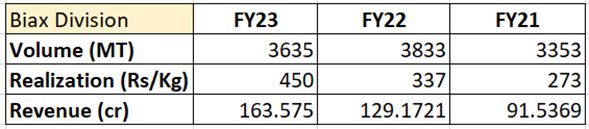

The realization of Biax division is continuously increasing.

As the current Biax division capacity (4000MT) is fully utilized at revenue growth is coming from realization benefit only.

Management is confident of the same thing repeating in FY24 also.

This can be driven by high technical grade product mix (low thickness)/ Global supply demand mismatch/ China + 1/ Toll manufacturing. Probably all of these combinedly played a role & realization moved up.

Between FY16 (realization was Rs 220/kg) to FY20 (Realization was Rs 242/kg) realization is pretty much flat.

Now they are investing 500+ cr for 2 more lines. Incremental capacity will be 8k MT.

Assuming they will be reaching near full utilization by FY27 & will be doing thickness as low as 1.5-2 micron, realization may move upto Rs 650/Kg.

That should do an asset turn of 1x. The question how sustainable is the realization growth? Would have loved to hear more from management but they do earnings call annually.

| Subscribe To Our Free Newsletter |