Personally, I find it quite hard to form a “10-year picture”, at least I wouldn’t in the case of Sandur. When I started buying at 700 levels, it seemed like a deep value bet trading at <1 Price to sales (most of the other valuation metrics were also close to multi-year lows; it still looks cheap to be honest). The biggest overhang was that of the Mining Expansion approvals, which have been cleared now.

I think it’s fine if we get the picture “roughly right” – with Sandur’s expansion in the mining segment, approvals in place, DI pipes capex with the strategic thinking of getting preference when the mines are up for re-auction, cheap valuations- things look mostly good in the coming 1-2 years given that the management executes well and there are no major screw-ups in the macros

In Q4, it was good to see that the management was able to sell a lot of the pending inventory from FY23, which makes the overall FY23 numbers look decent (not comparable to FY22 due to abnormal margins, but maybe this could be the new base). Additionally, any positive surprise in iron ore prices or that of other segments could be a positive surprise.

As pointed out by Ayush bhai, the scale up in mining segment (>2x in case of iron ore, slightly <2x in case of manganese ore) will add significantly to the bottom line since the PBT margins are >40%

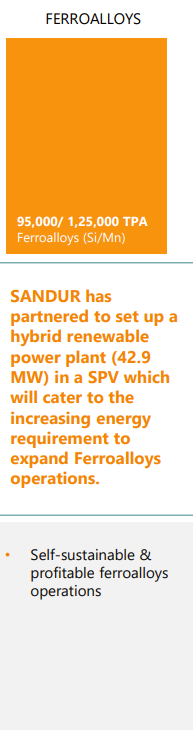

Another interesting thing from this quarter’s investor ppt was that Sandur has partnered to set up a hybrid renewable power plant for 42.9MW for its ferroalloys segment (attaching the relevant snippet below)

Had prepared a short note on Sandur a couple of months ago, attaching it here since it might be helpful ![]() (has data till Q3 FY23)

(has data till Q3 FY23)

Sandur Manganese Note_vF.pdf (132.1 KB)

Disc: 10% allocation at cost, holding, probably biased. Please do your own due diligence

| Subscribe To Our Free Newsletter |