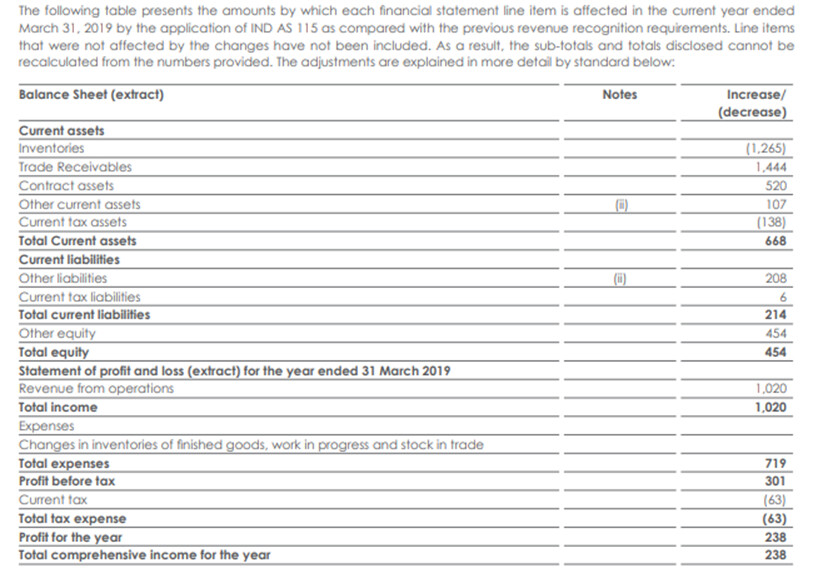

While the rest of the ag-chem sector faces headwinds, the PI juggernaut continues. For the first time, analysts quizzed the management on revenue recognition, as if finding the results too good to be true. It may be noted that w.e.f. 1st April 2018, PI adopted Ind AS 115 for the CSM segment, which allows the company to recognize revenue “over a period of time” as in case of contracts rather than “transfer of control” which is the usual norm for physical goods.

(Extract from Annual Report for FY2018-19)

Essentially, what this change does is it allows the company to book revenue as soon as goods are produced without waiting for shipment. This is perfectly legitimate though more aggressive (thanks to @zygo23554 for pointing this out and explaining neatly here. This change resulted in a Rs.23.8 crore increase in profit that year, but does not affect the YoY growth thereafter. So long as PI does not face any reversal of sales due to customer’s refusal to lift goods that have already been produced, this will have to be considered okay.

| Subscribe To Our Free Newsletter |