HAL Q4 FY23 Result Update:

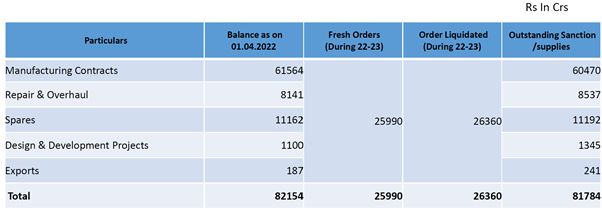

- Order book position is maintained at Rs. 81784 Crores with receipt of fresh Manufacturing Contracts, ROH and Spares orders.

- Guidance: Revenue guidance for FY24E was maintained at 8-9%. For FY25, revenue growth is expected to be in double digits mainly led by execution of LCA Tejas MK1A. From FY26 onwards, revenue growth is likely to stabilise at 12-13%. Repair and Overhaul revenue is expected to see an uptrend of 5-6% in revenue. EBITDA margin (including other income) is expected at 26-27% in the coming periods. Moreover, execution of other key orders and sustained growth in MRO will drive revenue growth in double digits from FY25E. The manufacturing segment will remain subdued in FY24 and expected to pick up in FY25. The company is expecting order value of ₹48,000 crore to get concluded in FY24. They are envisaging orders from export market including Philippines, Indonesia, Argentina, Egypt, Maldives, Sri Lanka, Thailand, Nigeria and Middle East in the coming periods.

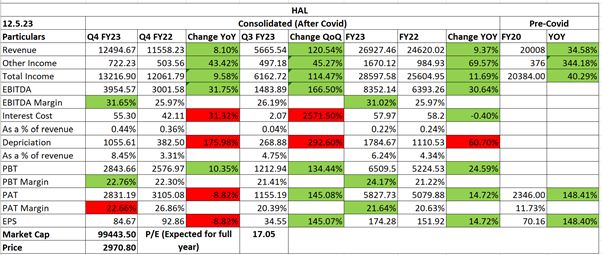

Brokerages are eyeing and increase in revenue in FY24E but PAT levels are expected to see a de-growth.

| Subscribe To Our Free Newsletter |