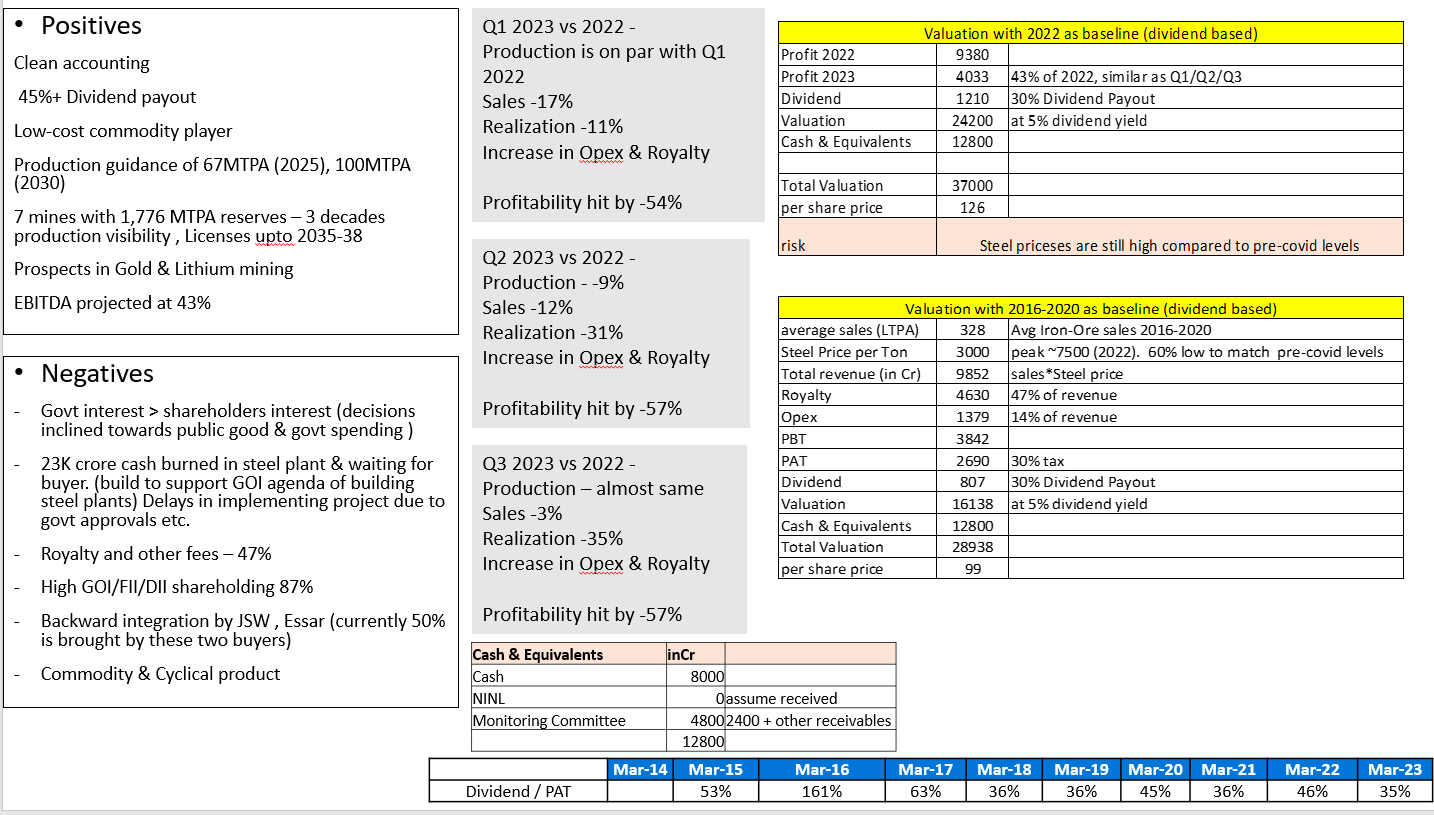

Thanks @utsav31 for pointing this out. This is a commodity company and the mistake i have done is valuing it based on the PE number.

The ideal way to value this is based on the –

-

Book value. i.e we should invest when the price is less than book value.

-

As NMDC is dividend paying company and most of the dividend is paid to govt of india (61%). There will be assurance that dividend will continue to flow.

Dividend – Rs.14.74 (2022), Rs.7.76 (2021), Rs.5.29 (2020), Rs.5.52 (2019), Rs.4.3 (2018)

Moreover the prospects of the company remains optimistic. As they have large mines with useful life upto 2035, Low cost operations, low debt, One advantage of having GOI ownership is that the accounts will be relatively clean & scrutinized .

Below are the valuation scenarios based on Dividend –

| Subscribe To Our Free Newsletter |