CMP : 110

FY23 might close > 70 crores

EBITDA margin : ~17%

PAT : 9 crores approx (FY23 yet to be announced)

PAT margin 12%

PE : 14

Amount in crores FY20 FY21 FY22 FY23 (approximate annualised)

Revenues 0.96 9.41 18.61 70

PAT -2.24. -0.67 1.51 9

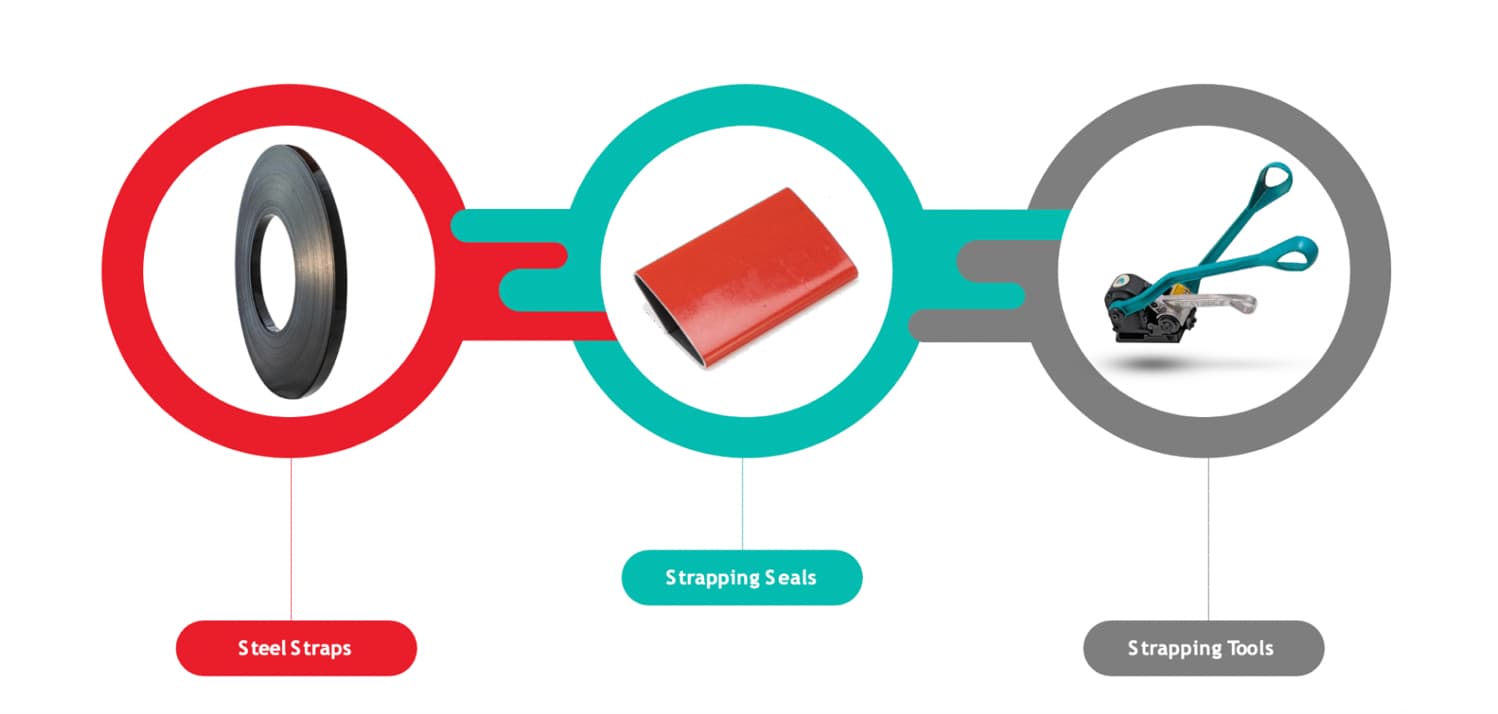

Incorporated in 2017, company is manufacturer of high tensile steel straps, strapping seals and strapping tools. It has 100+ customers, 50+ EEs. It boasts clients such as Jindal, JSW, POSCO, SAIL, BAOSTEEL, AJ Steel, THL pipe, Hyundai steel. St. Gobain, Gold plus.

Its capacity for steel straps is 18000 MTPA and strapping Seals is 80 MNPA.

About the promoter :

Balamanikandan has a degree in engineering in electronics and communication from Anna university and has obtained master of scientific degree in info security from university of London, UK.

He performed extensive research in steel strapping for nearly 2017-2018 and understood the industry has been concentrated by a few names.

Competition :

Player Per month capacity (MT) Market share

Signode 6000 49%

Grip Strapping. 4000 27.50%

Tata Steel BSL 1000 5%

Walzen Strips. 1500 11%

Krishca 1500 7.50%

Marketsize in India is ~10000 TPM.

Competitive Advantage :

Steel strap is critical item needs stringent heat treatment. Heat treatment process is intense and there is no machine supplier in india, all machines are imported from Korea.

The straps needs to be High precision 100% perfect, since any faulty can cause road accidents. Even a Small crack can make entire FG useless.

Krischa is the lowest cost producer. Competition using Led based oven. They are doing electrical based oven, pollution free process.

Also These are small % of end product, making the customer not so sensitive to price change. It is a small market and hence no large player would want to have it inhouse.

Purpose of issue :

Company raise ~18 crores to fund new capex (12 crores) and to repay its debt (4 crores). The company intends to double capacity to 3000 MT New capacity will be ready by Oct/Nov, 2023.

Per tonne sells for approx 1lac. So can achieve 180 crores with current capacities.

With 3000 MT can achieve 350 crores turnover.

Growth drivers :

India is one of the fastest growing steel industry. Current production is around 120 Million MTPA, and by 2030, it is expected to reach 300 Million TPA.

Company plans to enter packing contracts business, it will help in boosting turnover at similar margins, doesn’t need any capex, it is a service business.

Their facilities are proximity to Chennai port, opening up export opportunities in Middle East. There are no players there, also can cater to US market from there. US has ADD on steel straps from India.

Anti Thesis :

Their RM is Steel coils, any fluctuations can in the interim dent margins.

Company doesn’t have a long track record, was established in 2017.

Disc : invested

| Subscribe To Our Free Newsletter |