Hi guys, Lest understand their current order book and execution

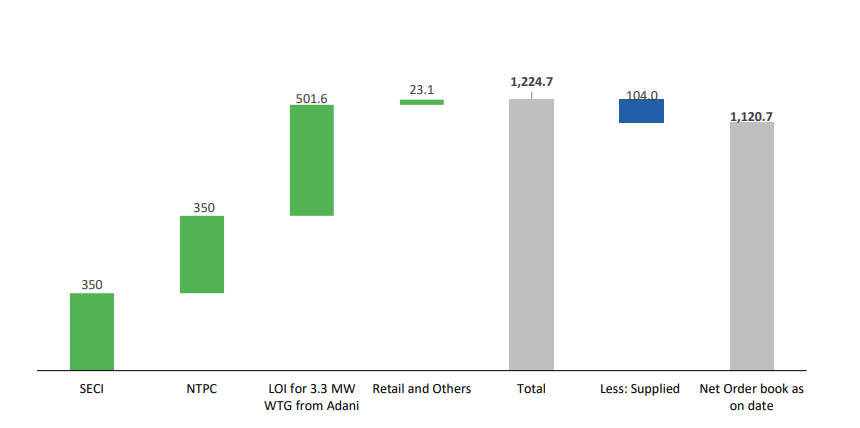

- This is the current order book of INOX, now this 350MW from SECI consist of 50MW of Nani Virani SPV and 200MW is from SECI III and 100MW from SECI IV.

@amey153 sir if you could please explain how will this be recognized. I mean 160cr would be through revenue and 100cr directly into equity??

300MW at 5cr/5.2cr per turbine can generate a revenue of 1500cr to 1600cr so if they execute this they would probably incur a loss of 200cr. Is this the way we can look at it??

-

They have been wining orders from NTPC till now and this months we have the NTPC auctions. So is there a possibility that hypothetically they win good orders from NTPC and they don’t proceed with SECI III & IV and what ever CWIP they have done they write that off.

-

Now from 350MW of NTPC order 150MW execution some what started between MAY – AUGUST 2022. So this would most probably be completed in Q1/Q2 FY24 generating revenue of roughly 700cr to 800cr. The balance 200MW execution started in Q1FY24 hence this can at the earliest be completed in Q4FY24 or Q1FY25.

-

The balance 501MW form adani will only be commenced once they have the certification which is in the final stage.

-

CONCALL

If they want to grow revenue multiple times then SECI III and IV is must. So 350MW from SECI and 150MW from NTPC. Looks like their next year revenue would be 2500cr. But will they be able to profit out of it. @amey153 sir any comments on this??

Next year interest cost can be 200cr so they save close to 140cr form here as well.

FY25 will have revenue from 200MW NTPC and 500MW from adani and in this they are confident of generating 14% to 15% EBITA. 700MW is like 3500cr revenue and EBITA of 550cr. They want to be debt free in next 12months. FY25 looks pretty good.

POSITIVE TRIGGERS

- NTPC auction in july so if they can win from here

- Certificate for 3MW series turbine

- Execution of 500MW (looks very likely) 2500cr revenue ( Doubt on profitability)

TECHNICAL

Looks very interesting, There are only 2 things which I am not very clear about or which are potential risk.

- SECI III and IV profitability

- Delay in getting the certification for 3MW series

@amey153 Sir if you could please give your view

Disc – Interested, not invested yet

| Subscribe To Our Free Newsletter |