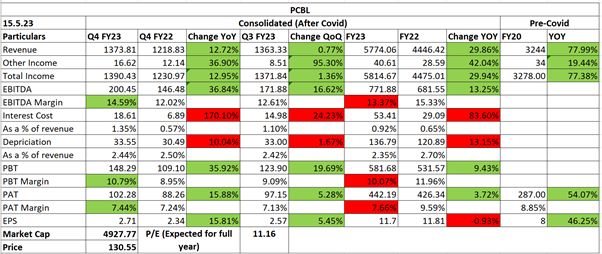

PCBL Q4 FY23 Result Update:

- Guidance: Management guided for ~500 KT+ carbon black sales volume in FY24E (up 12% YoY, 445 KT in FY23) amid a new greenfield plant & expects to further grow speciality volumes to ~50 KT in FY24E vs. ~40 KT clocked in FY23. Amid healthy demand prospects, we expect sales, PAT to grow at 7.8%, 13.0%, CAGR, respectively, in FY23-25E, building in 12.2% volume CAGR. Long term growth prospects are robust amid favourable demand – supply situation in overseas markets. Exports are expected to do good especially from the US & Europe region. The company expects to maintain its margins achieved in FY23 and improve margins by around Rs. 1,000 per tonne due to product mix changes, operating leverage, and improving manufacturing efficiency.

- Expansions/Capex: The Greenfield Project in Tamil Nadu has been commissioned, and the Brownfield expansion of specialty black in Mundra is nearly ready and undergoing commissioning. The company plans to utilize 40%-50% of the Chennai plant’s capacity for this financial year. The Specialty Carbon Black – Mundra line is expected to become operational, and the company anticipates the growth momentum to continue. Additionally, there will be a capacity increase of 10,000 tonnes for the full year, representing a 25% growth. The company plans to increase capex by Rs1.5 billion in brownfield expansion and Rs1 billion in Chennai, totalling approximately Rs2.5 bn in capex for FY24. Capacity utilization at new facilities is expected to be around 40-50%.

Brokerages expect Revenues of FY24/FY25 at 6000 cr/6700 cr. Expected EPS for the respective years is Rs. 12/Rs. 15.

| Subscribe To Our Free Newsletter |