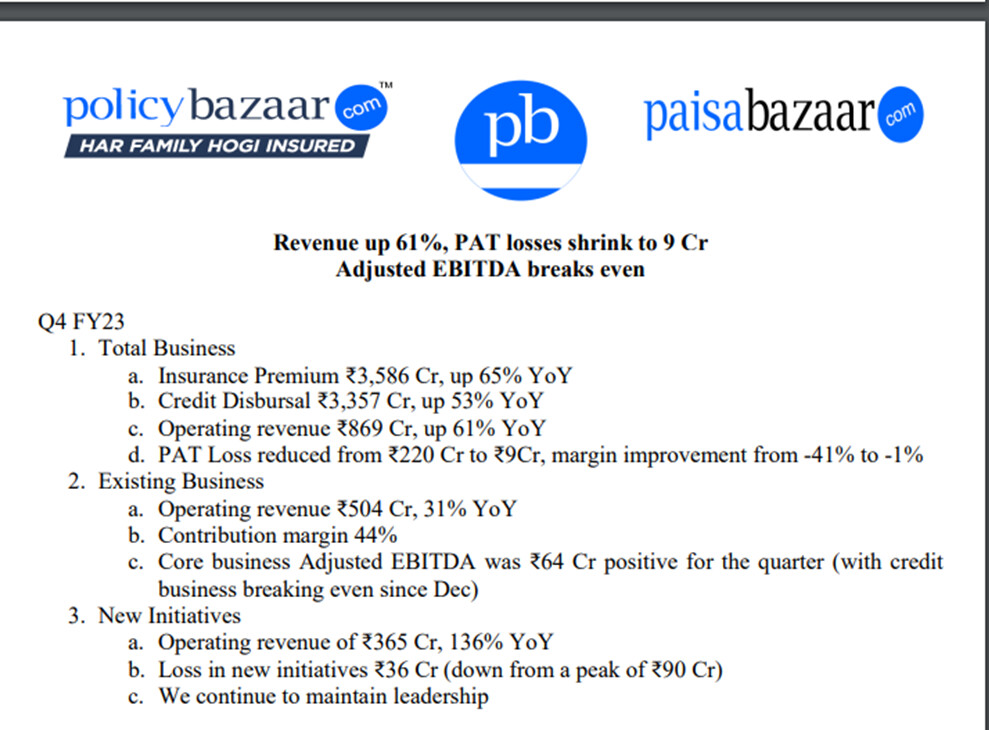

Good set of numbers by PB Fintech.

As trail revenue increases over time in both Pasia & Policybazaar (renewal rev) , the margin profile of the business should look dramatically different.

Management is guiding to be PAT positive in FY24.

My personal opinion is that being PAT positive is a little bit of an understatement. If you back out the 542 cr of ESOP charge in FY 23 (Which is not a real expense “this fiscal” but was a historical expense & because of GAAP accounting, it is being reflected over the vesting period), they are already Adj. PAT +ve 54cr.

Increased operating leverage next year as the business grows, a higher mix of trail rev, improved efficiencies in the “new initiatives” and no further ESOP charges should drive GAAP PAT significantly above 54cr.

Disc: Invested.

| Subscribe To Our Free Newsletter |