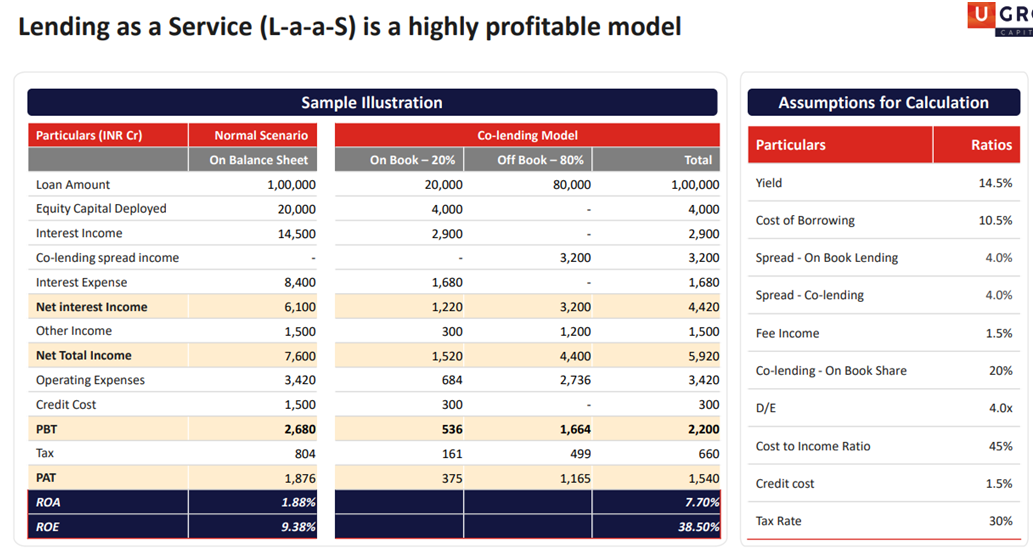

Ugro has established a co lending business model. The off balance sheet book (mainly with PSBs) earns spread without credit risk (except FLDG with NBFCs) and pushes the ROE magnificently.

There are two data points I want to discuss.

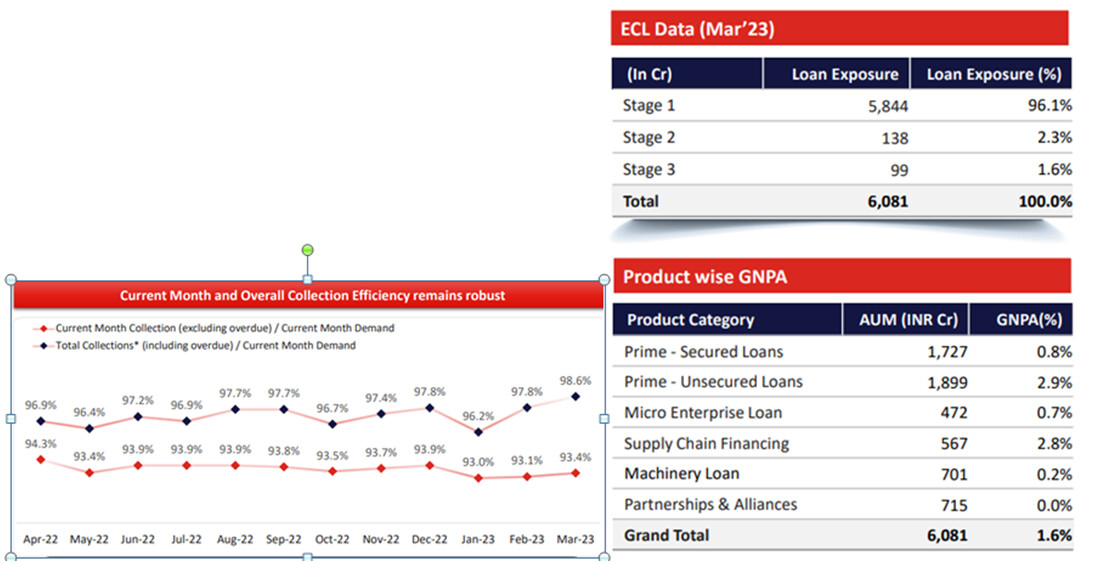

Gross NPA is 1.6%

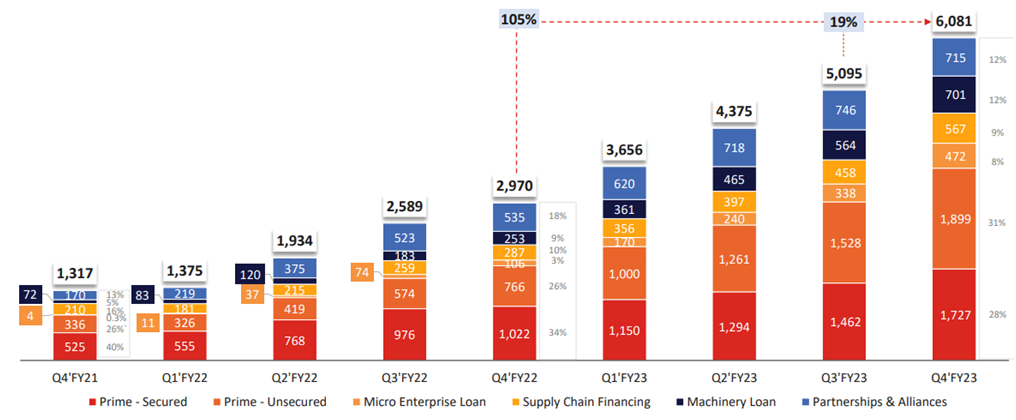

Q4 AUM: 6081cr

Q3 AUM: 5095cr

Disbursement made in Q4 cannot be NPA (requires at least 90 days due). So, for me GNPA is at least 1.9% (still good number).

For a very fast growing company AUM is increasing rapidly and GNPA may look optically low. The day AUM starts slowing down, real GNPA number will be reflected.

With a very little history, it’s very difficult to judge the underwriting quality.

Collection efficiency:

Their net collection efficiency (excluding overdue) is 93.4% for March.

It means 6.2% book fall into SMA bucket. This is disturbing for me.

But their gross collection efficiency (including overdue) is 98.6% for March. This number on a growing book is extremely good probably because of their in house collection team & litigation team.

The NPA is low because of their ability to recover.

6.6% account does not pay EMI. Out of which 2.7% pay within 60 days.

2.3% pays within 60-90 days.

Finally GNPA is 1.6%.

I am positively surprised by their recovery capability & equally worried whether they will be able to do the same in a downcycle.

| Subscribe To Our Free Newsletter |