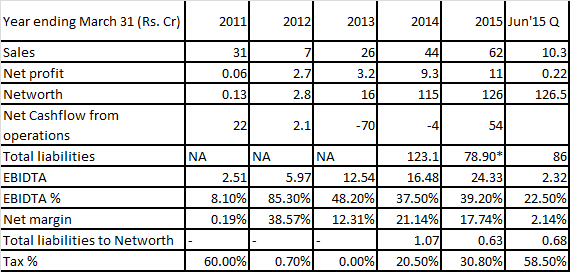

The company looks interesting. A brief of its financials:

(* long term debt is Rs 22.5 cr from Tata Capital payable in Sep 2017; unsecured’ bullet repayment. Short term debt is Rs 4.8 cr)

Investment thesis:

• Slightly difficult to project financials for each year

• Therefore, there is need for a big picture call

• Over 5 years, existing 14.3 million sq ft of development could yield sales of Rs. 2500 crore as per the company presentation (works out to appx. Rs. 1750 per sq. ft, which seems reasonable)

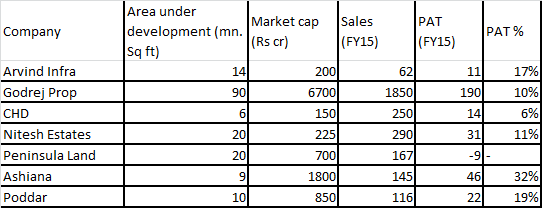

• Godrej properties average net margin for last 5 years is 15% (range 10.3-19%; 10.3% for FY15). Assume 10% for Arvind.

• Net profit works out to Rs 250 cr (Rs. 375 cr. Assuming 15% net margin)

• This is average of Rs 50 cr net profit per year (although it would be lower to begin with and would increase with time)

• Assume PE of 20 after 5 years (current PE of Godrej is 33).

• Market cap could be 20*50 = 1000 cr. i.e. 5 times of current market cap of Rs 200 cr. Sufficient margin of safety?

Risks:

• Execution ability

• Company needs to keep getting more projects so that growth continues to remain visible, so as to justify 20 PE

• Owners are mediocre – not pristine, but not a total chor also.

• No change in business model – continue to focus on residential and remain asset light

• Heavy comparison with Godrej properties

Annual report: http://www.arvind.com/pdf/annaul_finacial_reporting/2015/Subsidiaries201415/ArvindInfrastructureLtd.pdf

Change in inventory of negative Rs 37.05cr seems to have had a major impact on profitability. Reduction in trade and other receivables by Rs 73.9cr has positively benefited cashflows. Need to look deeper into these.

Just did a quick relative check (figures are rounded; please inform if there are any errors):

Views welcome.

Disclosure – initiated a starter position today. Not a recommendation. May add/or exit based on further study.

| Subscribe To Our Free Newsletter |