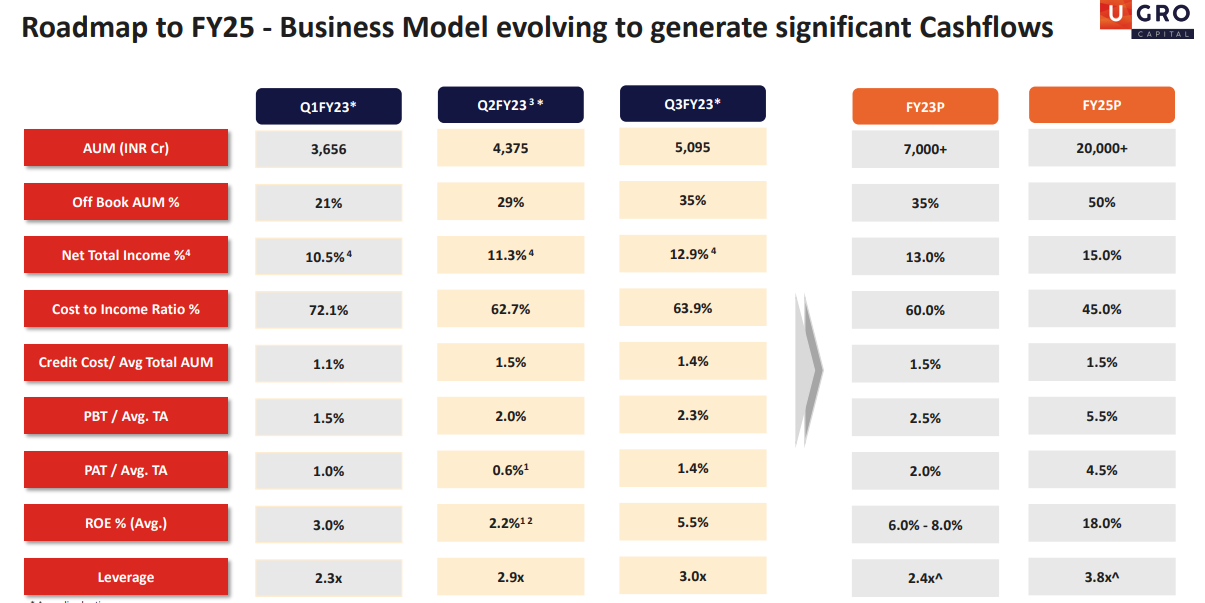

What this means – Some back of the envelope calculations

2025 PAT = 800 Crores. [ 4% of 20,000]

For context – FY23 PAT = 60 crore. Even after adding back the deferred tax reversals.

Of the 20k Cr AUM in FY25, 50% will be off-book. So on book AUM is going to be likely closer to 10k Cr and balance sheet assets basis historical trends is likely to be 11.5-12kCr (On book AUM/Assets has trended at 86-88% in the last two years). Equity needed will be much lower – this is the beauty of an at-scale co-lending model.

Having said that I think Management will slow down on the 20k Cr guidance for FY25 and focus more on steering the ship with good cost metrics and underwriting quality and my projection is they will end up with 17-18k Cr AUM by 2025. I think most of the 2025 metrics are achievable, the most challenging one IMO will be their cost to income ratio of 45%. I will be very pleasantly surprised if they do hit that C-I target in FY25.

As far as further equity dilution is concerned, the CFO was on record this year saying there is unlikely to be any dilution in FY24. I expect another round of equity infusion of 500-600Cr in FY25, probably in Q1. The dilution at that point is likely to be much less than now because the price will hopefully be much higher.

To my mind, if Ugro can show that their underwriting is robust as their book matures or the cycle starts turning, sky is the limit.

Disclaimer: Invested and biased. Projections may be wrong, please do your own DD. Financial businesses carry inherent leverage risks plus new financial companies only prove themselves after seeing a full underwriting cycle.

| Subscribe To Our Free Newsletter |