Thanks for sharing the Q4 concall highlights.

Attended the concall of Tinna rubber for Q4 of Fy 22-23 and observed that management was uneasy on replying the questions regarding quantitative deails and bifurcation of revenue from road sector and Non road sector.

Reply from management was unsatisfactory regarding growth in revenue in comparison to volume growth. Revenue of the company increased to 295 crs in fy 23 against 229 crs of fy 22, an increase of 29%. But found that, volume of waste tyre crushed is increased to 74,000 tons (disclosed in concall) in fy 23 against 48,286 tons of fy 22, an increase of 53%.

Disclosure in financial statements for Q4 of fy 23 was also poor. Any other income or expenses which materially affect the P/L A/C, whether it is provision for bad debts, balances written off, gain/loss on sale of fixed asset, gain/loss on foreign exchange fluctuation, subsidy or grant from govt. should have separately disclosed through notes on accounts with figures.

Few of my earlier queries through email was satisfactorily answered by the management, but my query through email after Q3 concall regarding volume (with attachment of figures) was not replied by the management. Reposting it here: –

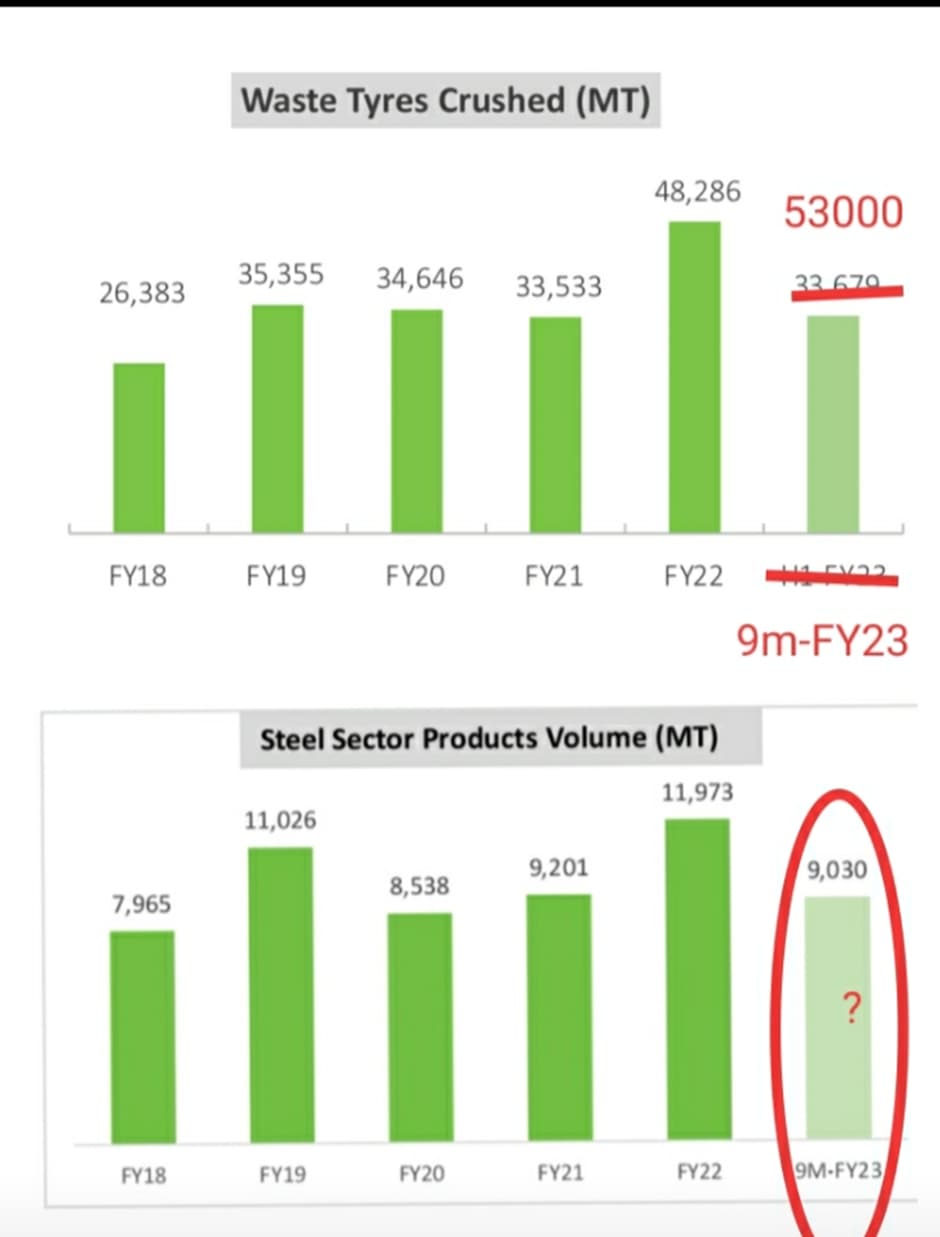

In FY 22 we crushed 48,286 MT of waste tyre and volume of Steel sector products was 11,973 MT, as disclosed in earlier investors presentation.

In Q3 concall of current financial year management told that till Dec. 22 we have crushed nearly 53000 tons of waste tyre.

In latest investor presentation the 9-monthly volume of steel sector products is just 9030 MT.

I want to know that what is the reason of such percentage – wise decline in steel sector products against the volume of waste tyre crushed?

I also want to know that in investors presentation the volume of products shown, whether it is for road sector or non-road sector or steel products sector, is quantity sold or quantity produced during that period?

disclosure :– invested from lower levels.

| Subscribe To Our Free Newsletter |