While they don’t seem to have done a concall yet, it seems like they have generally enjoyed a strong pricing environment for some of their products. It could be because of China’s Covid situation etc. In which case we should probably not extrapolate the FY23 margins – and also the topline will face headwinds if the prices come down.

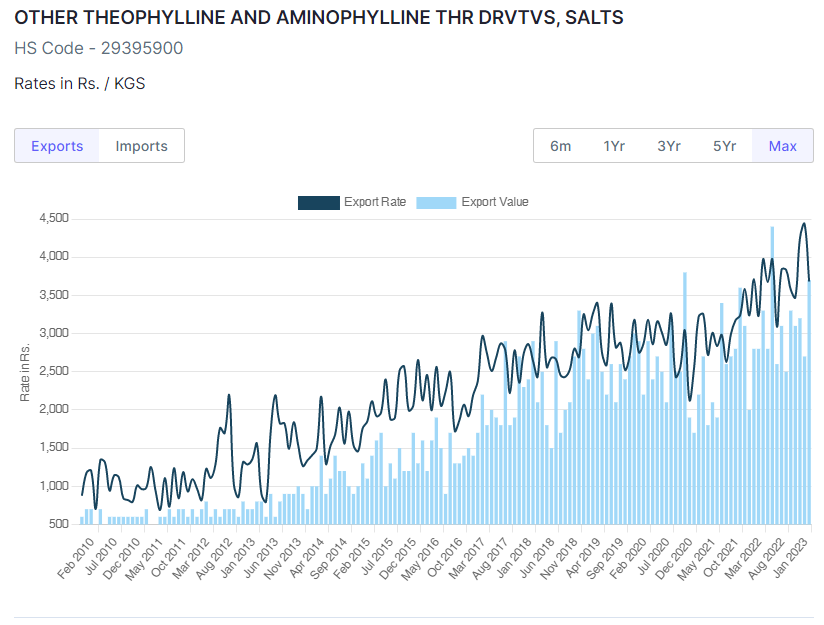

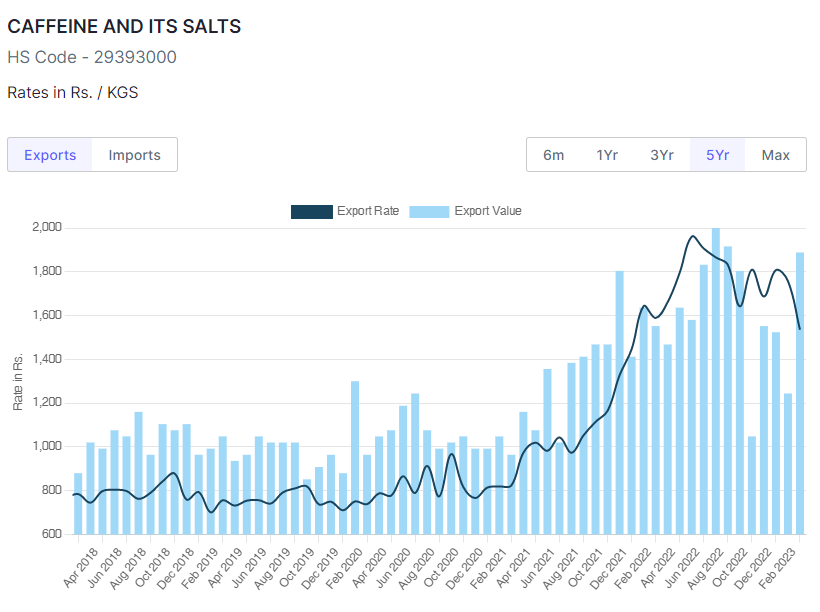

Not sure how reliable an indicator this is, but here is the export data which is there in Screener.

This is just Xanthine derivatives, there are other movings parts to the business of course, and capacity expansion etc.

| Subscribe To Our Free Newsletter |