Can not be a better time than now to re-visit Natco thesis considering that Natco has completed one full financial year of Lenalidomide (gRevlimid) supply (in a quantity restricted manner though) for US markets. I think we need to evaluate this from two/three broader dimensions:

1. Market share impact to Innovator:

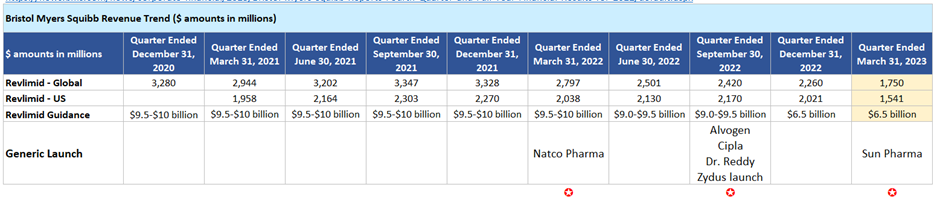

Below is revenue contribution data for Bristol Mayers Squibb for Revlimid (both Global and US specific) collated from different regulator fillings over past 10 quarters. This is a good starting point to see how competition is unfolding, impact on their market share and overall market structure.

-

BMS was able to hold the fort for 3 full quarters maintaining $2B+ run rate from even after Natco launched first generic in the market in March’22. Part of that can be explained by the fact that Natco had volume limited launch (that too for 4 strengths out of 6).

-

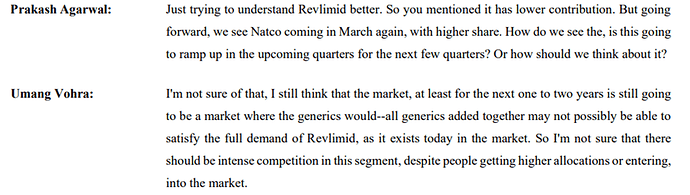

Real impact has started unfolding starting recently closed March’23 quarter. ~25% Q-o-Q / 33%Y-o-Y revenue drop. Must be to do with entry of 4 new generics in the month of Sep’22.

-

Even from guidance perspective, till last quarter, BMS was maintaining an annual $9B+ revenue guidance. Only in the march’23 filling they have cut the guidance by good ~30%+ (to $6.5B). Broadly, thinking this ~INR 2000 is the number that is pivotal to gauge revenue visibility for Natco and rest generics for next 12 months (or so). Off course, volume quota will get increased for each player every 12 months and accordingly BMS will have revision to revenue guidance.

-

BMS has bigger challenge in ‘Global’ sales. Reading through investor presentation (link) of Lotus/Alovgen (who is the second generic in US, after Natco), looks like they garnered significant chunk in EU, Canada and JP. This has some implication to Natco since they too want to grab chunk of Lenalidomide market through subs outside US.

2. Most updated competitive Landscape of generic Lenalidomide:

-

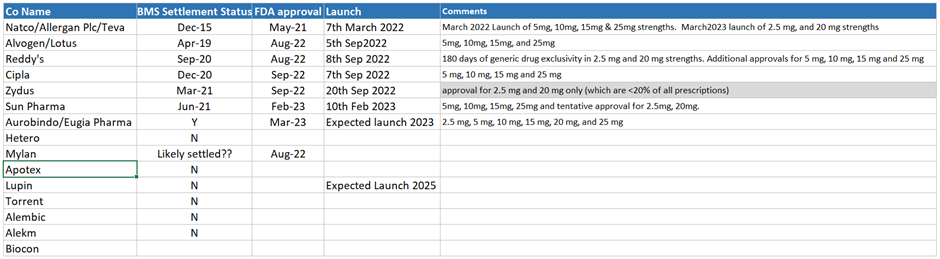

Based on current visibility, this is a 6 players market as of now with due settlement, FDA approval and market launch. Speculation that Auro to launch by Sep’23 (via subsidiary Eugia Pharma).

-

There are 6/7 more player waiting to join-in, however, none of them have reached BMS settlement as of now. Therefore, safe to conclude that initial wave of competition is topping out and this will be a 8 player game for next couple of quarters.

-

Even if new competitors comes in, they may have to start with low single digit dispensing quota with step-up quota every 12 months – as the norm has been for most of the settlements. This is a significant edge for anyone who started early. Natco has clear head start and will be ahead of rest all competitors (existing and future one) since they will cross the time milestone ahead of rest.

[ Think Zydus concall has a subtle cue that first year quota for all/them was 4% going up to 9% second year]

-

Another important factor to notice is the drug strengths that each one has approval for. As of now, its Natco and Dr. Reddy who looks to have approval for most strengths (2.5 mg, 5 mg, 10 mg, 15 mg, 20 mg, and 25 mg). Zydus may end up being a peripheral player only with currently approval of 2.5 mg and 20 mg only (which are <20% of all prescriptions), unless adding more prevalent strength to kitty.

3. Natco Profit Share Projection:

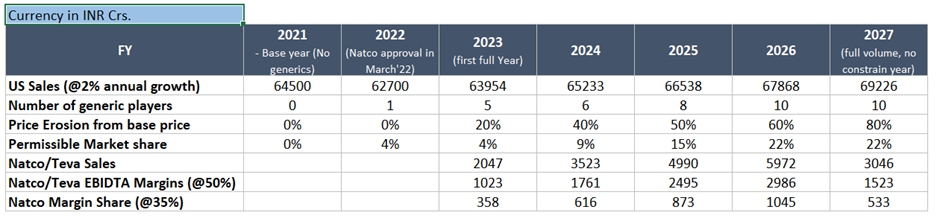

This is little tricky, for the very fact that each of the participants are very guarded about the communication. Incidentally, Wallgreens has a class action suit against BMS where Teva/Natco/Dr. Reddy/Sun are co-accused – challenging BMS settlement with generics as anti competitive/anti-free market. So, effectively, will be very hard to get a sense on price erosion, market share split (between innovator/generics and within generic players). Keeping those considerations/limitations in mind, below is a broad excel work to see what the conservative case can be:

[Clear call-out: This working has certain assumptions built-in since disclosed info is very limited]

-

Interestingly, Teva (Natco’s) partner is very subtle about Revlimid prospects while being reasonable transparent about rest of the other block buster drugsin pipeline.

-

On the other hand, Indian generic players like Dr. Reddy and Cipla are sounding very upbeat about market share. Some estimates suggests that Dr. Reddy had infact higher share than Natco at some intervals since they had 180 days of generic drug exclusivity in 2.5 mg and 20 mg strengths.

Dr Reddy Q3,FY23 concall:

Cipla Q3’FY23 concall:

-

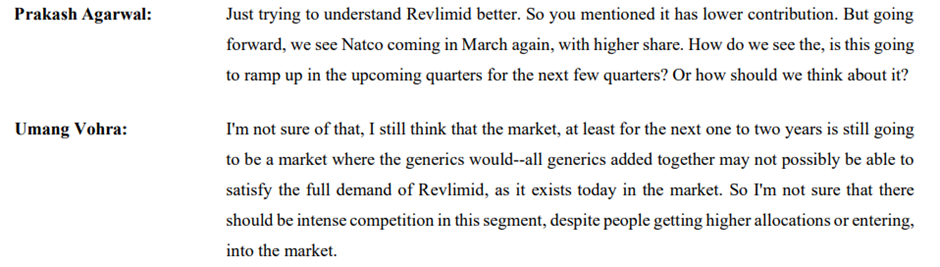

Even a marginal player like Zydus who has approval for limited strengths only are confident that there is no price war at the moment.

Zydus Q4’FY23 concall:

-

With current facts and assumptions in the mix, looks like Natco can have addition of incremental ~300 Crs. to bottom line for each of the years till Jan 2026 (when no holds barred field opens up for all). Some estimates even suggests that beyond 2026 Natco and Dr. Reddy will be big winners on account of early mover and distribution reach respectively.

As a follow-up activity, I intend to cover some aspects related to US pipeline, further growth prospects for ROW subsidiaries, scalability of Agchem vertical etc.

Call for help: Inhouse RRR trio (Rajat (@rajats ), Rohit (@rohitbalakrish_ ), Rupesh(@rupeshtatiya.) , I think you guys track Natco. Feel free to add your perspective, additional info etc. to make it more comprehensive.

Regards,

Tarun

Disc: Sold my holding in Natco once 180 days exclusivity was over in Sep’22, as per initial plan.

| Subscribe To Our Free Newsletter |