Please note that I am not accounting expert and hence my understanding may be wrong. I have gone through the Annual report for FY22 to understand goodwill accounting and impairment policy of the company. Page 226 (pdf file)/Page 206 (print file) annual report provide notes to account related to Goodwill and its impairment.

As we observe, there has been major charge of good will impairment of Rs 73 Cr in March 2023 quarter in consolidated accounts (vis Rs 5.59 Cr in standalone account). In the consolidated companies, Music broadcast is significant subsidiary of the companies. While the notes to result does not provide what all heads the company has provided for goodwill impairment, the price decline in Music Broadcast in March quarter could be one reason for major goodwill impairment.

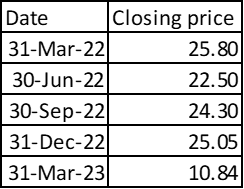

Fine enclosed quarter wise price of Music Broadcast price

During March 2023 quarter, price decline almost 60% from Rs 25 to Rs 10.84 per share and that could have trigger goodwill impairment in my view.

Recently, I have recently added Jagran Prakashan in my portfolio due to following factors:

- High Dividend Yield and Cashflow returning management.

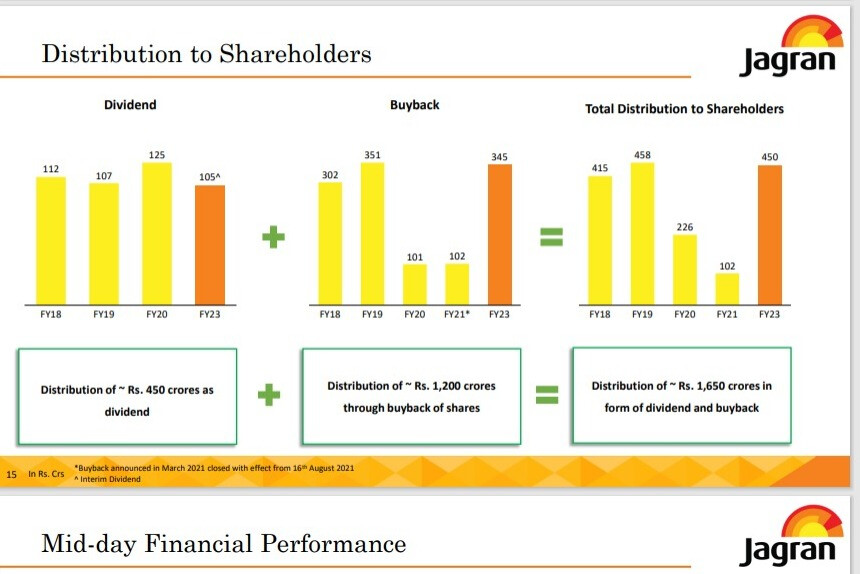

At current price of Rs 75 with Dividend of Rs 4 per share declared in FY23 (and also likely to be sustainable), one can expect around 5%+ Dividend yield from this investment. Further, as compared with current market capitalization of Rs 1600 Cr, the company has already distribution Rs 1650 Cr (by way of Dividend+ Cash buyback) as per March 2023 presentation.

Future cashflow to investor would depend more on future profit and business prospect, but at least intent of management to share cashflow with investor is strongly established from past action in my understanding.

-

Improving Business Prospect:

Media Industry was worst affected industry from COVID. While recovery in economy also resulted with delay, recovery in advertisement and subscription revenue to print media, still it just managed to get to level near FY2020, which means no real growth in past 3 years. Further, profitability was also adversely affected by higher newsprint price. As per Screener compiled import price data of Newsprint, Newsprint import price peaked to Rs 73.54 per kg in October 2022 and now trades at around Rs 65 per kg. The decline in newsprint price along with stable GDP growth and 2024 being Central election shall augur well for sales and profitability of the company in my view. My record of being right with forecast is pathetic at best. Hence, reader shall do his/her own due diligence, as my forecast may revert to mean (that is being incorrect) and very low probability of being correct. -

Concern for Minority shareholder:

The management of Jagran Prakashan did IPO of Music Broadcast in March 2017 as price of Rs 333 (10 face value+ 323 premium per share). Subsequently share was split in 2 paid up (5 shares) in Feb 2019 and bonus issue of 1:4 share in March 2020. So, 1 share held in the company would have been now 6.25 shares, reducing IPO cost per share to ~Rs 53. However, the market price of Music Broadcast was at around 20-25 per share. In order support Minority shareholder, Music Broadcast issue a Bonus preference share (with approval of NCLT), where by only non-promoter investor got a preference share. This is very positive steps in my view. In Past, we have seen Reliance Power did same but the price continued to decline even after that action. However, I consider this as a very positive gesture from promoter.

Negative:

- The management did acquisition of Music Broadcast at around Rs 500 Cr for ~70% equity stake in the company in 2014.

Jagran Group to acquire Radio City | Mint

At current market cap of Rs 382 Cr of Music Broadcast, value of 70% stake ~ Rs 270 Cr, decline of 45% over almost decade of holding. One can also attribute current decline market capitalization to industry fortune also as Radio business continue to suffer post COVID and is the most adversely affected segment of Media sector (if one compare revenue in FY20 with FY23). However, as on date, the acquisition did not yield required return for investors in my view.

https://www.screener.in/company/RADIOCITY/

Disclaimer: My view may be positively biased due to my recent investment (around 1.5% of my equity portfolio). Purchased share in last 15 days. I am not a SEBI registered advisor. I am not suggesting any investment action in the company. I may exit from the company WITHOUT INFORMING forum in case I find any other investment opportunity or change by asset allocation. Reader shall consult his/her investment advisor and do due diligence before making any investment decision.Future cashflow to investor would depend more on future profit and business prospect, but at least intent of management to share cashflow with investor is stongly established from past action in my understanding.

| Subscribe To Our Free Newsletter |