Finmin changes mind, offers ethanol producers Cenvat relief – Financial Express (Impact on Balrampur Chini)

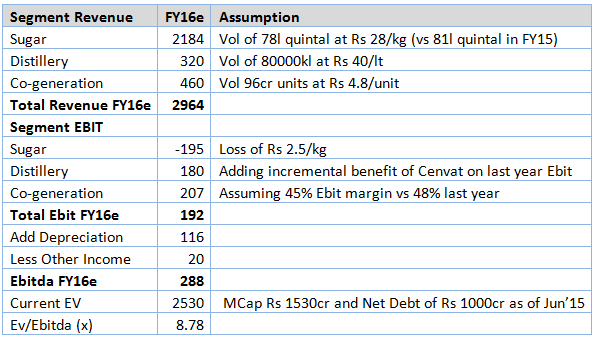

Impact on Balrampur

• For Balrampur, Company produced 32500kl of Ethanol in FY15 against total distillery production of 69900kl. With OMC offtake started picking up, company produced 21000kl of Ethanol out of total distillery production of 24500kl in Q1. Further, company is making investment of Rs 200cr in its distillery to align with pollution norms. With that, company will be able to run for 330 days vs 250 days earlier, effectively increasing its production 12000-17000kl of additional volumes by Sep’16.

• Company’s current realization is around Rs 40/lt with this cenvat and excise benefit, company’s cost will decrease by Rs 4-5/lts in upcoming season. Assuming, c15% growth in volumes in FY16, incremental benefit of cenvat/excise will be around Rs 35-40cr to its EBIT for this fiscal. For FY15, Company reported distillery Ebit of Rs 144cr which is likely to increase to Rs 180cr in FY16e.

• Overall, Company likely to report Ebitda of Rs 288cr (assuming Ebit loss of Rs 2.5/kg on sugar), Stock trades at 8.8x its FY16e Ebitda.

Sensitivity of Sugar loss on FY16e Ebitda – In FY15, Company made a Ebit loss of close to Rs 3.5/kg, base case I have assumed Ebit loss of Rs 2.5/kg in Fy16

Computation of Ebit loss for Sugar: FY15 Ebit loss at Rs 278.5cr; total qty sold during FY15 at 81.45lakh quintal, loss/kg works out at Rs 3.42/kg

Discl: Not invested, but sector does look interesting

| Subscribe To Our Free Newsletter |