Was having a look at the financial statements of the company and there are a few divisions except the exploration part of their business that I believe can be a significant booster for the Company.

1. Dividends from Indian Oil Corp. (IOC):

Oil India holds a 5.16% stake in IOC that as of today is valued at approx. 6500 Crs. as of today. The holding co. the gap will sustain but what I believe is that the dividends from IOC are going to substantially increase due to the following reasons:

-

IOC has had a very good quarter and is definitely going to have a very good Q1FY24. I believe even the next couple of quarters are going to be moderate. This will lead to IOC paying far greater dividends than last year when IOC made a ver tiny PAT.

-

Three very major expansions of IOC are going to be completed in the next 5 quarters (SOURCE: Motilal Oswal Report):

-

Barauni refinery expansion in April 2023 of 3 MT

-

Gujarat Refinery in Aug 2023 of 4.3 MT

-

and lastly and most importantly Panipat refinery in Sept 2024 of 10 MT.

This should provide significant profits as refinery margins are still way above average.

- Finally, IOC’s capex as compared to previous years is going to fall.

This article outlines this. It should provide further free cash flow to them.

2. Numaligarh Refinery Limited (NRL) expansion to be completed:

Numaligarh refinery is going to get expanded from 3 MT to 9 MT in December 2024 as per the management. This should significantly increase their income from refineries.

NOTE: In addition to refinery income, the expansion will also allow Oil India and other North East based exploration companies an outlet for their Natural gas that they can’t produce to their optimal capacity as there is a lack of demand in the region. You can read about this in detail in HOEC’s earnings calls where they talk about how they have the capacity to produce above 40 mmscfd of gas from Dirok but they can only produce 30 mmscfd as there is no outlet for the gas to be consumed.

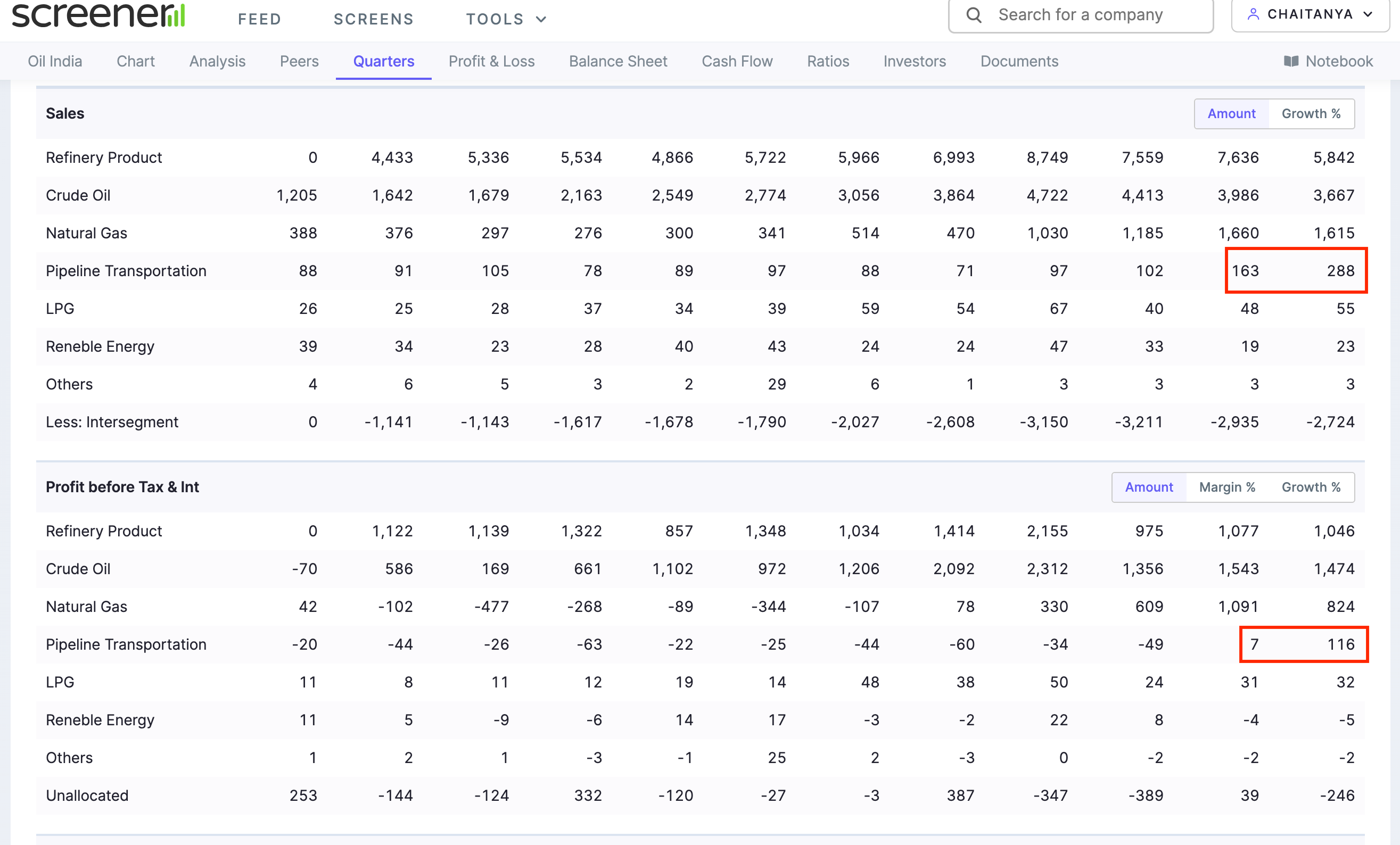

3. Pipeline income:

This is something that really seems to be unnoticed:

As you can see in the last two quarters the pipeline income has gone up significantly. This is most ostensibly because of the India-Bangladesh pipeline completion. I am not 100% sure about this as the management doesn’t really talk about this segment elaborately.

In addition to this pipeline, the Indradhanush pipeline is also going to get completed in phases over the next 2 years. Oil India owns 20% of it directly and 20% through NRL. They are most certainly not going to earn super normal profits on this pipeline but this should add to the PAT as the size of the pipeline Capex is quite huge.

CONCLUSION:

These are the three elements except the exploration part of their business which seems to be quite unnoticed and can provide a surprise to their earnings. These in addition to their target of increasing their oil production by 30% and gas by 60% in the next two years can lead to a disproportionate increase in their EPS and share price. Just for the record, I am not confident that they will be able to achieve their production targets, but they did increase their oil and gas production by approx. 4-5% even when ONGC’s production fell.

DISCLOSURE: I started accumulating the stock from 170 levels last year and still have a target of 30-40% upside in the next two years (this is excluding the 5-7% dividend).

| Subscribe To Our Free Newsletter |