Thankyou for your kind words.

I think they mentioned the size and location of this land in previous con call. I did not do the hard work. If we can spend some time on google we can get a broad range. Like if they have 25acre we can get the per acre cost.

Management has tried their best to not disclose any details on this I am clueless.

- Plz go through recent con call very interesting. I have a lot more to share but many people don’t take interest hence i don’t share much. If you see I have been very clear that volumes will pick up in H2FY24 and peak will be H2FY25( I revise this from H1FY26).

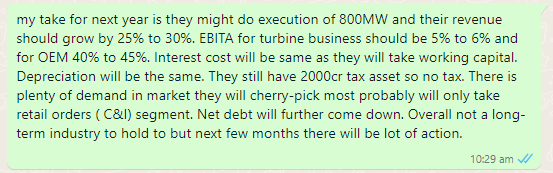

Next year they are confident of executing 50% to 60% of order book( Close to 800MW) and also see the per windmill realization is up form 4.9cr to 5.3cr. So next year I am expecting 20% to 30% sales growth on a standalone basis. 10% to 15% on consolidated basis.

Next year OMS is going to puck up 2021 installation comes in 2024 OMS we can quantify this but I have not done yet.

- They will not take any international order. Just see the recent order they have one is majorly from retail and I have made the tender post still there are huge amount of order in market.

They won the torrent power order which has the higest price. They are getting choosey in domestic market international is out of question now.

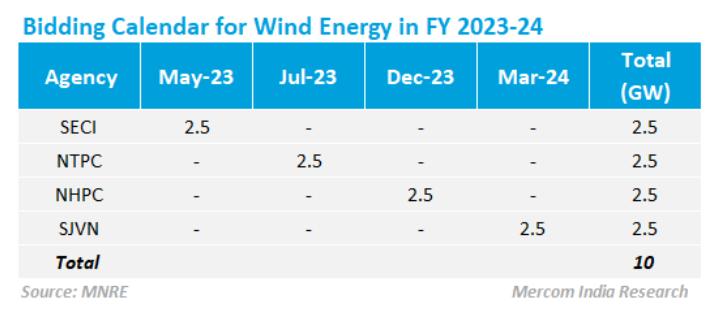

This year bidding plan. There is huge amount of order and the ISTS waiver will end in june 2025 so all C&I, retail are in a rush to complete before june 2025 hence I say peak is H2FY25. I wont be surprised if they don’t take any more order form central auction

- They did explain this in concall I did not understand. Waiting for transcript. What I understood is the entire project cost reduces but not the per turbine cost.( margins are the same but headache reduces) So just think for setting up 300MW capacity with 2MW wind mill I need 150 of them.(more logistic, more land, more operations) but with 3MW I need only 100 wind mill.

My thesis.

They are somewhat getting the same 2016 valuation ( little bit higher) where as 2016 their debt was 11000cr and today it is 2000cr and the entire situation today is more positive than 2016. So they should be valued more.

Technically they look very strong. I am expecting 15 to 20rs by march 2024.( They just need to wind 2 to 3 more order and price will trigger)

I am expecting 300cr to 500cr PAT next year ( I think it is 160 for current year) this can go to 1000 easily if they execute 1.8GW I have done the math above so with my avg price of 8rs I am very well placed and my thesis was 100% in 1year to 1.5year which looks very possible now.

Dic- Invested 7.5% at 8.2

| Subscribe To Our Free Newsletter |