I disagree. Everyone has capacity expansion plans, the question is when these triggers play out and how early one wants to be. In the absence of volume triggers, this sector largely moves with the sentiment of the underlying commodity.

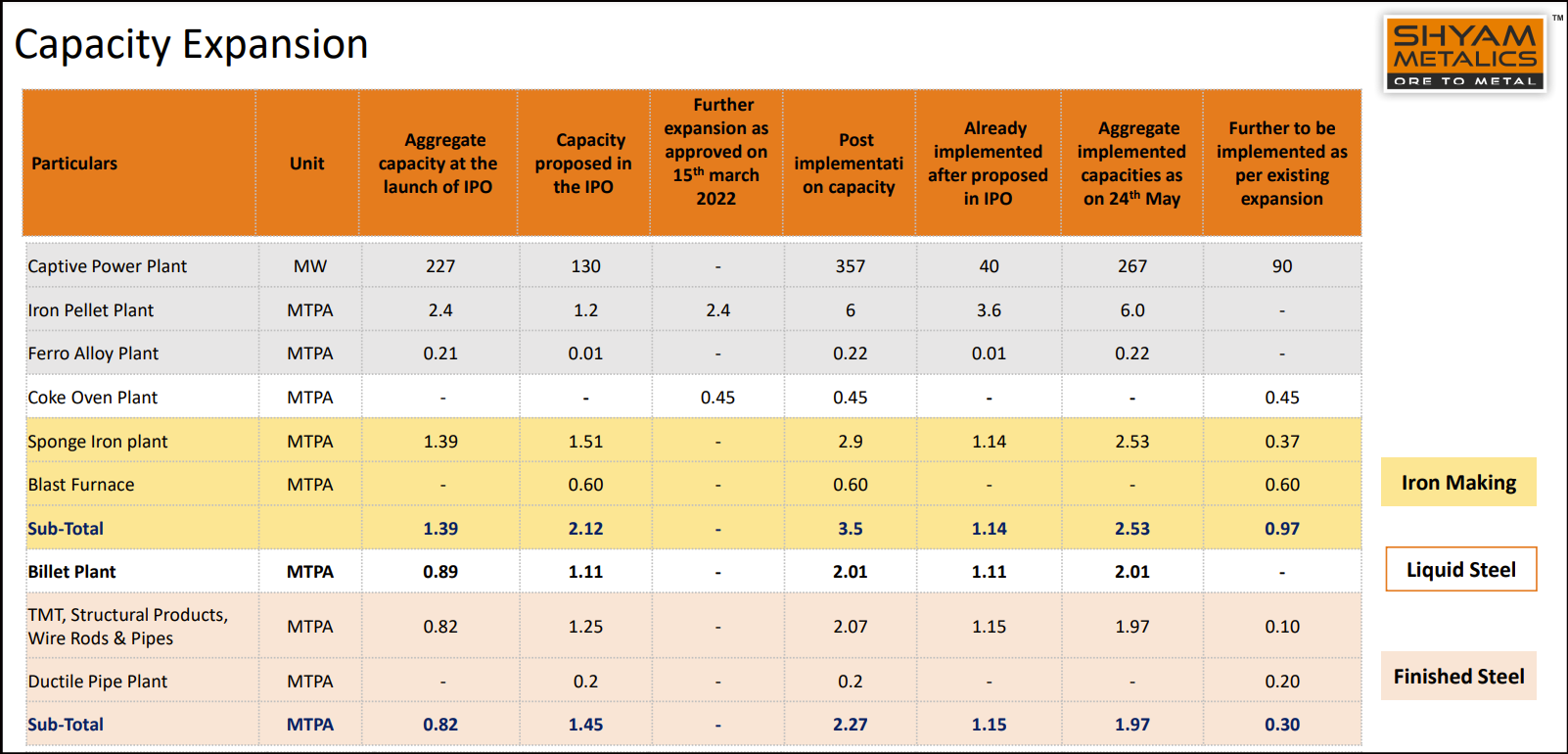

For Shyam, a lot of this capex has been capitalised, so one has volume growth even though the underlying index is in the doldrums.

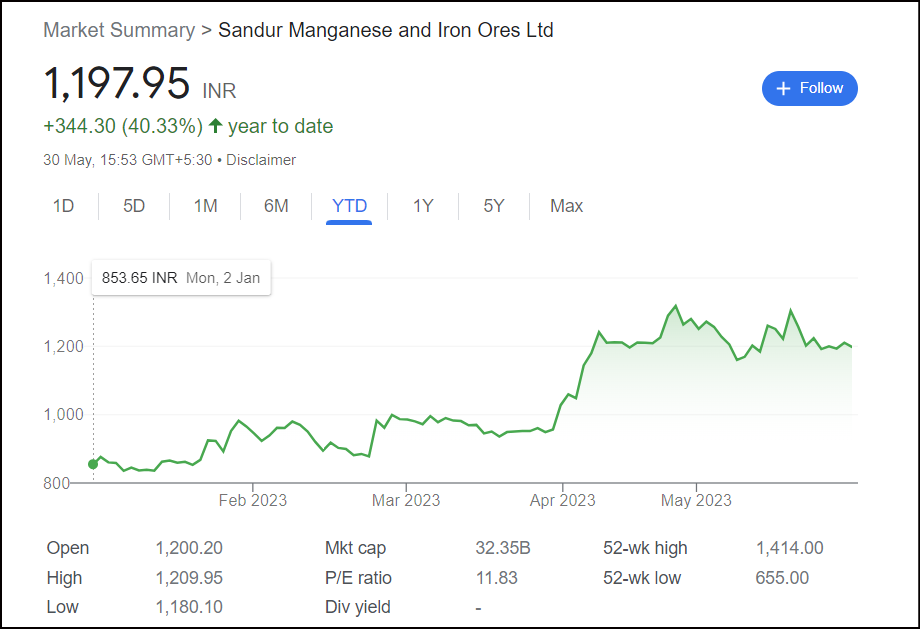

Sandur Manganese too had an incredible first half of the year with the stock rallying on expectations of their mining EC coming through.

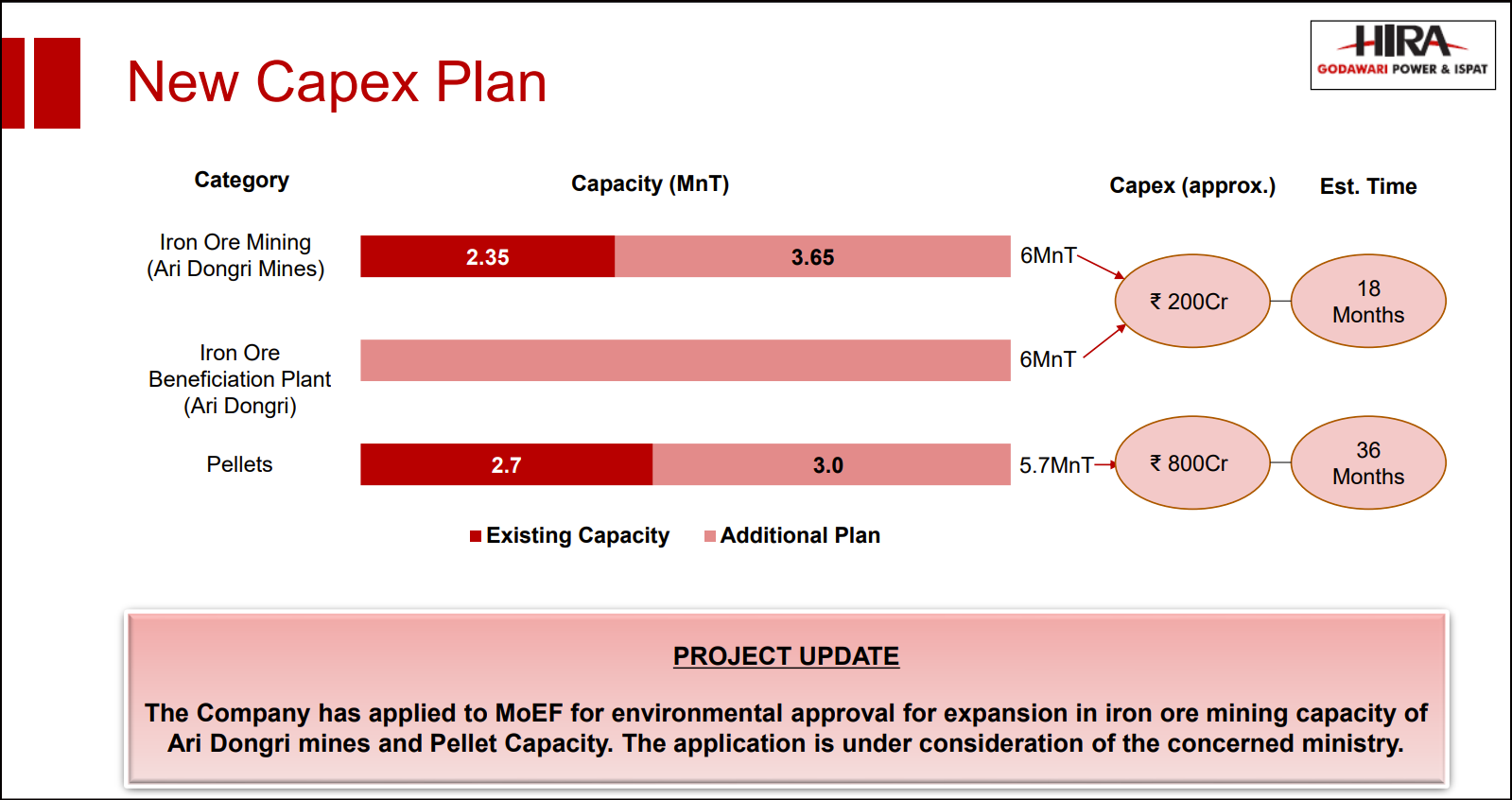

In GPIL’s case, despite all the stories written on the company thread, it looks like FY24 is a year of consolidation in terms of volumes, and capex triggers will play out in FY25 and beyond.

There are many nuances in the story. Shyam didn’t have captive mines until recently, and then they had to pay a premium. I’m playing this in the simplest possible way: to have volume growth on my side until realisations recover.

I’ll churn out of Shyam eventually depending on how the cycle moves.

| Subscribe To Our Free Newsletter |