROAD AHEAD

In the above table see ammonia Price chance and TAN realization change with 1 quarter lag.

- Like in Q1 Ammonia up by 38% but TAN up by 5% margins at 11.8%. FY22

- Q2 Ammonia down by 2% but in Q3 TAN up by 35% margins 18%. FY22

- In Q4 TAN down by 18% and in Q3 ammonia down by 15%. FY23

- In Q4 ammonia down by 53% so in Q1 FY24 TAN can be down by 50% to 60%

.

Just a small point that even if TAN moves up or down by less percentage than ammonia it will in absolute terms create a positive effect in up move and negative in down move.

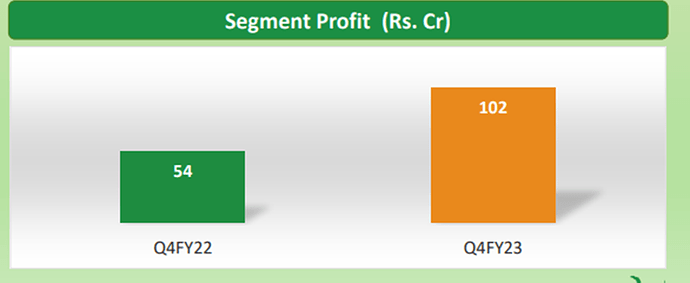

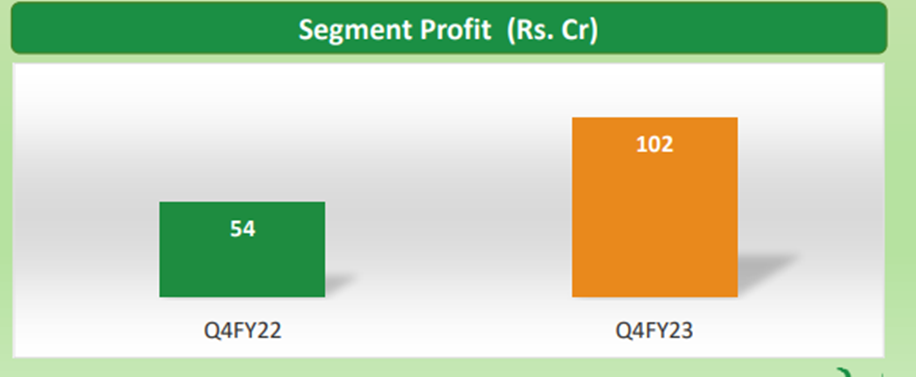

In Q4 the margins have improved by 10bps and they have performed more than my expectation but HOW?

-

IPA in Q4 has performed phenomenally because Safeguard Quantative Restriction was imposed on IPA dated 31st March 2023 by Directorate General of Foreign Trade. This means IPA cannot be imported now

-

Fertilizers segment benefits with falling ammonia price and this segment has also performed exceptionally

MY TAKE

-

They have entered down cycle and next quarter can be a horrible quarter we saw that in Q4 ammonia is down by 53%. So let’s see how much can IPA, Fertilizer rescue the TAN, Like if you see Q4FY21 and Q1FY22 TAN realizations were almost 50% down from current level and margins were between 15% to 17%. if they can give in these lines then it is good.

-

Ammonia plant looks like more of a burden this year than creating value but we tried to see the economic cycle so as per me either GAS has to fall or ammonia has to RISE. Will take time nobody can predict

-

They are making a lot of efforts on Steel Grade, Solar grade acids they are also working on TAN as a solution rather than product and as per them this solution will give them premium margins.

-

Technical

500 is a big time time support and 300 to 400 the sub sequent support looks like we can see 300 to 400 levels in the coming time unless we have a rally in ammonia or fall in GAS price

Overall the possibility of operational or commissioning issue looks low but the economics are not favorable for them. Lets see like they are saying domestic price are up by 50% to 60% so they can also sell some ammonia.

Thankyou

| Subscribe To Our Free Newsletter |