As of today, I have the following changes to the model portfolio:

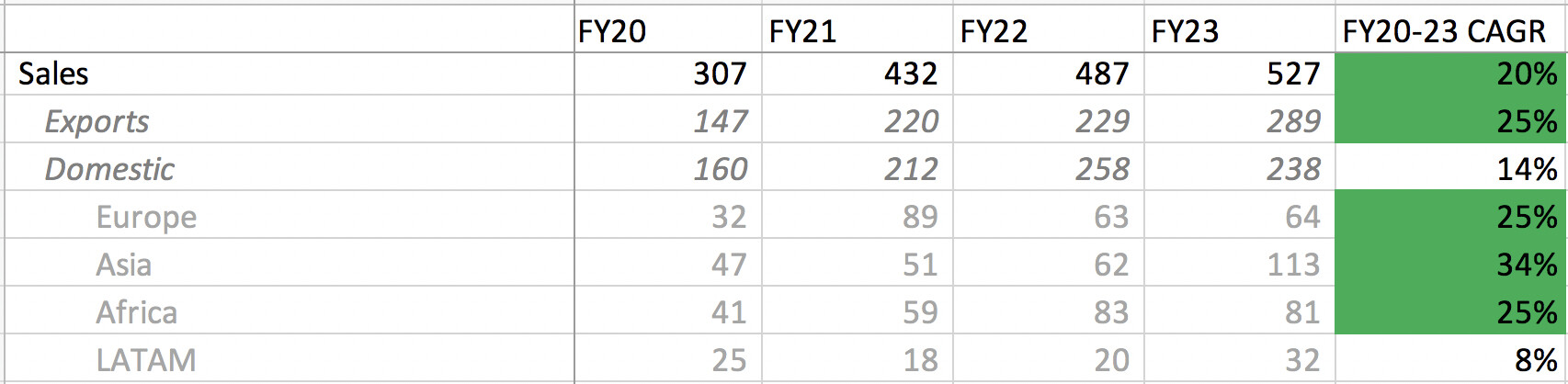

- Added Anuh Pharma as a new position at 2% allocation. Anuh Pharma came up with a large capex in FY20, since when they have grown sales and PAT at 20% and 40% CAGR.

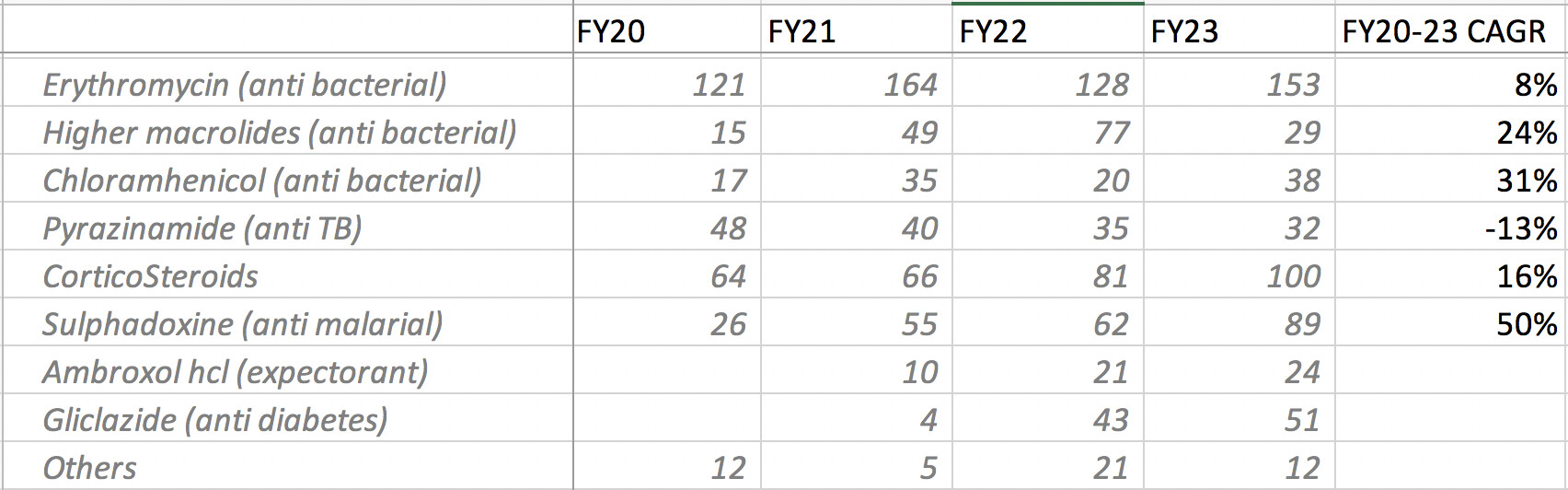

Importantly, this scaleup has happened due to ramp up in newer molecules. In FY20, anti-bacterial and anti-TB accounted for 65% of sales which has reduced to 48% in FY23. Anti-diabetes is now 10% of their sales. They have also launched vildagliptin which is another diabetes API. So they are migrating from acute to chronic focused portfolio, thereby diversifying their product basket.

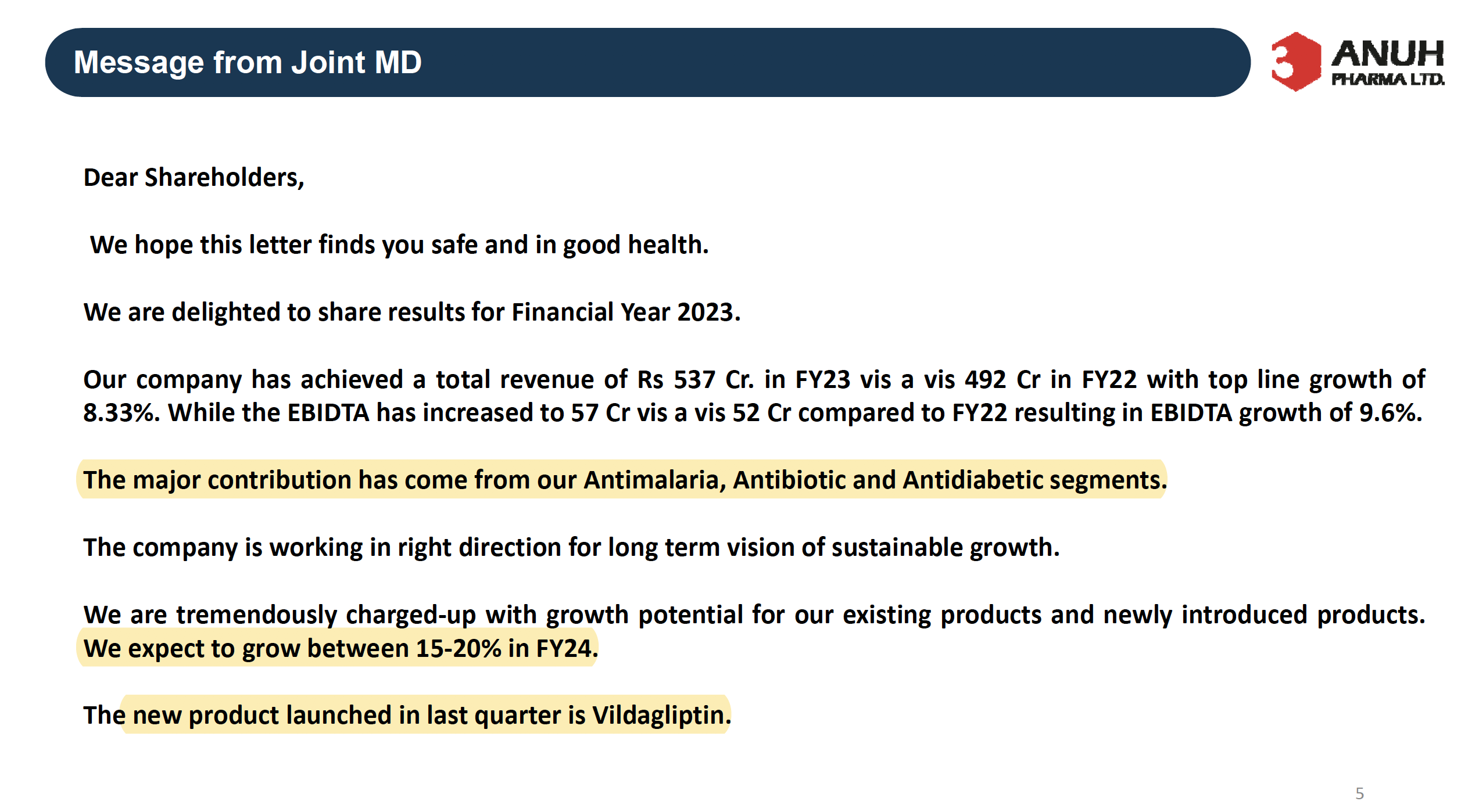

Management has guided for 15-20% growth in FY24 and further ramp up in newer products. This is a very conservative management that has funded most of their expansion using internal accruals and have maintained a very good dividend payout of 30-40% over time.

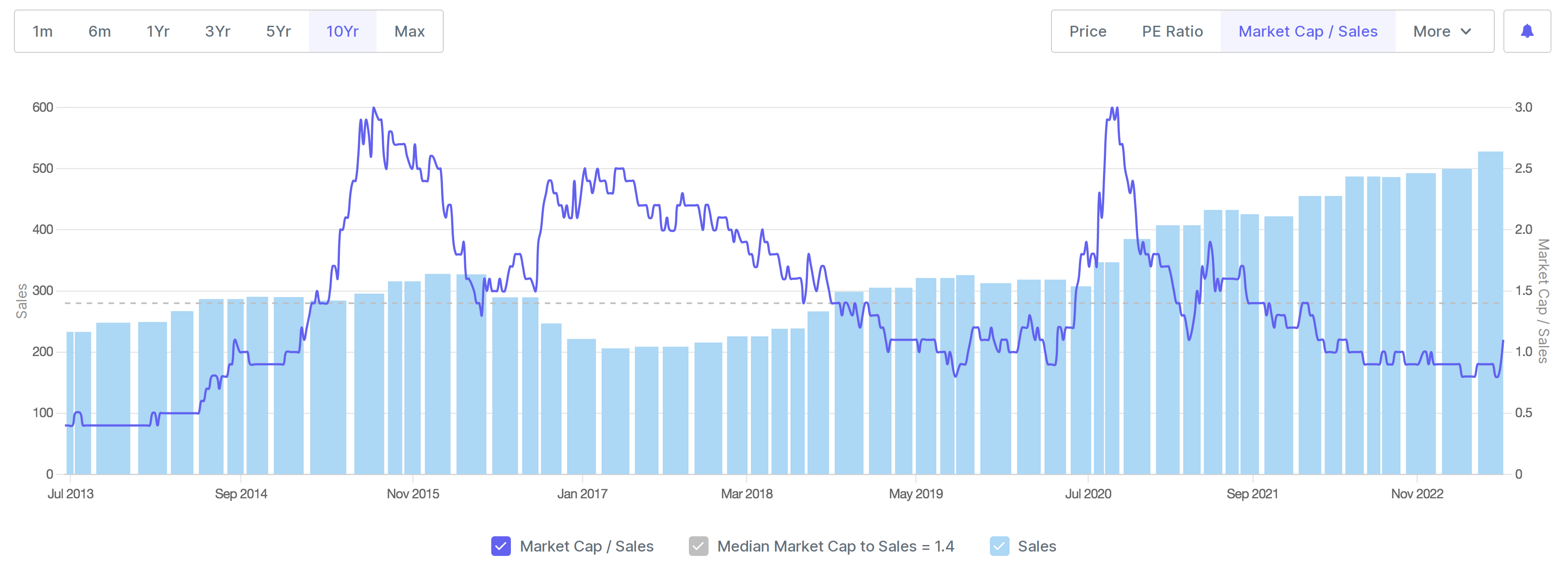

In terms of valuations, they are quite cheap. Post FY14, they have generally topped out around 3x sales and bottomed at 1x sales. Current valuations are towards the lower end.

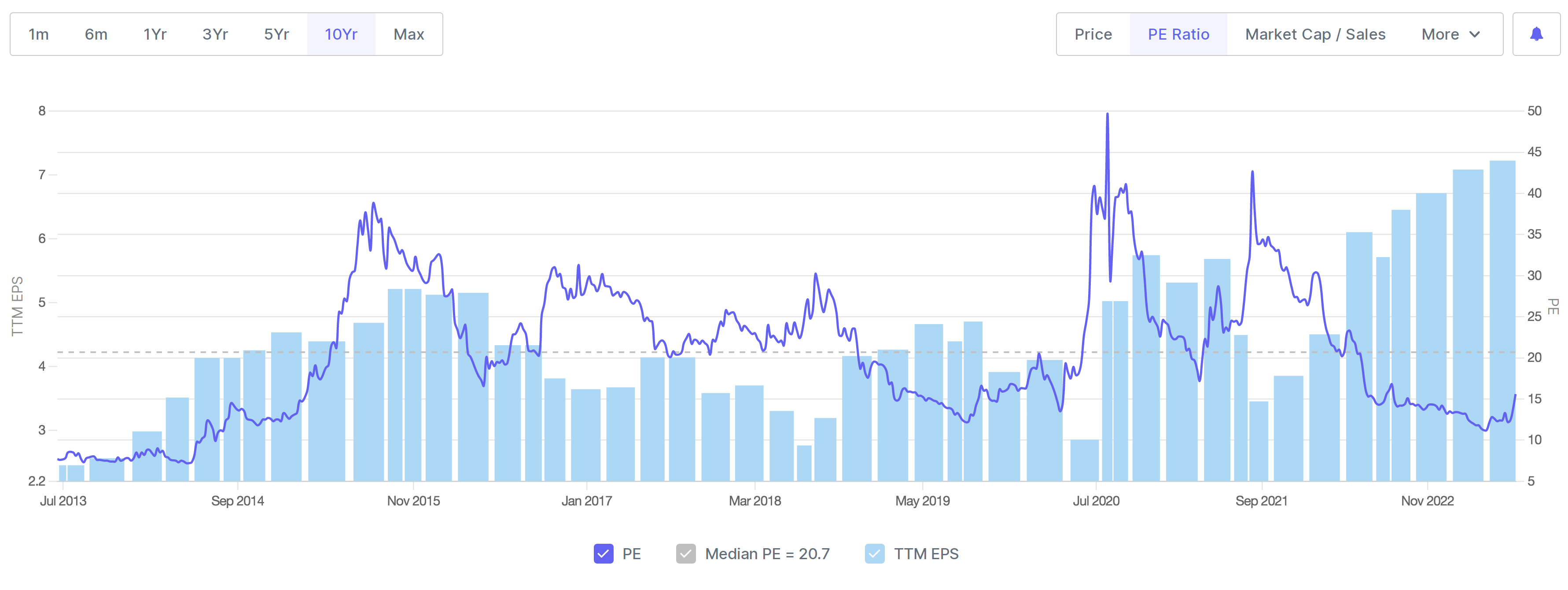

In terms of PE as well, they are quite reasonably valued.

Overall, Anuh Pharma has shown very good capital allocation, funding most of their capex through internal accruals and maintaining a good payout. With more focus on growth, I feel good value can be created in next few years. Lets see how it works out.

- Increased position size in Propequity from 1% to 2%. Company came out with good results, with sales growing by 21% in FY23. In last 4 years, they have grown sales and profits at 18% and 32% CAGR. If we exclude the 60 cr. cash, their current PE is 9x. Including the cash, they are available at 15x PE.

Propequity is expanding rapidly in their valuation business, having opened 30+ new branches in last couple of years. In terms of employees, they have added 100+ employees in this vertical in past year. In this business line, their main competitor are individual valuers, where Propequity’s main edge is a low turnaround time (TAT). As they get empanelled with more banks and HFCs, their sales can show very rapid growth. I want to make this a 4% position and will wait for execution in next few quarters before doing that.

-

Reduced position size in Stylam from 4% to 2%. There has been a huge re-rating in the stock since I initiated the position a few months back. Since most of Stylam’s business is B2B, I dont know if 30x PE is a sustainable multiple. To reduce valuation risk, I have reduced its position size.

-

Reduced position size in Aegis from 4% to 2%. Optically, Aegis’ results looked quite good, however looking underneath there were quite a few misses. Their core LPG terminalling business is not growing as expected and industrial distribution business is doing most of the heavylifting. I am worried that a lot of industrial distribution growth has come because of pricing arbitrage between propane and natural gas, and this can also reverse going forward. Given that Aegis is trading at a premium multiple, I have decided to reduce my position size.

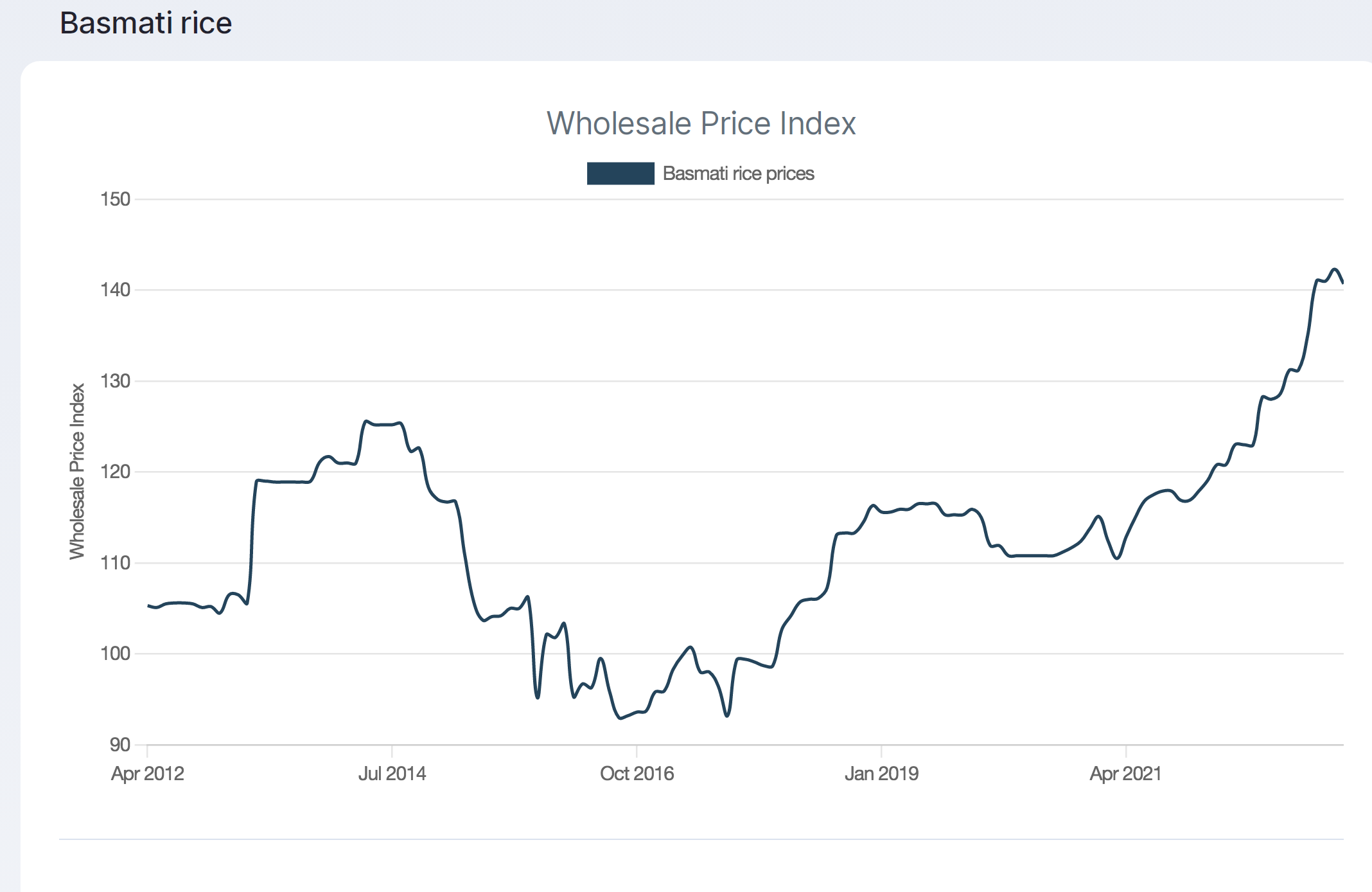

- Reduced position size in Chamanlal Setia from 4% to 2%. The basmati cycle has played out very well. However, due to the rapid increase in basmati prices demand has also softened.

Although Chamanlal trades at very cheap multiples (7.7x PE) and has shown amazing growth in the past (24% EPS growth in past-5 years and 26% in past-10 years), it hasn’t ever got high valuations. My own mental model is to enter near 1x PB and exit towards 2x PB. Adjusting for the revaluation of land, their current PB is around 1.75x which is closer to the higher end. If the cycle turns adverse, valuations can easily go back to 1x PB. Therefore, I have decided to reduce my position.

-

Exited Control Print. Since initiating the position in October 2021, company has grown EPS at 30% and share price has doubled. Broadly, they have traded between 10-20x PE in the past 5-years. Current valuations are towards the higher end and I have decided to exit the position.

-

Exited Suyog Telematics. I was very surprised (and annoyed) to learn that company has decided to increase their exposure to funicular business. In the past, management had promised that Suyog Funicular will repay debt to the parent (Suyog Telematics) once they are listed. Its been more than a year since listing of Suyog funicular, but debt hasn’t been repaid. Not only that, but they have also decided to put more capital in the funicular business by acquiring Haji Malang funicular. I dont see logic in this transaction and therefore am exiting my position.

As a result of these transactions, a 5% cash position has been created. Currently, I am looking to add Mayur Uniquoters as a new position. Additionally, I am looking to reduce (or sell) Aditya Birla AMC and replace it with a higher position size in HDFC AMC (or buy a basket of cheap brokerage cos). I haven’t made my mind yet and will update once I have more clarity. Model portfolio is below:

Core compounder (40%)

| Companies | Weightage |

|---|---|

| I T C Ltd. | 4.00% |

| Housing Development Finance Corporation Ltd. | 4.00% |

| NESCO Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Aegis Logistics Ltd. | 2.00% |

| Gufic Biosciences | 4.00% |

| HDFC Bank Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

| Caplin Point Laboratories Ltd. | 2.00% |

| P.E. Analytics Ltd | 2.00% |

Cyclical (47%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Aditya Birla Sun Life AMC Ltd | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Chaman Lal Setia Exp | 2.00% |

| Stylam Industries Limited | 2.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Sundaram Finance Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| Manappuram Finance Ltd. | 2.00% |

| Transpek Industry Ltd. | 2.00% |

| ANUH PHARMA LTD. | 2.00% |

| Shree Ganesh Remedies Ltd – PP | 1.00% |

Turnaround (2%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 2.00% |

Deep value (6%)

| Companies | Weightage |

|---|---|

| Geekay Wires | 1.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

| RKEC Projects | 1.00% |

| Subscribe To Our Free Newsletter |