Unit Level Economics of Equitas SFB in different products:- (Posting here as other thread isn’t open)

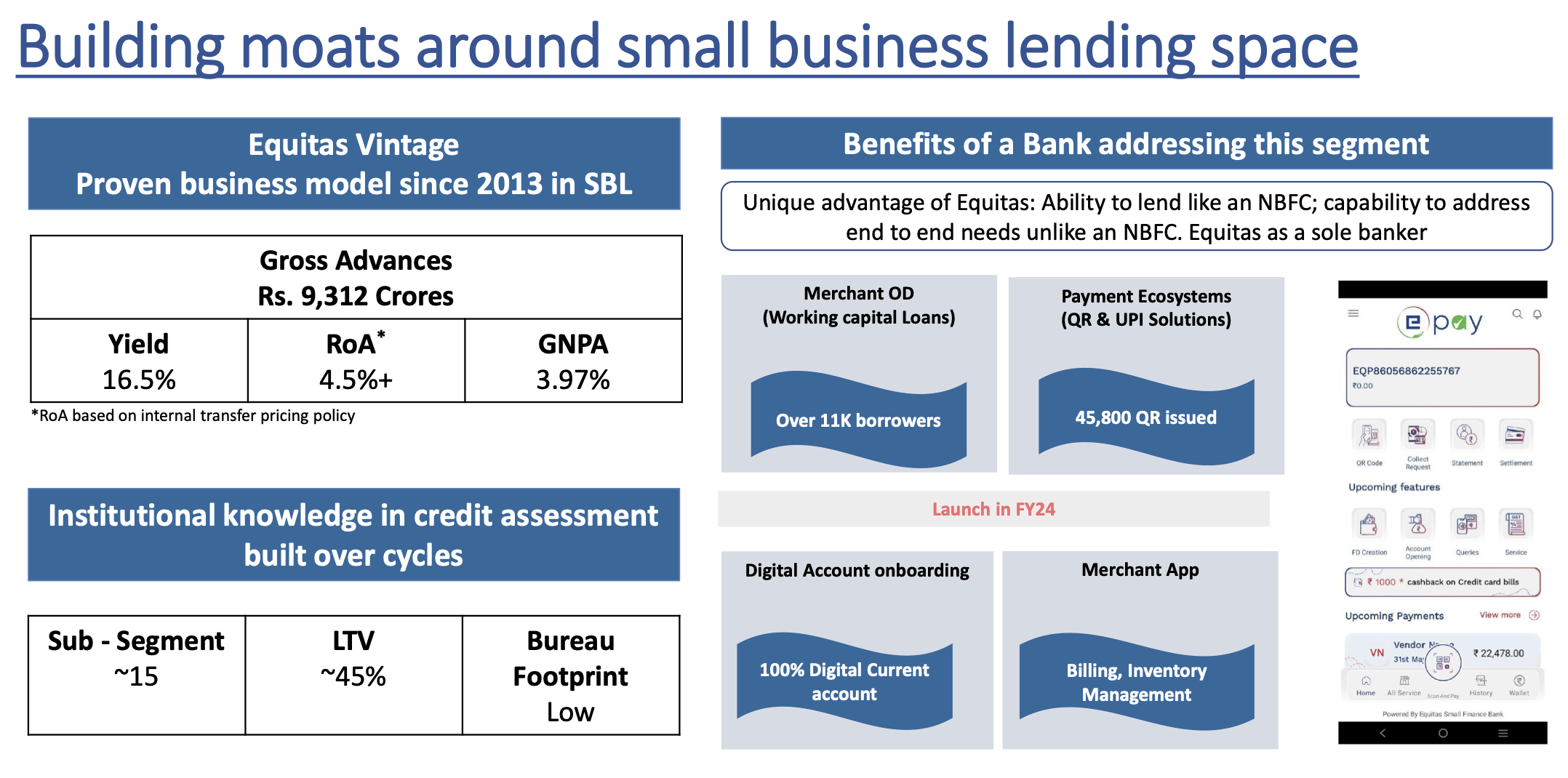

- Small Business Loans:– These loans contribute 36% to the entire book, and have grown at a CAGR of 44% between FY15-FY23.

This Business unit does ROA of 4.5%+.

Average ticket size of these loans is below 6 lakh rupees.

These loans are high opex in nature but are extremely profitable as seen by the ROA. This is similar to what FIVE star finance or Aptus do. Only real difference is- that EQUITAS has much lower cost of funds vs the other 2.

Average Credit cost from FY19 till date has been 2% in this division and this includes the covid wave. In FY23, GNPAs were 3%+ in this business unit. As the end borrowers have just recovered. Overall, RSL loans and GNPAs have fallen back to pre covid levels in Q4FY23.

Average GNPA in this division has been 3.14% vs Industry average of 4%+.

Yields in this segments are close to 18%.

2. Microfinance:-

This business division used to be 28% of the mix in FY18 and this has fallen to 18% in FY23. Management has guided to bring MFIN below 15% over the medium term.

This has been a deliberate strategy, as EQUITAS was primarily a Microfinance institution. Mix of Microfinance has fallen over the last 10 years.

This is indicated by their Yields, as Yields in unsecured loans are the highest. Overall Yields have fallen from 21% in FY18 to 17% as the mix of Secured asset class has increased as a % of the book.

Mircofinance Unit Economics:-

ROA of 4-5%. Average ticket size remains small at Rs.27,000 and Credit cost is 2.5%. Yields on these loans are 21%+.

- Vehicle Finance:- This segment contributes 25% to the overall loan mix.

In the Vehicle finance book, 71% of the loans are given to Small & Light Commercial Vehicles.

22% of the loans are given to Medium & Heavy Commercial vehicles.

This business unit had poor profitability in last 2 years due to covid related stress. ROA was sub 1.1% and Yields on these loans are close to 16%. High in opex, as indicated by 5.5%, cost to assets ratio. Recovery of Profitability in this unit can cushion the overall ROA going forward.

- Housing Finance:– this contributed 10% to the overall Loan Mix. These loans have an average ticket size of less than 10 lakh rupees. This is similar to what AAVAS, Aptus and Home first do.

Yields on these loans are :- 10.3%.

This a fully secure loan product. Opex in this business is very high, as this business unit has started scaling up just recently.

The bank is also going to launch other products like credit cards and Personal loans.

Closing thoughts:-

-Bank has consistently started hitting 2% ROA in last 2 Quarters. And the incremental ROE has gone above 15% in Q4FY23. If these numbers sustain with asset quality sustaining, things can become interesting.

As AU with 8% unsecured loan book+ 92% secured book,1.8% ROA is at 4.56x Price to book.(165 rs is the latest BVPS)

Equitas has re-rated a bit but given the Book Value per share is at 45 rs (post merger). There could still be some room looking at the changes in incremental profitability.

Currently, only 2 Small finance Banks have transitioned to secured products. Others are still majorly in Microfinance or IGL loans.

Disc: Not a recommendation to buy or sell by any means. Sources used:- Investor presentation, QIP Document, Philip capital report, and Kotak Report.

| Subscribe To Our Free Newsletter |