My complete analysis on Jubilant Ingrevia

does not include the current quarter’s updates.

JUBILANT INGREVIA- Multiple Triggers In Place

Currently the company is not faring well, due to external factors but as and when the cycle turns it can benefit immensely in my opinion.

ABOUT

Jubilant Ingrevia, a global integrated Life Science products and Innovative Solutions provider serving, Pharmaceutical, Nutrition, Agrochemical, Consumer and Industrial customers with their customized products and solutions that are innovative, cost-effective and conforming to excellent quality standards.

Ingrevia was demerged from Jubilant Life sciences as on 01.02.2021 and company was listed on 19.03.2021.

Jubilant Ingrevia’s portfolio also extends to custom research and manufacturing for pharmaceutical and agrochemical customers on an exclusive basis.

Life science chemicals (56% of sales)

Specialty chemicals (28% of sales)

Nutrition (16% of sales)

Handles 5 Global scale Manufacturing sites with 50 plants and top 10 customers accounting for 20-25% of the overall revenue.

Expertise in 35 Technology platforms which include Acetyl, Pyridine/ Piperidine,

Ketene/ Diketene, Halogenation & others (At large commercial scale).

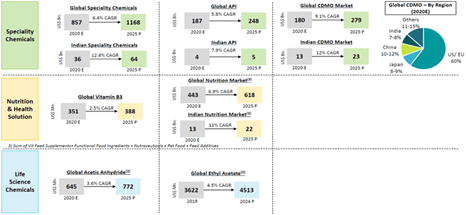

INDUSTRY

The products have use across Pharma, Nutrition, Agro chem, Industrials & consumer products which are all growing at a decent pace. Due to the diversified end user base Ingrevia is shielded from industry slowdown. They have a long runway for growth in all three areas they work in and have provided the below summary of market landscape.

The highest margin/value segment is Nutrition followed by speciality and then life science.

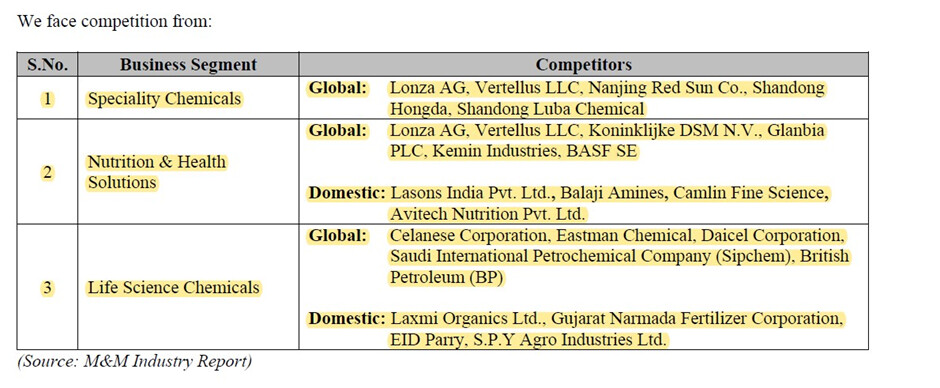

Major competitors are international MNC’s.

Since Ingrevia is the lowest cost producer in most of its products, they are the market leaders in those products and have the highest market share.

Amongst top 2 in pyridine-beta globally

#1 in 11 pyridine derivatives globally

Top 2 in vitamin B3(niacinamide) globally

#1 in vitamin B4 in domestic market

Top 2 in acetic anhydride globally .

MANAGEMENT

Bhartia Group is a well-established & reputable group and have been successful so far, are the promoters of Ingrevia. They have interests in various sectors & this demerger of Speciality chemicals business was done to unlock shareholder value.

Pre demerger, Jubilant lifesciences was not able to reduce its debt from 2010. Post demerger the management of Ingrevia has been successful in reducing the debt position significantly, this shows the renewed interest/focus or drive of the management to grow the business.

The promoters are very professional and let the hired management/team run the business. 5 out of the 7 committees are led by independent directors. The board of directors are also balanced in terms of promoters and independent directors. This shows the corporate governance standards of the company.

The company and management are very clear with the ESG standards and adhere to it.

ENTRY BARRIERS

Backward integration **- They are the lowest cost producer because they are fully backward integrated to the key raw material beta picoline thus being able to source the raw materials in-house without facing any supply volatility, also lesser freight costs (for raw materials to be transported). It takes a lot of time and capex to get to the level of backward integration Ingrevia is at.

Price leadership **- Lowest cost producer of pyridine-beta and all value added products. Due to years of experience

Switching costs **- Long and tedious approval process by customers, takes 3-5 years for product approval and facility audit.

Complex chemistry **- Demonstrated expertise in handling multi-step chemistries (up to 13 steps). Due to strong R&D and experience.

Technological knowhow **- Uses the niche technology (air oxidation) for manufacturing niacinamide-leading to lowest cost. Developed this process from scratch thus difficult to duplicate.

Connections with farmers **- Attained deep reach within the farmer community for Animal nutrition and Health products. Takes a lot of time as most farmers are not educated and must really understand the benefit they can derive from the product.

Brand recognition **- ‘ANICHOL’ for vitamin B4 is a leading brand and the company has another 18 brands. Brands are positioned in the minds of the customers thus hard to replace.

Handling large volumes of ketene **- Ketene is a very volatile compound and very difficult to handle or store. Ingrevia can handle huge volumes of it due to its decadal experience in the chemistry.

Multiple plants **- Ingrevia has 61 plants spread out in such a way so as to be the preferred choice of their customers in terms of freight costs and delivery time

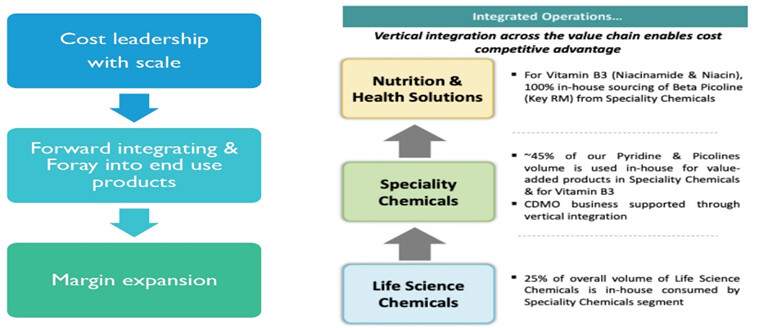

Forward integration **- Ingrevia uses the end products of its three business segments (nutraceuticals, speciality chemicals and life science) as feedstock for production among each other.

THESIS

Expansion – Ingrevia has planned a capex of Rs 2,050 crore over fiscals 2022 and 2025 towards expansion for diketene derivative products, expansion of facilities for crop protection chemicals, vitamin B3 products and acetic anhydride. The capex is progressing as per schedule and is expected to be funded through internal accrual, with minimal reliance on external borrowings. The expected asset turns will be >2x and >20% ebitda margins. Expected peak revenue is 9500cr, but speciality and nutrition segment will increase from current 46% to 65% thus higher margins. Commissioned the Diketene phase one and acetic acid plant.

New products **- Plans to launch 60+Products (in Pipeline) for next 4 years. These new products will majorly be higher value products (margin accretive).

Management expectations **- Wants to double the revenues by 2026 . This will be achieved through the mammoth 2000cr capex, entering new products and better reach to customers.

Firing the CDMO engine – New GMP and non-GMP facilities, which are expected to be ready during Q3 FY’23, will help them in capturing growing demand of CDMO projects. CDMO is again margin accretive. This will start adding meaningfully once the facilities reach optimum utilization. Entered a contract worth 270cr over 3 years.

Loan Prepayment – Ingrevia repaid/prepaid about Rs 548 crore long-term debt over fiscal 2022 and first quarter of fiscal 2023, reducing debt at a fast pace to lighten the balance sheet and increase profitability.

Foray into Diketene chemistry – Indian market size is $150mn (2019); 40% was imported; Laxmi Organics is sole Indian manufacturer with 55% market share; Plans to launch 6 derivates; One of the few global companies capable of handling large volume of ketene; Huge demand coming up for diketene and one of the leading producers has exited. This product is mainly to substitute imports. Already was into ketene production now entering the value added diketene segment.

Agro-active – Moving up value chain from ingredients to producing agro-actives (for pesticides).

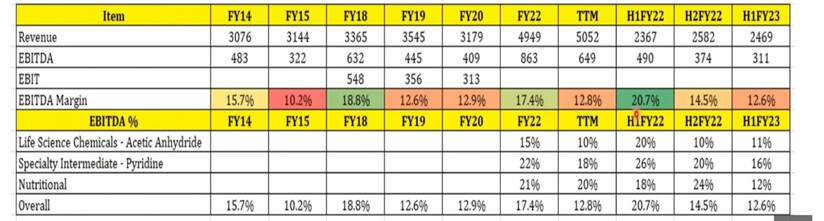

Margins bottomed – As we can see from the picture below the lowest margins for Ingrevia range from 10-13%. In FY15 the margins were 10.2% then there was a margin expansion, same happened in FY19 and 20. Currently ebitda margin is at 12.6%, the margins of all three segments are currently compressed due to supply chain, inventory and cyclic reasons.

Credits to @Worldlywiseinvestors sir’s and @suru27 sir’s youtube video for this particular thesis pointer and image.

Pre mixes – The nutrition segment consists of vitamins and premixes, there is a flu going around Europe. This is affecting the demand for the vitamins and thus causing a contraction in margins of manufacturers of vitamins all around the world. The management is trying to increase the share of the pre mix segment in the total revenue. Pre mix has higher margins which will help balance out the current margin contraction that can be caused by the vitamins.**

Foray into Fluorine chemistry – Ingrevia is trying to enter the fluorine chemistry, although the competition here is high** **(srf, navin fluorine, gfl) the demand or fluorine products/derivatives is also high. This segment is high margin. No clarity given on the type of products they will be manufacturing.

ANTITHESIS

Regulatory risks – Previously Paraquat (herbicide) which uses pyridines was banned by multiple countries thus Ingrevia had to stop its production. There is risk if the government brings in new regulations or product bans for any of Ingrevia’s existing products.

Lifescience segment – The lifescience segment of Ingrevia is commoditised, it has no supply/ pricing power for any of its products. The products here have very low margins therefore acting as an overhang for the overall margins. If the management isn’t able to walk the talk of reducing the share of this segment as has been told then this may impact margins as well as the reputation of the company.

Raw material volatility – Acetic acid is the major raw material and is largely imported. China has world’s 42% capacity of acetic acid. There can be volatility in prices due to freight costs or availability also as China is trying to control its pollution levels, the government is shutting down various plants and manufacturing sites this can lead to shortage is supply if acetic acid plants are shut down.

ESG compliance – Before 2015 there were various esg compliance issues with the company there were various cases by employees and villagers against the operations and functioning of the Gajraula plant, there was a chemical leak at the Nira plant and few other pollution related cases (although this was long back and no such issues now).

Power and fuel costs – Energy costs form a significant part of the operating costs, current spike in energy prices has hurt the margins and can also do so again in the future if these prices persist. Coal is being imported right now as government couldn’t fulfill their contract to supply it due to some shortages although it is expected that the supply from the government will resume from January 2023.

Flu in Europe and US – The majority of the vitamins manufactured are supplied to US and Europe. There has been a continuous rise in flu cases thus the demand for vitamins has fallen, leading to inventory built up by both distributors and Ingrevia.

Demand risk – Ingrevia already has done a huge capex. If there is an economic slowdown or anything that may suppress demand for its products, the company won’t be able to convert this huge capital expenditure into cash flow. This may result in underutilisation of the new plants and thus an increase in debts to fund the working capital.

As @SajKap sir said, company ki niyat kharab nai hai but samay kharab chal raha hai.

Think about it.

| Subscribe To Our Free Newsletter |