- Volume growth of only 8% is expected over FY24-25. GUJGA’s long-term volume growth prospects remain robust, with the addition of new industrial units, and expansion of existing units.

- Increased pricing competition expected from alternate fuels.

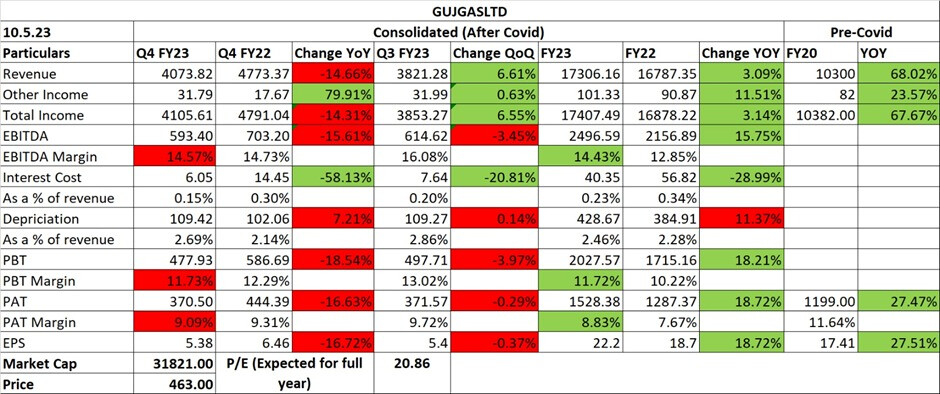

- Q4 saw a higher than expected gas cost due to which margins were affected.

- Low visibility on the spot LNG prices in the medium term.

- Volume recovery in industrial PNG segment. Growth in CNG, domestic PNG to support overall volume growth.

- Better pricing power and regulatory tailwinds over the long term.

- In the near term, price trend/global LNG costs trend will be key monitorable.

- Brokerages recommend buy/add with a target of Rs. 500-600.

- Brokerages recommend an EPS between Rs. 22-24.

| Subscribe To Our Free Newsletter |