The company is mainly into offshore software services in areas USA, Canada, Australia,

Europe and the Middle East. Out-sourced Product development (OPD) market space

continues to be the key focus area for the Company. I think the company is providing

services to clients in countries such as USA( which brings 80% of the revenue )

using ( low-cost ?)resources from India. Their offshore software development services

include right from developing, deploying, and supporting while their clients focus on their

main business.

Achievements:

2500+ successful projects, 1100+ satisfied customers, 35+ finest of technologies

deployed

Growth:-

From Mar-2014 to Mar-18, the company had flat sales of 30 Crores. From then

onwards, sales have increased from 30 in Mar-18 to 77 in Mar-23 on a consolidated basis

and from 14 to 55 on a standalone basis. Operating profit has grown over the same

period and OPM is 22-24% over the last 3 FYs. Whether margins are sustainable or not

need to be seen.

Risks: As mentioned in the main post by @Manojeet_Das , it is regarding the remuneration. If we look at the RTP transactions reported the remuneration is around 1 Cr and the lease is 0.37 Cr for the period upto Sep-22 and the respective figures for the period Oct-Mar 23 are 1.8 Cr and

0.38 Cr.

If the company uses its building and land which it acquired, then will this lead to a reduction in lease expenses need to be seen. Did they mention anything in the AGM @rupeshtatiya sir?

Regarding remuneration: This is the information that I have found in ARs. In FY22, the

ratio of remuneration received by G Suresh is 25.82 to the median remuneration

received by the employees. In FY21 the ratio is 32.26. I have compared this with the

Danlaw Tech India Ltd which at present has 251 MCap and the ratio is 28.8 in FY22. So I think the remuneration is not a red flag, what do you reckon @Manojeet_Das sir.

In FY21, the remuneration is reported to be around 181 lakhs( increase of 39%

compared to FY20 ) , and for FY22 the remuneration is similar. I think FY23

remuneration has increased which they have proposed in FY22 AR.

Number of employees: 287 employees v 240 YoY AR 22. Their website now shows that

it employs over 525+ professionals. They are still hiring through LinkedIn and seem to

be offering permanent WFH as an option.

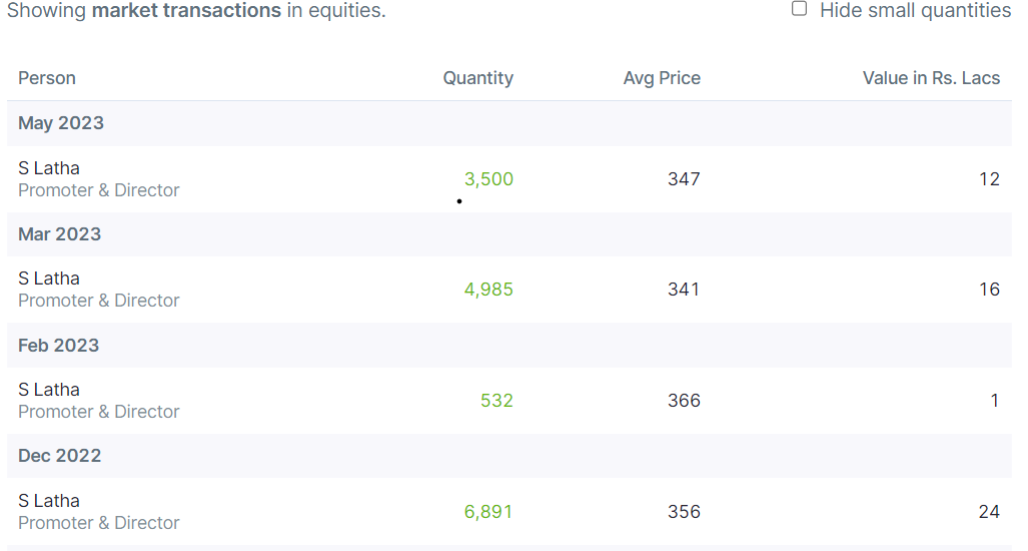

Promoter buying: The promoter, S Latha has been buying shares and increasing their

stake.

Overall promoter holding 53.75 Mar-23 vs 53.64 Dec-22

Valuations:

The company is now available at P/E of 15.2 against the 5 year median P/E of 12.8 and

3 year median P/E of 14.2. If the company maintains the same growth over next 2-3

years, then we can expect good upside in the stock price. Other seniors please share

your views regarding the valuation and the current opportunity.

IMO, currently it looks good, as lot of Micro-cap and small Caps are reaching all-time

highs.

Disclosure: No positions yet, but looking to add at this price. Not a buy/sell recommendation.

| Subscribe To Our Free Newsletter |