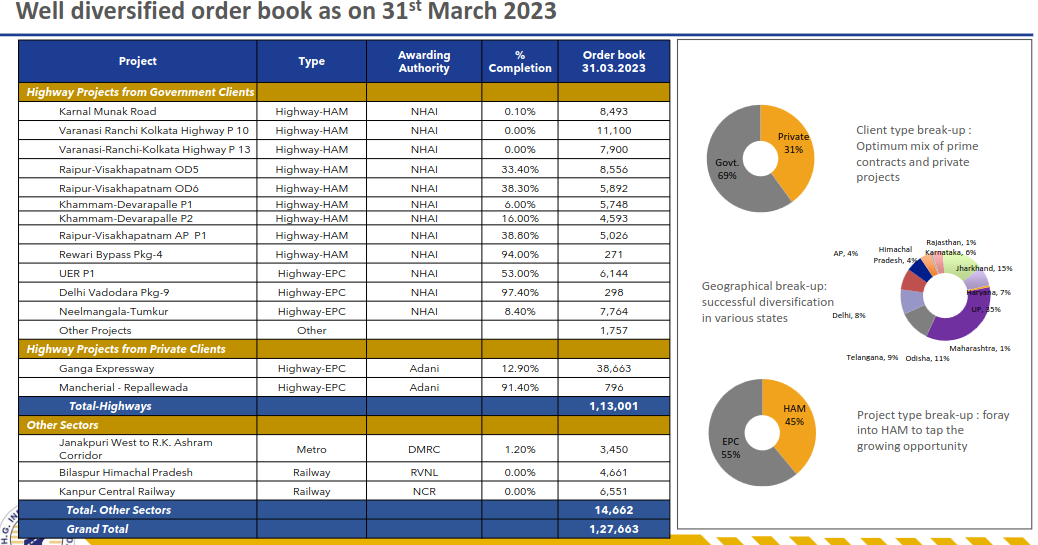

Order book from Investor Presentation at https://www.hginfra.com/pdf/investor_presentation_q4_n_fy23.pdf

Concall notes summary from Screener.in

Concall Notes – May 2023

Financial Performance:

Standalone overall revenue increased by 22.2% YoY in FY23

EBITDA grew by 21.5% YoY in FY23

Profit before tax for Q2 FY23 grew by 64.8% YoY

Five-year CAGR for revenue, EBITDA, and PAT were 26%, 28%, and 38% respectively

ROCE and ROE increased to 30% and 24% respectively

Order Book:

Order inflow of INR8,650 crores during the year

Anticipates securing orders worth INR8,000 to INR9,000 crores in FY24

Aims to have 20% to 25% of the order book comprising non-road projects within

the next two to three years

Bid for INR8,000-9,000 crores in railways and metro projects and INR1,600 crores

in water projects for FY23

Business development unit created to explore opportunities in railways

and water projects for FY24

HAM Projects:

Monetized four HAM projects for INR1,394 crores with an equity value of INR531 crores

Total requirement of all HAM projects in equity was INR16,120 crores

INR735 crores were invested till March, with a balance requirement of INR440 crores

for FY24, INR359 crores for FY25, and INR76-odd crores for FY26

The company expects inflows from the monetization of projects to be received one

by one with different amounts

The company has secured INR500 crores worth of execution from recently

won HAM projects

New Projects:

Secured three HAM projects and three non-road projects

Central government intends to accelerate the construction of roads in FY24

with the awarding of new projects of 12,000 to 12,500 odd kilometers this year

The company is looking to grow their order book in the financial year, majorly

from roads and highways segment, but they would like to further extend their

presence in other sectors too, including water, railways, and other opportunities

Bid for five water projects in FY23 but couldn’t invest in any of them due to

L4 to L5 range estimation

The company is exploring Ropeways and tunnel projects in addition to

highways, railways, and water projects

NHAI has a pipeline of 2,300km bids to be awarded from June onwards,

and NHO projects offer further opportunities

Margins:

EBITDA and gross margins have shown improvement due to a normal trend,

with OPM increasing

The EBITDA margin guidance for the next few years is tentatively around 16%

The company expects operating margins to be around 15-15.25% for

under-execution projects

Capex:

Capex for the year was INR340 crores, with equipment upgrades

being a strategic focus

The net capex addition for 2024 and 2025 is expected to be around

INR100 crores

Debt and Cash:

The company expects debt level to come down to around INR350 crores

by the end of next financial year

Mobilization advance is INR328 crores, retention and miscellaneous

deposits withheld total INR879 crores in debtors

The company has INR67 crores withheld amount, which is considered

in the debtor balance

Guidance:

The company expects inflow of INR530 crores from

he sale of four projects

this year

The company expects execution growth of close to 23% and does not see

any risk to execution from elections

The company expects to sustain 20% growth in FY25

Q1 earnings are not possible due to delayed NOCs, but arrangements will be

made for Q2 and Q3/Q4

Heavy monsoons affected projects in March and April, but Q2 is expected to have

a 23% YoY increase in earnings

The revenue guidance for FY24 is expected to be around INR5,500 to

INR5,600 crores, which is 23-24% of the total

The company had a successful year and is committed to delivering

better in the future.

| Subscribe To Our Free Newsletter |