There will be growth in the EPS in the upcoming quarters because of following reasons-

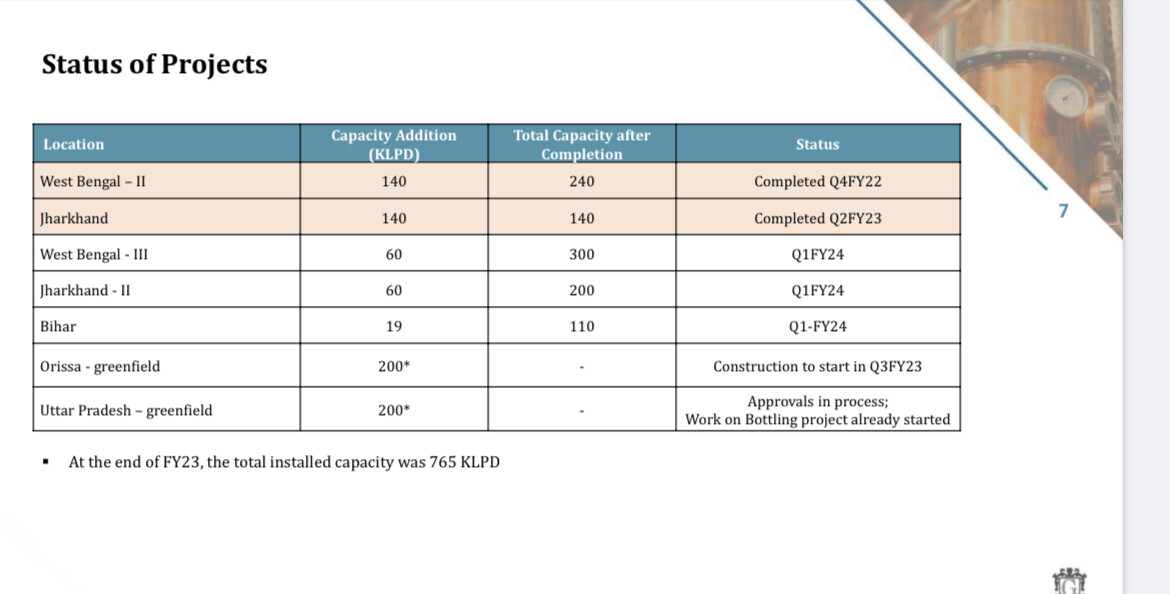

1-Capacity Expansion is Recently Completed for West Bengal Unit2 and is In-Progress for WB Unit3, Jharkhand Unit2, Bihar Plant, Greenfield Capex for UP is already Started.

We will see the major Increase in Topline +Bottomline from Q2FY2024 onwards

2-Secured another price hike of Rs 40 per case for Value Plus and Rs 20 per case for Value segment in Rajasthan, effective 1st Apr’23. This along with ongoing momentum in Premium+ Brands will continue to support consumer segment realisations

3-Full year of operations for 140 KLPD Jharkhand facility and incremental capacity of 60 KLPD each at West Bengal III and Jharkhand II, is likely to benefit Manufacturing Business in FY24

Disclaimer- Invested, can be biased, Source- Investor Presentation- Q4FY22

Always open for your opinion ![]()

| Subscribe To Our Free Newsletter |