There are some negatives in the latest result of Party Cruisers Limited.

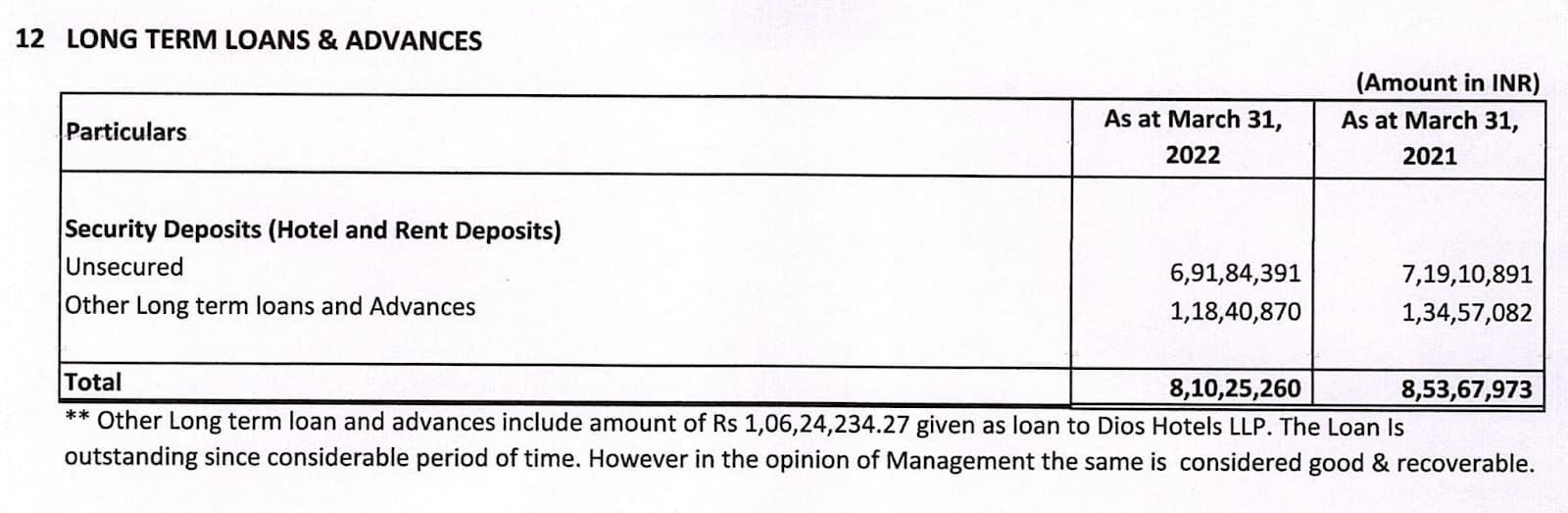

“Other Long term loan and advances for march 2022 include amount of Rs 1,06,24,234.27 given as loan to Dios Hotels LLP. During the year management has decided to write off the loan given to Dios Hotel LLP since as per management judgement and estimation the same is not recoverable. The same has been shown under extraordinary item in Profit and Loss Account for the current year.” Dios Hotels LLP is a related party.

This is from the last annual report where the management mentions that the loan to the related party is good and recoverable.

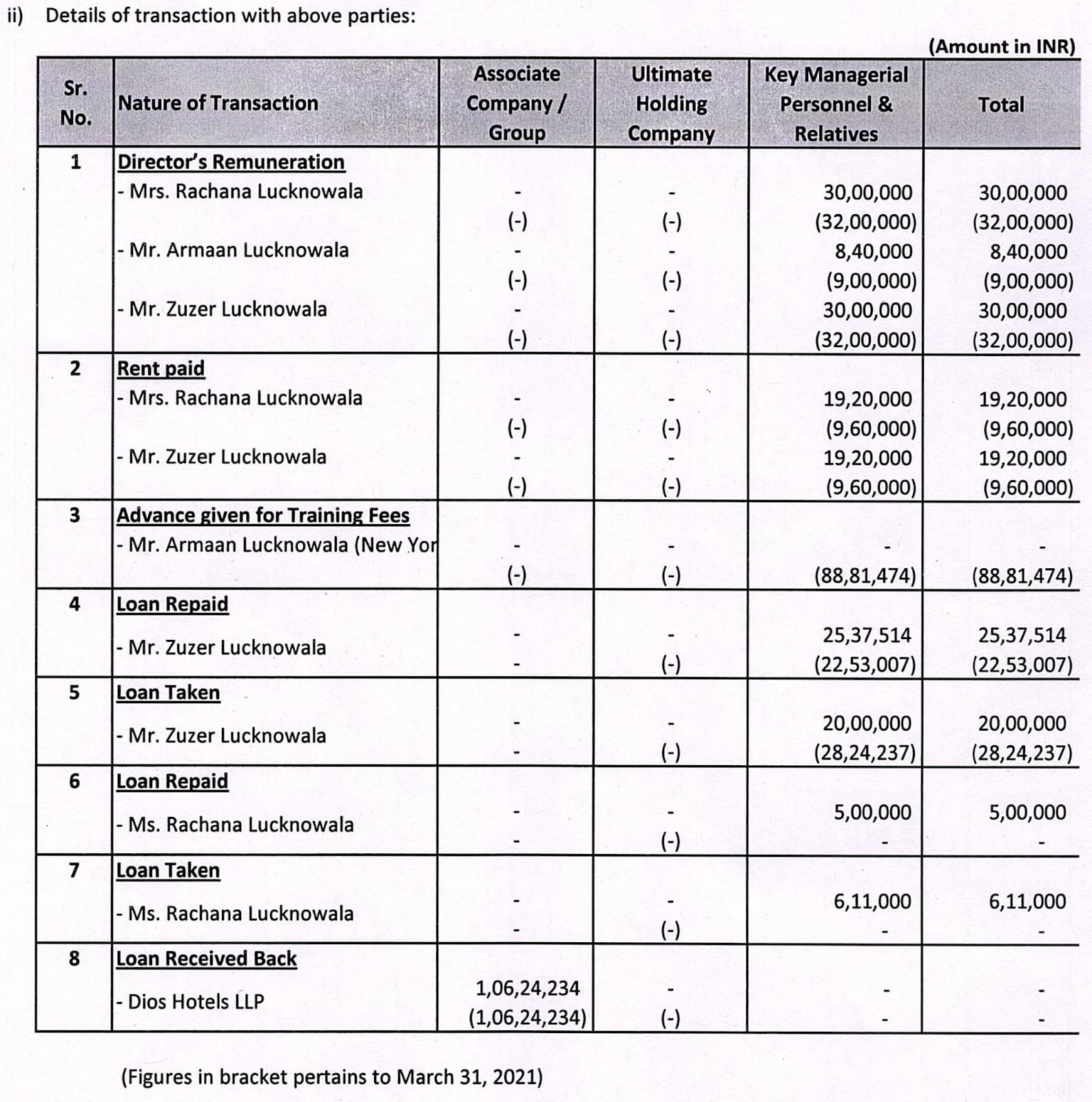

Related party transactions of last year are as follows:

Qualified Opinion

Independent auditors have not been able to obtain sufficient appropriate audit evidence to provide a basis for an audit opinion on the financial results.

“1. The Company’s Current Financial Assets as at 31st March 2023 includes Trade Receivables, aggregating to Rs. 497.45 Lakhs (31st March 2022 Rs. 105.06 Lakhs). Respectively out of which in respect of Trade receivable amounting to Rs. 48 Lakhs confirmations/statements have not been received. Therefore, we were unable to comment on the recoverability. Hence, we were unable to ascertain the financial impact on standalone financial statement.

2. The Company’s Current Financial Liabilities as at 31st March 2023 includes Trade Payables, aggregating to Rs. 181.15 Lakhs (31st March 2022 Rs. 175.88 Lakhs) respectively in respect of which confirmations/statements from the respective parties have not been received and which were outstanding for substantial period of time. Further, whilst, we have been able to perform alternate procedures with respect to certain balances, in the absence of confirmations/ statements from the respective parties, we are unable to comment upon the adjustments if any, that are required to the carrying value of aforesaid balances and consequential impact if any on the accompanying standalone financial results.

3. Trade receivable include amount of Rs. 15.96 Lakhs which were outstanding for substantial period of time. Management has assessed that; no adjustments are required for carrying value of aforesaid balances. Consequently, in the absence of sufficient appropriate audit evidence to support the Management’s contention of recoverability of these balances, we are unable to comment upon the adjustments if any, that are required to the carrying value of aforesaid balances and consequential impact if any on the accompanying standalone financial results.

4, The Company loan & advances include amount of Rs. 25.52 Lakhs. which is outstanding for substantial period of time. The same is shown under the contingent assets of the notes of account in previous years. We are of the opinion that provision of same is required in the books of account but as per Management assessments no adjustments are required for carrying value of aforesaid balances since they are in discussion with party for the settlement of amount & there for management is of the opinion that no provision is required, therefore the Company has not made any provision for possible loss on such loans and advances.”

The amount is less but it puts a question mark on the reported figures.

| Subscribe To Our Free Newsletter |